Main Takeaway

Offering payment plans wins deals that a single large invoice would kill, but only if you build them on a solid foundation: a deposit upfront, automated collection, a clear late-payment policy, and real-time visibility into what every client owes. Get the structure right, and payment plans improve cash flow rather than threaten it.

What Is a Payment Plan?

A payment plan is a formal arrangement between a business and a customer that divides a total balance into a series of scheduled payments made over an agreed period. Rather than requiring a single lump-sum payment, the customer pays in portions, typically equal installments, at predetermined intervals: weekly, biweekly, monthly, or at project milestones. Payment plans can be interest-free or include a financing fee to compensate the business for the time value of deferred revenue. When structured correctly and supported by automated billing, they are one of the most effective tools a service business has for closing larger deals without taking on unmanageable credit risk.

There is a deal-killing moment that almost every service business has experienced. A potential client loves what you do, the scope is agreed upon, and then you present the total. The number is right, it reflects the value you deliver, but it is more than the client can commit to in one payment right now. The engagement stalls or disappears entirely.

The fix is not to discount. It is to restructure when the money arrives. Offering payment plans turns a single pricing barrier into a series of manageable steps, and for many clients, particularly small businesses and growth-stage companies, it is the difference between signing and walking away.

The real question is not whether to offer payment plans but how to do it without creating cash flow problems of your own. A poorly designed payment plan can leave you financing a client’s operations indefinitely, absorbing the risk of missed payments, and losing track of what is owed. A well-designed one does the opposite: it accelerates decisions, improves collection predictability, and deepens client relationships.

Why Businesses Offer Payment Plans

The strategic rationale for offering structured payment arrangements goes beyond simple customer convenience. When implemented thoughtfully, payment plans actively support revenue growth and collection efficiency.

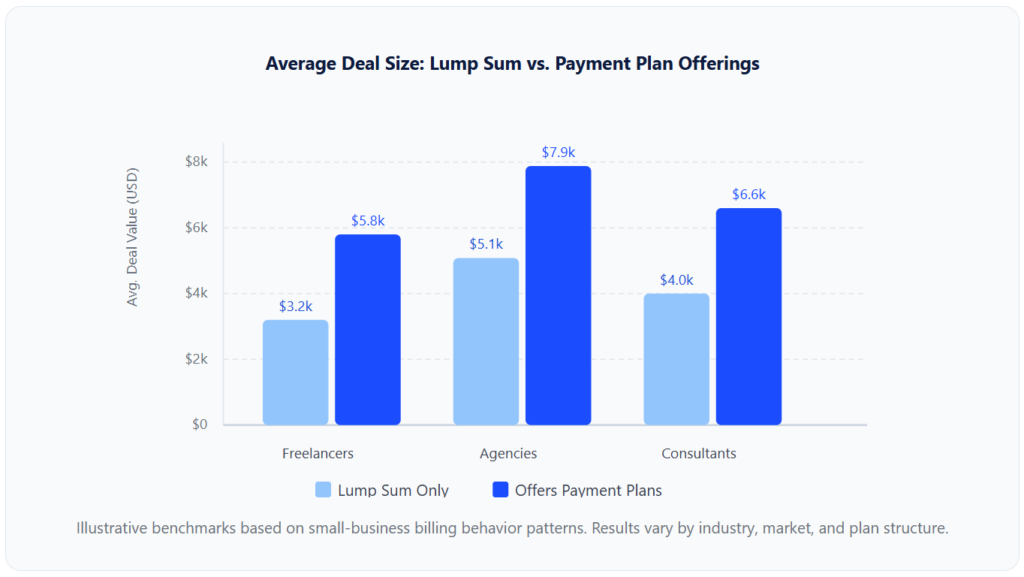

Larger average deal size. When price is no longer a single number that must be swallowed whole, clients are more willing to engage at a higher scope. A $12,000 website project that would have been rejected as a lump sum becomes a $2,000-per-month conversation over six months. The business earns more per client; the client gets what they actually need.

Faster close rates. Decision-making stalls when the financial commitment feels large and immediate. Breaking the total into manageable installments reduces the psychological weight of the decision and shortens the approval process, especially in organizations where expenditure approvals depend on amount thresholds.

Competitive differentiation. In markets where competitors all quote the same services at comparable prices, flexible payment terms can be the deciding factor. Many clients will choose a vendor who accommodates their cash flow over a cheaper one who demands full payment upfront.

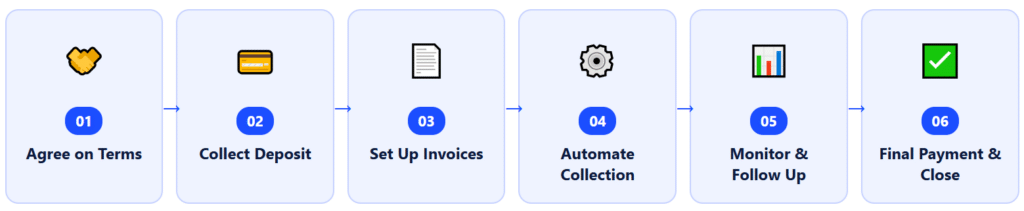

How a Payment Plan Works: The Full Lifecycle

Understanding the mechanics of a payment plan from start to finish is the first step toward designing one that works reliably. At its core, the process involves six phases, from the initial conversation with a client through to the final payment and account closure.

Phase one: Agreement

Before a single invoice is generated, both parties need a clear written record of the payment terms. This does not need to be a complex legal document, but it must specify the total amount, the number of installments, the payment schedule, the accepted payment methods, the late fee policy, and what happens if the plan is cancelled midway.

Phase two: Deposit

Collecting an upfront deposit, typically 20 to 50 percent of the total, is the single most important safeguard in any payment plan. The deposit covers a portion of your work immediately, signals the client’s seriousness, and creates a financial barrier against early-stage abandonment.

Phase three: Invoice setup

Once the deposit is received, you configure the remaining installments in your billing system. Each installment generates an invoice on the agreed date, sent automatically to the client’s billing contact. With installment billing software, the full schedule of invoices can be pre-generated at once, so the client can see every upcoming payment, which actually reduces late-payment disputes significantly.

Phase four: Automated collection

Each invoice should trigger automatic payment processing if the client has a payment method on file or an automated reminder sequence if they pay manually. The goal is zero manual follow-up under normal conditions.

Phase five: Monitoring

Even with automation, someone needs to review outstanding balances on a regular cadence. A client who misses one payment might be dealing with a temporary cash flow issue; a client who misses two in a row may require a more direct conversation.

Phase six: Final payment and close

When the last installment clears, send a confirmation and close the account in your billing system. Overpayments on installment plans are typically applied to the final invoice.

Structuring Payment Plans That Protect Cash Flow

The mechanics above tell you how a plan works. What determines whether it helps or hurts your financial position is how the plan is structured in the first place. There are five levers that matter.

1. Set a Minimum Deposit Threshold

There is no universal rule on deposit size, but a floor of 25 percent is reasonable for most service businesses. For custom or high-cost engagements, web builds, consulting retainers, and construction projects, 40 to 50 percent upfront is standard practice. The deposit should at minimum cover your cost of goods or time for the first phase of work, so you are never out of pocket if the relationship sours.

2. Keep the Instalment Count Manageable

More payments mean more opportunities for something to go wrong. For most service transactions, three to six installments is the right range. Plans that extend beyond six months without a compelling reason, a large contract value, or a clearly defined milestone structure begin to carry meaningful credit risk that you are absorbing on the client’s behalf.

3. Decide on Financing Fees Deliberately

Many businesses offer short-term payment plans (two to three payments over 60 days or less) interest-free as a sales incentive. For longer arrangements, a modest financing fee of one to three percent of the total is both standard and appropriate; it compensates you for the time-value cost of deferred income and provides a small cushion against late fees you may never collect. The key is to make this fee explicit in the agreement rather than folding it into your quoted price in a way that creates confusion later.

4. Automate Everything You Can

Manual payment plan management is unsustainable. As your client base grows, the administrative overhead of tracking who owes what, sending reminders, and following up on missed payments becomes a serious drain on time. Collection automation handles reminders, failed payment retries, and escalation sequences without any manual input, freeing your team to focus on delivering the work rather than chasing invoices.

5. Define a Clear Default Policy

Your payment plan agreement should state explicitly what happens if a payment is missed. A reasonable structure: a grace period of five to seven business days, then a late fee (typically 1 to 2 percent of the installment amount per month), and after two consecutive missed payments, the right to pause service delivery or require the remaining balance in full. Having these terms documented upfront eliminates ambiguity and gives you a clear basis for enforcement if needed.

Structuring Tip: Pre-Bill Before the Due Date Send the installment invoice three to five business days before it is due, not on the due date. This gives clients time to process the invoice through their own accounts payable system, especially important for B2B clients who may require internal approval before releasing payment.

Real-World Examples by Industry

Payment plans look different depending on the nature of the work and the typical transaction value. Here are common structures across four service categories.

Web Design and Development Agencies

A standard structure for a $9,000 website build might look like this: 33 percent ($3,000) on contract signing, 33 percent ($3,000) on design approval, and 34 percent ($3,060) on final launch. This milestone-based approach aligns payment directly with deliverables, giving the client natural checkpoints and giving the agency leverage to pause work if an installment is missed. It also means the agency is never more than one phase ahead of its receivables.

Consultants and Business Advisors

For a six-month advisory engagement billed at $2,500 per month, the plan is essentially a recurring billing arrangement rather than a traditional installment plan. The distinction matters: recurring billing reflects ongoing service delivery with no defined total, while an installment plan applies to a defined project amount split over time. Consultants working on defined deliverable packages, a market entry strategy, a financial model, or an operations audit typically use true installment billing with a front-loaded payment structure.

Landscaping and Home Services

For a $15,000 landscape design and installation project, a three-payment structure is common in the trades: 40 percent on contract ($6,000), 35 percent at midpoint ($5,250), and 25 percent on completion ($3,750). The first payment covers materials; the second funds the bulk of the labor; the final payment is withheld until the client signs off. This structure protects both parties and is widely understood as an industry standard.

Professional Training and Coaching

Coaches and trainers offering multi-session programs often split payment into two or three installments aligned with the program’s phases. A 12-week executive coaching program at $6,000 might invoice at weeks one, five, and nine. The key here is to automate the invoice delivery and payment collection so that the client’s payment never depends on the coach remembering to send an invoice at the right time.

Key Benefits of Offering Payment Plans

The benefits of a well-run payment plan program extend well beyond the immediate transaction. Here is what the data and experience consistently show.

Higher close rates on large contracts.

Price is the most common objection in service sales. Structured payment plans address the objection without discounting the work. Businesses that offer flexible payment options consistently report shorter sales cycles on high-ticket engagements.

More predictable revenue.

When clients are on defined payment schedules, you can forecast the next 60 to 90 days of cash inflow with reasonable accuracy. This predictability makes everything from payroll planning to investment decisions more straightforward. It is one of the reasons many businesses actively prefer payment-plan clients to lump-sum payers, the revenue is visible in advance.

Stronger client relationships.

Clients who feel that a business accommodated their financial reality tend to be more loyal, more communicative, and more likely to provide referrals. Payment flexibility signals confidence in the relationship rather than anxiety about getting paid.

Lower cost of customer acquisition.

Expanding a relationship with an existing client who is already on a payment plan is almost always cheaper than acquiring a new one. If the payment plan experience is smooth, invoices arrive on time, payment is easy, and the client can see their remaining balance in a self-service portal, and renewal and upsell conversations become natural.

Reduced need for external financing.

Some businesses turn to invoice factoring or lines of credit to manage cash flow gaps. A deposit-anchored payment plan effectively eliminates most of those gaps internally, without the cost of external borrowing.

Risks and Things to Watch For

⚠ No Written Agreement

Verbal payment arrangements create serious risk. Without a signed document specifying the total amount, payment schedule, late fee policy, and default terms, you have very little recourse if a client decides to dispute the arrangement. Always formalize the plan in writing before any work begins.

⚠ Skipping the Deposit

Allowing a client to start a plan with no upfront payment is one of the most common, and costly, mistakes in service billing. Without a deposit, the client has no skin in the game and significantly less incentive to follow through. It also means you absorb 100 percent of the credit risk from day one.

⚠ Extending Plans Too Long Without Automation

A six-month or twelve-month payment plan managed manually is a recipe for missed invoices, inconsistent follow-up, and growing accounts receivable. If you cannot automate the collection workflow, keep the plan short or limit who you offer it to. Automated collection tools solve this problem entirely by handling reminders and failed payment retries on schedule, without human involvement.

⚠ Poor Visibility Into Outstanding Balances

If you cannot answer the question “who owes me money and how much?” in under 60 seconds, your accounts receivable management is fragile. Tracking payment plan balances in a spreadsheet works for two or three clients but breaks down quickly at scale. A centralized customer management system that surfaces outstanding balances, payment history, and upcoming installments in a single view is not a luxury, it is a baseline operational requirement.

⚠ Not Accounting for Soft Costs

Offering a payment plan has real costs beyond the obvious risk of non-payment. The time spent setting up the plan, monitoring it, following up on late payments, and handling exceptions all add up. Make sure your pricing reflects these operational costs, particularly for longer-term arrangements.

Payment Plans vs. Related Concepts

Payment plans overlap with several related billing and financing concepts. The distinctions between them matter, both for how you set them up and how clients interpret them.

| Concept | How It Works | Defined Total? | End Date? | Interest / Fees? | Best Used For |

|---|---|---|---|---|---|

| Payment Plan (Installment Billing) | Fixed total split into a set number of scheduled payments | Yes | Yes | Optional | Large one-time projects or purchases |

| Recurring Billing | Ongoing charges on a repeating schedule; no defined total or end date | No | No (until cancelled) | No | Subscriptions, retainers, monthly services |

| Buy Now Pay Later (BNPL) | Third-party provider finances the purchase; business is paid upfront | Yes | Yes | Sometimes (paid by customer) | Consumer retail; point-of-sale conversion |

| In-House Financing | Business extends credit directly, sometimes with formal loan terms | Yes | Yes | Yes (typically) | High-value B2B or B2C with longer time horizons |

| Invoice Factoring | Third party buys your unpaid invoices at a discount for immediate cash | Yes | Yes | Yes (discount fee) | Improving seller’s immediate cash flow, not buyer’s |

| Deferred Payment Terms (Net 60/90) | Full payment due at a future date; no splitting of the amount | Yes | Yes | Typically no | B2B procurement with long accounts payable cycles |

The practical takeaway from this comparison is that installment billing is the right tool for defined, finite transactions, a project, a purchase, or a fixed-scope engagement. For ongoing service relationships with no defined end point, recurring billing is the more appropriate structure. Many businesses use both models simultaneously depending on the client and engagement type, and the right billing platform can handle both from a single interface.

How to Get Started: Building Your First Payment Plan System

Moving from ad-hoc payment arrangements to a structured, automated payment plan program takes some upfront setup, but the investment pays back quickly in reduced administrative time and more consistent cash flow. Here is a practical path forward.

1. Define Your Offering Before You Present It to Clients

Decide in advance which services or transaction sizes qualify for a payment plan, how many installments you will allow, whether you will charge a financing fee, and what your deposit minimum is. Having these parameters decided before the conversation means you are not improvising terms under sales pressure, which is a common source of payment plan problems.

2. Create a Standard Payment Plan Agreement Template

Your agreement should cover the total amount, installment amounts and due dates, deposit requirement, accepted payment methods, late fee policy, what constitutes default, and any service delivery implications of non-payment. Your legal or accounting advisor can review it once, and then you can reuse it for every client with minimal customization.

3. Set Up Installment Billing in Your Invoicing System

Configure your installment billing schedule in your billing software before the work starts, not after. Pre-generate all invoices in the plan so the client receives the full schedule upfront, this dramatically reduces surprise or dispute at later installment dates. With ReliaBills, you can calculate each installment based on the principal, any financing fees, down payment amount, and number of payments, then set the delivery frequency in a few clicks.

4. Collect and Securely Store the Client’s Payment Method

The cleanest payment plan experience for both parties is one where the client stores a card or bank account on file and payments are processed automatically on each due date. This removes the friction of the client needing to actively pay each invoice and eliminates the most common cause of unintentional late payment. Make sure your billing platform is PCI-compliant and that stored payment credentials are tokenized, never stored in plain text.

5. Configure Automated Reminders and Failed Payment Workflows

Set up at least two reminder touchpoints per installment: one three to five days before the due date and one on the day of (for clients paying manually). For automated payments, configure a failed payment retry and a client notification that goes out immediately if a transaction fails. A structured collection automation workflow handles all of this without any manual involvement once it is set up.

6. Give Clients Self-Service Visibility Into Their Plan

One of the most effective ways to reduce inbound client questions about payment plans is to give clients access to a portal where they can see their full installment schedule, remaining balance, payment history, and upcoming due dates at any time. A client portal reduces the volume of “How much do I still owe?” calls to near zero and signals to clients that you run a professional, transparent operation, which, in turn, builds the trust that leads to on-time payment.

7. Review Your Receivables Weekly

Automation handles the routine, but a weekly review of outstanding balances keeps you informed of any accounts that need a human touch. Look for clients who are two or more days past due on an installment, who have had a payment fail and not yet updated their billing info, or whose plan is approaching a milestone where a conversation about renewal or next steps might be valuable. Good customer data management makes this review a five-minute task rather than a time-consuming reconciliation exercise.

Where to Go Next on ReliaBills: Once your payment plan workflow is running smoothly, explore how recurring billing handles ongoing service relationships alongside your installment plans and how the collection automation and customer portal features work together to create a billing experience your clients will actually appreciate.

Frequently Asked Questions

1. What is a payment plan?

A payment plan is a formal agreement between a business and a customer that divides a total balance into a series of scheduled payments over a defined period. The payments can be equal installments or variable amounts, and the arrangement may be interest-free or include a financing fee depending on the duration and the parties’ agreement.

2. How do I offer payment plans without hurting my cash flow?

The four key safeguards are collecting a meaningful upfront deposit (at least 25 percent), automating payment collection so no installment is ever forgotten; charging a financing fee on longer plans to compensate for deferred revenue, and maintaining real-time visibility into outstanding balances so you can identify problems before they grow. A billing platform that handles the collection workflow automatically removes most of the cash flow risk from payment plan management.

3. What is the difference between a payment plan and recurring billing?

A payment plan, also called installment billing, applies to a defined total amount split into a fixed number of payments with a clear end date. Recurring billing charges an ongoing fee for a continuing service on a repeating schedule with no predetermined end. Both can be automated, but they serve very different business models and client relationships.

4. Should I charge interest or a financing fee on payment plans?

For short plans, two to four payments over 60 days or less, offering interest-free terms is a standard sales incentive and rarely hurts your economics. For longer arrangements extending three to twelve months, a financing fee of one to three percent of the total is appropriate and widely accepted by clients. Make the fee explicit in the agreement rather than embedding it invisibly in your price.

5. What happens if a customer misses a payment?

Your written agreement should specify a grace period (five to seven business days is typical), an automatic late fee after that window, and the right to pause service delivery or demand the remaining balance in full after two consecutive missed payments. Automated billing software handles the notification and retry workflow; your job is to define the policy upfront so it is enforced consistently and without awkwardness.

6. Can small businesses offer payment plans?

Absolutely, payment plans are not exclusive to large enterprises or financial institutions. Any service business can structure installment arrangements regardless of size. The key enabling factor is having a billing system that automates the workflow, because managing multiple payment plans manually becomes unworkable quickly. Modern invoicing software makes this accessible to even solo operators.

7. How many installments should a payment plan have?

For most service transactions, three to six installments is the practical sweet spot. Fewer installments are easier to manage and carry less risk; more are sometimes necessary for larger contracts but should be paired with tighter automation and stronger default terms. Plans exceeding six months should almost always include a financing fee to account for the extended exposure.

8. Do I need software to offer payment plans?

Not strictly, but trying to manage multiple client payment plans in a spreadsheet is one of the fastest ways to create cash flow problems. Automated installment billing eliminates missed invoices, inconsistent follow-up, and manual tracking errors. The time savings alone typically justify the cost of billing software within the first month of managing more than two or three active plans simultaneously.

Closing Thoughts

The businesses that struggle with payment plans are almost always the ones that offer them reactively, under sales pressure, without a written agreement, without a deposit, and without any automation to support collection. The businesses that thrive with payment plans design them intentionally: fixed terms, upfront deposits, automated invoicing, and clear policies for what happens when something goes wrong.

Done right, offering payment plans is not a concession to clients who cannot afford your work. It is a structural decision to meet clients where they are financially, capture deals you would otherwise lose, and build a more predictable revenue stream in the process. The cash flow protection comes not from demanding full payment upfront, but from designing a system that ensures every installment arrives reliably, on time, automatically, without friction on either side.

Recent Articles:

- Installment Billing for Service Businesses: A Practical Guide

- Proforma Invoice vs Commercial Invoice: When to Use Each

Brant Pallazza is the Founder and President of ReliaBills, an invoicing and recurring billing platform built to help small businesses secure predictable cash flow. With over 20 years of experience in direct response marketing and e-commerce leadership, including a 13-year tenure managing over $500 million in gross sales at Digital River. Brant writes actionable guides on automated billing, payment processing, and scaling SMBs.