Maintaining healthy cash flow is one of the most common and persistent challenges faced by growing businesses, especially those scaling operations or managing high volumes of customer transactions. Even profitable companies can struggle with liquidity when payments from customers are delayed, creating gaps that disrupt daily operations. To address this issue, many businesses turn to external financing options to stabilize their cash position and maintain momentum.

Two of the most widely used financing solutions are invoice discounting and traditional business loans, each offering distinct advantages depending on the situation. While both provide access to capital, they operate differently in terms of structure, repayment, and impact on financial health. Understanding these differences is essential for making informed financial decisions that align with business goals.

Choosing between invoice discounting vs business loan options requires a clear understanding of when each method is most effective. Businesses that evaluate their cash flow patterns, receivables, and long-term financial strategy are better positioned to select the right solution. Making the correct choice can significantly improve financial flexibility, reduce risk, and support sustainable growth.

What Is Invoice Discounting?

Invoice discounting is a form of receivables financing that allows businesses to unlock cash tied up in unpaid invoices before customers settle their balances. Instead of waiting for payment terms that may extend 30, 60, or even 90 days, businesses can access a percentage of the invoice value almost immediately. This approach helps bridge cash flow gaps without interrupting operations or delaying critical expenses.

One of the defining characteristics of invoice discounting is that businesses retain control over their customer relationships and collections process. Unlike factoring, where a third party may interact directly with customers, invoice discounting operates in the background. This makes it an attractive option for companies that want to maintain professionalism and consistency in client communications.

By leveraging outstanding receivables, businesses can create a more flexible financing model that scales with their revenue. As invoice volume increases, so does the available funding, making it particularly useful for companies experiencing rapid growth. This dynamic funding approach is a key reason why many businesses prefer invoice discounting over more rigid financing options.

What Is a Business Loan?

A business loan is a traditional financing method where a lender provides a lump sum of capital that must be repaid over a predetermined period with interest. These loans can come from banks, credit unions, or alternative lenders, and they often require a formal application process. Approval is typically based on creditworthiness, financial history, and the overall stability of the business.

Repayment terms for business loans are usually fixed, meaning businesses must make regular payments regardless of their cash flow situation. Interest rates can vary depending on risk factors, loan size, and market conditions, which can impact the total cost of borrowing. While predictable, these obligations can create pressure during periods of low revenue or unexpected expenses.

Business loans are commonly used for long-term investments such as expansion projects, equipment purchases, or large operational upgrades. They provide upfront capital that can be deployed immediately for strategic initiatives. However, they may not always be the best solution for short-term cash flow gaps or businesses with fluctuating income cycles.

Key Differences Between Invoice Discounting and Business Loans

Source of funding: invoices vs lender capital

Invoice discounting relies on a company’s existing receivables as the primary source of funding, making it directly tied to sales activity. In contrast, business loans are funded by lenders based on credit assessments and financial evaluations. This difference means invoice discounting is more accessible for businesses with strong sales but limited credit history.

Approval criteria: receivables vs creditworthiness

Approval for invoice discounting is largely based on the quality and reliability of outstanding invoices and customer payment history. Business loans, on the other hand, require strong credit scores, financial statements, and sometimes collateral. This makes loans more restrictive for newer or rapidly growing businesses.

Repayment structure: customer payments vs fixed installments

With invoice discounting, repayment occurs naturally when customers pay their invoices, reducing the need for separate repayment schedules. Business loans require fixed monthly installments regardless of incoming cash flow. This structural difference significantly impacts financial flexibility and risk exposure.

Impact on balance sheet

Invoice discounting is often considered off-balance-sheet financing, depending on the structure, which can help maintain healthier financial ratios. Business loans are recorded as liabilities, increasing debt levels and potentially affecting borrowing capacity. This distinction is important for businesses managing financial reporting and investor expectations.

Speed of access to funds

Invoice discounting typically provides faster access to cash since it leverages existing invoices rather than requiring lengthy approval processes. Business loans may take weeks or even months to process due to documentation and underwriting requirements. Speed can be a critical factor when immediate liquidity is needed.

When Should a Business Use Invoice Discounting?

When experiencing cash flow gaps due to slow-paying customers

Businesses that regularly deal with delayed payments can benefit significantly from invoice discounting. It allows them to maintain operations without waiting for customers to settle invoices. This ensures continuity and reduces financial stress caused by inconsistent cash inflows.

When holding a large volume of unpaid invoices

Companies with substantial receivables can unlock significant working capital through invoice discounting. Instead of letting invoices sit unpaid, they can convert them into immediate cash. This improves liquidity and supports ongoing business activities.

When needing quick access to working capital

Invoice discounting offers rapid funding, making it ideal for urgent financial needs. Businesses can cover payroll, supplier payments, or operational costs without delays. This agility is especially valuable in fast-paced industries.

When wanting to avoid taking on additional debt

Since invoice discounting is not a traditional loan, it does not add long-term debt to the balance sheet. This helps businesses maintain healthier financial ratios and borrowing capacity. It is an attractive option for companies aiming to stay lean financially.

When maintaining control over customer relationships is important

Businesses that prioritize direct communication with clients prefer invoice discounting over factoring. It allows them to handle collections internally without third-party involvement. This helps preserve trust and brand reputation.

When Is a Business Loan the Better Option?

When funding long-term investments or expansion

Business loans are ideal for large-scale projects that require significant upfront capital. These include opening new locations, purchasing equipment, or investing in infrastructure. The structured repayment aligns with long-term growth plans.

When predictable repayment schedules are preferred

Fixed installment payments make it easier to plan budgets and manage finances. Businesses can forecast expenses accurately and maintain financial discipline. This predictability is beneficial for stable companies with consistent revenue.

When there are limited receivables to leverage

Companies with low invoice volume may not benefit from invoice discounting. In such cases, business loans provide an alternative funding source. This ensures access to capital even without strong receivables.

When businesses qualify for favorable loan terms

Established businesses with strong credit profiles may secure loans with competitive interest rates. This can make loans more cost-effective over time. Lower borrowing costs can improve overall financial efficiency.

When capital is needed upfront in a lump sum

Certain expenses require immediate and full funding, which loans are designed to provide. Invoice discounting, being tied to invoices, may not meet such needs. Loans offer the flexibility to deploy capital instantly for major initiatives.

Advantages of Invoice Discounting

Faster access to funds compared to traditional loans

Invoice discounting enables businesses to access cash quickly, often within days of issuing invoices. This speed helps address urgent financial needs without lengthy approval processes. It supports smoother day-to-day operations.

Flexible financing based on invoice value

Funding grows alongside sales, making it a scalable financing option. Businesses can access more capital as they generate more invoices. This flexibility aligns with growth and demand fluctuations.

No need for additional collateral in many cases

Since invoices act as the primary asset, additional collateral is often unnecessary. This reduces risk for business owners and simplifies the application process. It also makes financing more accessible.

Scales with business growth

As revenue increases, so does the availability of funding through invoice discounting. This creates a dynamic financing model that adapts to business expansion. It supports sustainable growth without added financial strain.

Maintains customer relationship control

Businesses retain full control over communications and collections. This ensures consistency in customer interactions and preserves brand reputation. It is particularly important for service-based industries.

Advantages of Business Loans

Fixed repayment structure for easier budgeting

Predictable payments allow businesses to manage finances with greater accuracy. This helps maintain stability and avoid unexpected financial strain. Budgeting becomes more straightforward and reliable.

Suitable for large, one-time investments

Loans provide substantial capital for major expenses. This makes them ideal for expansion, equipment, or infrastructure projects. Businesses can execute strategic initiatives without delays.

Potentially lower cost for long-term financing

In some cases, loans may offer lower overall costs compared to short-term financing options. This is especially true for businesses with strong credit. Lower interest rates can improve profitability.

Builds business credit history

Timely loan repayments contribute to a stronger credit profile. This can improve access to future financing opportunities. A solid credit history enhances financial credibility.

Predictable financing terms

Loan agreements clearly outline repayment schedules, interest rates, and terms. This transparency helps businesses plan effectively. It reduces uncertainty in financial management.

Risks and Considerations

Invoice discounting fees and service costs

While convenient, invoice discounting comes with fees that can add up over time. Businesses must evaluate whether the cost aligns with the benefits. Careful analysis ensures profitability is maintained.

Dependence on customer payment behavior

Funding relies on customers paying invoices on time. Delays or defaults can impact cash flow and financing availability. This introduces a level of dependency on external parties.

Loan interest rates and long-term obligations

Business loans require ongoing repayments with interest. This can become burdensome if revenue fluctuates. Long-term commitments must be carefully managed.

Risk of over-leveraging finances

Taking on too much financing can strain resources. Businesses must balance borrowing with their ability to repay. Over-leveraging increases financial risk.

Impact on cash flow and financial planning

Both financing options affect cash flow differently. Businesses must understand these impacts before committing. Strategic planning is essential for maintaining stability.

How Recurring Invoices Strengthen Invoice Discounting

Recurring invoices create a steady and predictable stream of receivables, which is highly attractive to lenders and financing providers. Consistency in billing demonstrates reliability and reduces perceived risk. This improves the likelihood of approval for invoice discounting facilities.

Regular invoicing also builds a strong payment history, which enhances credibility. Businesses that consistently generate and collect invoices are seen as financially stable. This can lead to better financing terms and higher funding limits.

Additionally, recurring invoices simplify financial forecasting and planning. They provide clear visibility into expected cash inflows. This strengthens overall financial management and decision-making.

The Role of Automation in Financing Readiness

Automation ensures invoices are generated accurately and on time, reducing the risk of errors that could impact financing eligibility. It eliminates manual processes that often lead to inconsistencies. This improves overall data quality and reliability.

Real-time tracking of payments and receivables provides better financial visibility. Businesses can monitor cash flow and identify potential issues early. This transparency is crucial when working with lenders or financing providers.

Automated systems also enhance reporting capabilities, making it easier to present financial data. Accurate reports build trust and credibility with stakeholders. This strengthens a business’s position when seeking financing.

Best Practices for Choosing the Right Financing Option

Evaluate short-term vs long-term financial needs

Understanding whether the need is immediate or strategic helps determine the right option. Invoice discounting suits short-term gaps, while loans support long-term goals. Clear assessment ensures better financial alignment.

Assess current cash flow and receivables volume

Businesses should analyze their cash flow patterns and outstanding invoices. High receivables may favor invoice discounting. Accurate evaluation leads to smarter financing decisions.

Compare costs, fees, and repayment terms

Each option comes with different cost structures. Businesses must calculate total expenses and long-term impact. Comparing these factors ensures cost-effective choices.

Consider impact on business operations and growth

Financing should support, not hinder, operations. Businesses must evaluate how each option affects flexibility and scalability. The right choice enables sustainable growth.

Use financial data and reporting for informed decisions

Accurate financial data is essential for evaluating options. Reports provide insights into performance and risks. Data-driven decisions improve financial outcomes.

Key Benefits of Choosing the Right Financing Method

Improved cash flow management

Selecting the right financing option ensures consistent cash availability. This supports daily operations and reduces financial stress. Strong cash flow management is critical for growth.

Reduced financial risk

Proper financing minimizes exposure to unnecessary debt or costs. Businesses can maintain stability and avoid financial strain. Risk management becomes more effective.

Better alignment with business goals

Financing should align with strategic objectives. The right choice supports expansion, efficiency, or stability. Alignment drives long-term success.

Increased operational flexibility

Flexible financing allows businesses to adapt to changing conditions. This improves resilience in dynamic markets. Agility becomes a competitive advantage.

Stronger financial stability

Well-managed financing contributes to overall stability. Businesses can plan confidently and invest strategically. Stability supports sustained growth.

Common Use Cases

SaaS and subscription-based businesses

These businesses rely heavily on recurring invoices, making invoice discounting highly effective. Predictable revenue streams support consistent financing. It enhances scalability and growth potential.

Logistics and freight companies

Long payment cycles make cash flow management challenging. Invoice discounting provides quick access to funds. This ensures smooth operations and timely deliveries.

Manufacturing and wholesale businesses

Large order volumes often result in delayed payments. Invoice discounting helps maintain production and supply chains. It supports operational continuity.

Service-based businesses with recurring clients

Regular billing creates stable receivables. This improves eligibility for invoice discounting. It ensures consistent cash flow.

Growing startups managing cash flow gaps

Startups often face irregular cash flow. Invoice discounting provides flexible funding without adding debt. It supports early-stage growth.

How ReliaBills Supports Invoice Discounting and Cash Flow Management

Modern businesses need more than just invoicing—they need intelligent systems that enhance visibility, accuracy, and financial control. ReliaBills simplifies invoice creation, ensures consistent documentation, and reduces manual errors that can impact financing opportunities. By digitizing billing processes, businesses gain better oversight of receivables and cash flow patterns. This foundation makes it easier to evaluate financing options like invoice discounting vs business loan strategies.

One of the standout advantages of ReliaBills is its recurring billing capability, which helps businesses generate consistent and predictable invoices automatically. These recurring invoices create a reliable stream of receivables, strengthening eligibility for invoice discounting and improving lender confidence. Automation ensures invoices are sent on time, reducing delays and improving payment cycles. This consistency plays a crucial role in maintaining strong financial health and financing readiness.

For businesses looking to scale, ReliaBills PLUS offers advanced features such as customizable templates, detailed reporting, and centralized document management. These tools provide deeper insights into financial performance and streamline audit preparation. Enhanced automation reduces administrative workload while improving compliance and accuracy. With these capabilities, businesses can confidently manage invoicing and position themselves for smarter financing decisions.

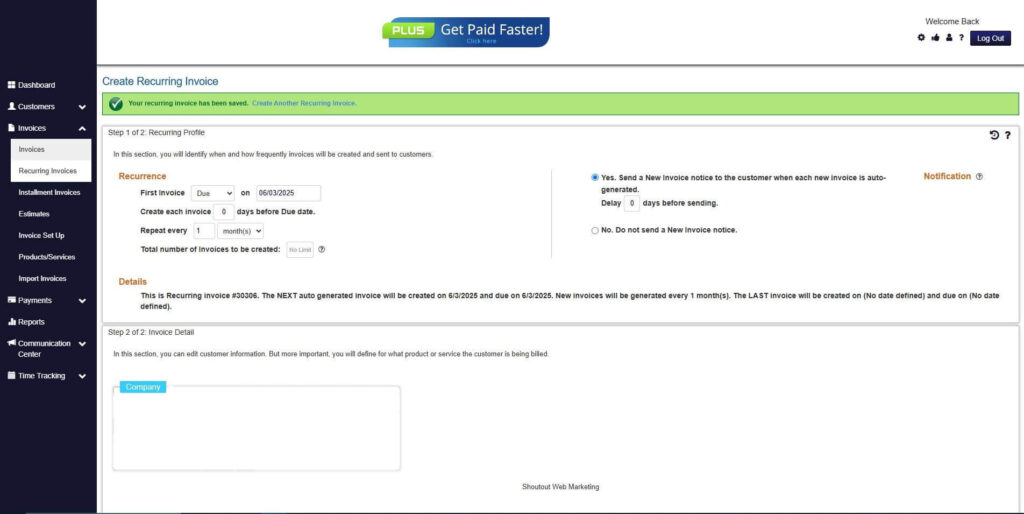

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

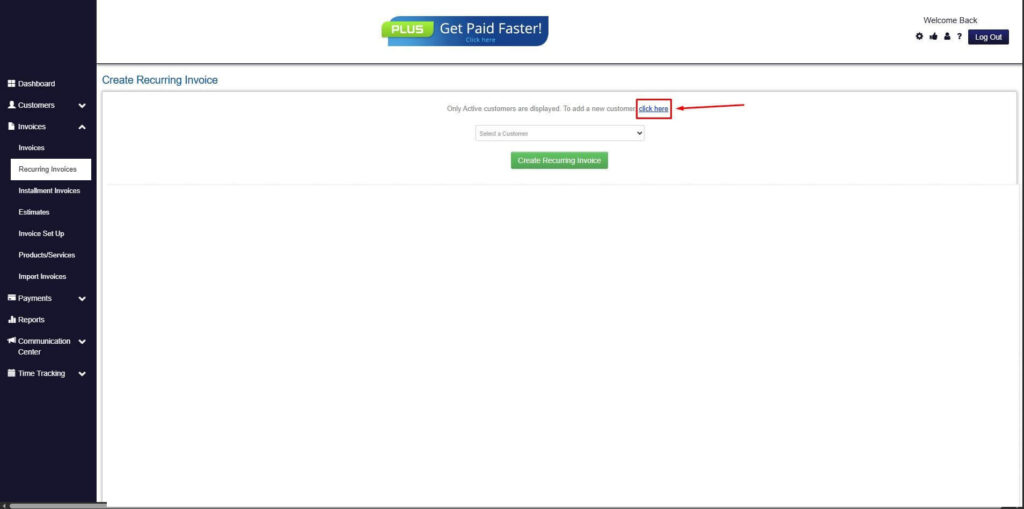

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

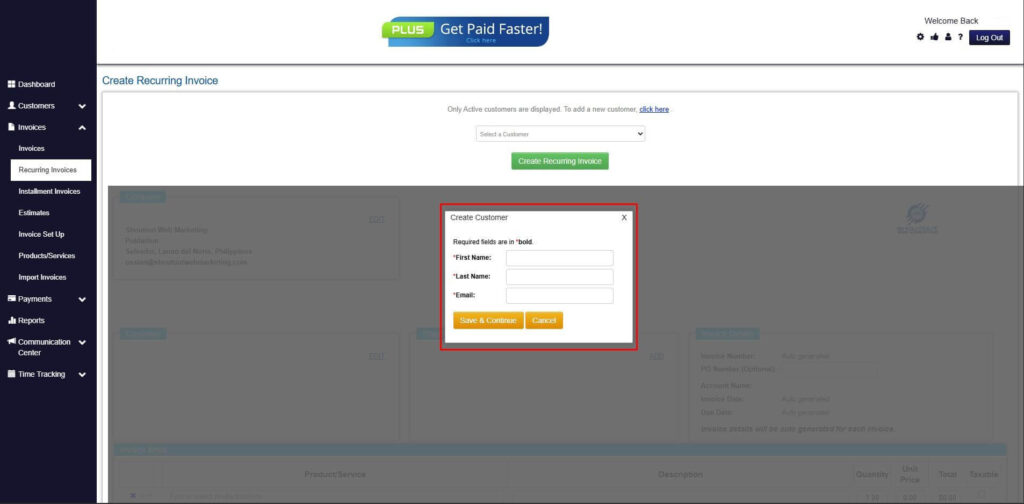

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

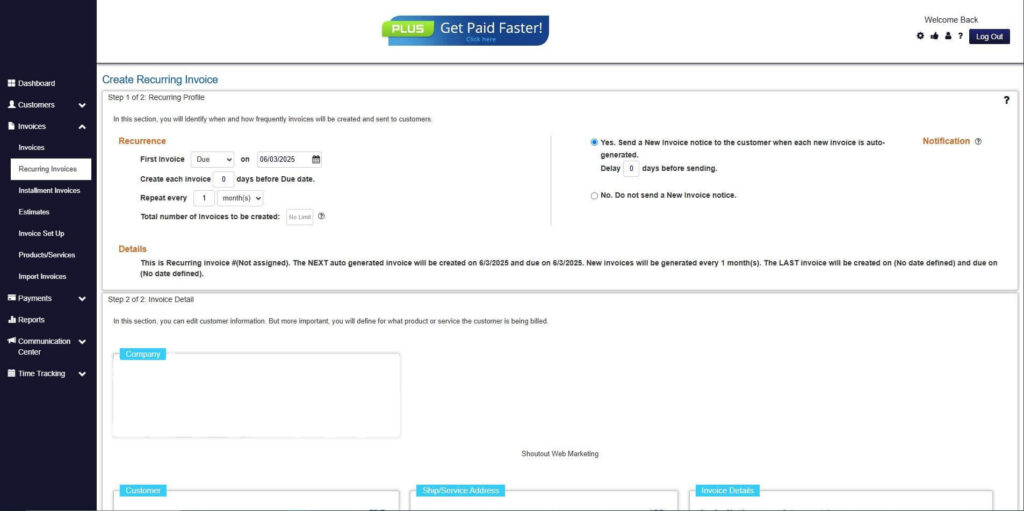

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

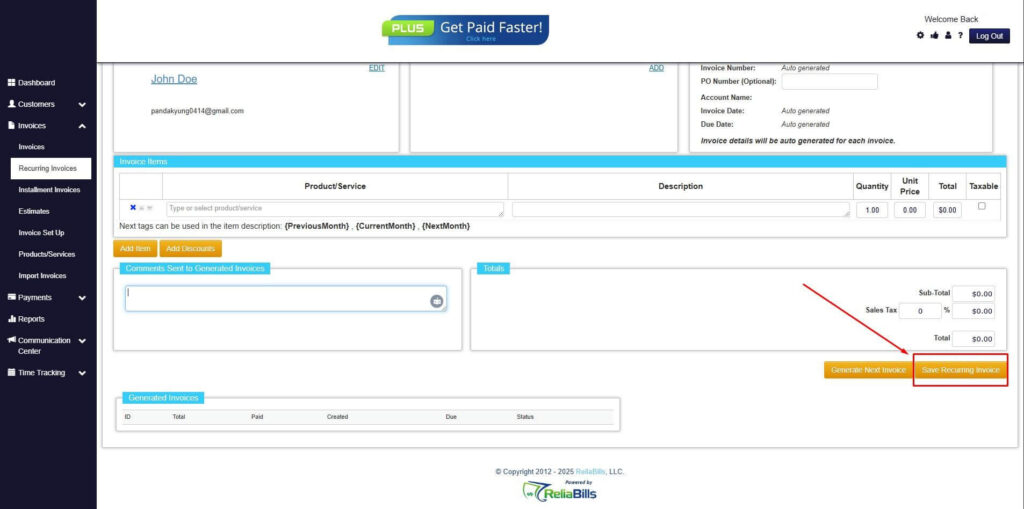

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

- Your Recurring Invoice has been created.

Frequently Asked Questions (FAQs)

1. What is invoice discounting?

Invoice discounting is a financing method that allows businesses to access cash from unpaid invoices. It helps improve cash flow without waiting for customer payments. Businesses retain control over collections.

2. Is invoice discounting better than a loan?

It depends on the business’s needs and financial situation. Invoice discounting is ideal for short-term cash flow gaps, while loans suit long-term investments. Each has its advantages.

3. Can small businesses use invoice discounting?

Yes, many providers offer solutions tailored for small businesses. Eligibility depends on invoice quality and customer reliability. It is a flexible option for growing companies.

4. What are the risks of business loans?

Loans require fixed repayments and may include high interest costs. They can strain cash flow if not managed properly. Businesses must evaluate their ability to repay.

5. How do recurring invoices support financing?

Recurring invoices create consistent revenue streams and improve financial predictability. This strengthens lender confidence and financing eligibility. It supports better financial planning.

Conclusion

Understanding the differences between invoice discounting vs business loan options is essential for making informed financial decisions. Each method serves a specific purpose, and the right choice depends on factors such as cash flow needs, business goals, and financial structure. Businesses that carefully evaluate their situation can select the most effective financing solution.

Accuracy, planning, and financial visibility play a critical role in maximizing the benefits of any financing method. Whether leveraging receivables or securing a loan, maintaining strong financial practices ensures stability and growth. Poor decisions, on the other hand, can lead to unnecessary costs and risks.

As businesses continue to evolve, adopting digital tools and automation becomes increasingly important. Solutions like recurring billing and automated invoicing help improve cash flow, reduce errors, and enhance financing readiness. By embracing these strategies, businesses can position themselves for long-term success and financial resilience.