If you run a business, you need to know how to prepare three financial statements: a balance sheet, statement of cash flows, and an income statement. For this article, we’re going to learn how to prepare an income statement.

The income statement is another term for a business’s profit and loss statement. It showcases the profitability of the firm over a given period. To set-up your income statement, you need first to choose a particular time frame. It could be the current month, a quarter, or an entire year’s worth of accumulated financial statements.

How to Prepare Your Income Statement

To help you learn more about the steps in creating an income statement, we’ve created a list of items below. These items present a line-by-line explanation of every element that comprises an income statement. That way, you can look at the profit or loss after deducting each of these expenses. Without further ado, let’s begin:

Line no. 1:

The first line item shows the sales figures, also known as the gross revenue. It represents the total amount of sales that the business has made over a given income statement period. For example, if your business managed to sell $50,000 perfumes at $20, you would present $1,000,000 on the sales line. It’s essential to display the amount sold, even if you’ve already billed your customers but haven’t collected the money yet.

Line no. 2:

The second line item will have a $500,000 entry for the cost of goods sold. This particular cost of goods sold is usually a firm’s largest expense. It contains all the costs directly related to producing your products, such as purchases of raw materials and direct labor.

If you purchase wholesale goods then resell them, the earnings will also reflect on this line. For example, $50,000 perfumes purchased at a wholesale cost of $10.00 each equals $500,000 cost of goods sold during the period reflected in the income statement.

Line no. 3:

The third line item covers the gross profit. To get this number, you will need to subtract the cost of goods sold from the gross sales.

Line no. 4:

The fourth line item covers the selling and administration expenses (SG&A). This item represents $250,000, covering your office expenses, such as the costs not directly related to the sale or producing goods. For example, if you have several related expenses, such as electricity, internet, and water bills, you can group them into a single line and label them as “utilities.”

Other expenses that fall under SG&A include costs like office rent, sales commissions, legal accounting fees, and employee wages. It can also include other metrics like tax income, operating expenses, selling and administrative expenses, the overall cost of operations, income tax, operating income, and more. These can be placed in separate revenue line items or as a collective group. Your operating expenses, for example, are placed in a separate line item.

Line no. 5:

The fifth line item represents the company’s depreciation expense. When you buy equipment or a building for your business, it will depreciate over a given timeframe. Depreciation is considered a non-cash expense that helps you with sheltering your taxes. That’s why it is also shown on the income statement.

Line no. 6:

The sixth line item covers operating profit, referred to as “EBIT” (Earnings Before Interest and Taxes. To get this number, you’ll need to subtract selling and administrative expenses from depreciation. Using the last example, the operating costs would equate to $170,000.

Line no. 7:

The seventh line item covers the interest expense. Interest is the amount that you pay on any debt your company owes to an external source. To calculate the interest on the debt, you’ll have to determine the interest rate that you are paying. Multiply it by your principal debt. For the example used in this article, the interest amount is assumed $30,000 and goes on this line.

Line no. 8:

After you subtract your interest expense from the EBIT, you’ll arrive at earnings before taxes on this line.

Line no. 9:

For this line, you’ll need to fill in the amount you paid in the state, federal, local, and payroll taxes. For this example, the tax rate will be 21%.

Line no. 10:

After subtracting the tax expense, you will arrive at the earnings that are immediately available to your common shareholders. This amount will be placed on this line.

Line no. 11:

Do you have investors in your company? Are you taking a salary from your firm? If your answer to all of this is ‘Yes,’ this line will serve as the place where you record the draw or the dividends.

Line no. 12:

The last and final line will cover your company’s net income, otherwise known as profit. To do so, subtract the cost and all of the expenses starting line 3 (gross profit). Your profit is the final number after deducting all of the numbers above. It represents the money you have left. You can put it back or reinvest it into the firm. This process is called retained earnings.

Once you’ve calculated everything, transfer the net income amount to your balance sheet at the end of your accounting period and into the retained earnings account. Aside from your net profit being reinvested back into the company, it might also be used to pay future dividends to your investors.

Income Statement Sample

Using the example amounts that we used, we’ve created a table representing a simplified income statement. An income statement might look a bit more complex as it will contain more line items. However, this basic income statement should serve to give you the fundamental layout and idea of how a profit/loss statement works:

ABC Company Income Statement for the Year Ending December 31, 2021.

- Sales – $1,000,000.00

- Cost of Goods Sold – $500,000.00

- Gross Profit – $500,000.00

- Selling and Administrative Expense – $250,000.00

- Operating Profit (EBIT) – $170,000.00

- Depreciation – $80,000.00

- Earnings Before Taxes (EBIT) – $140,000.00

- Interest – $30,000.00

- Taxes (21%) – $29,400.00

- Earnings Available to Common Shareholders – $110,000.00

- Dividends or Owner Draw – $20,000.00

- Net Income – $90,600.00

No matter how many line items your income statement will have, it will always have the core line items such as gross profit, operating expenses, tax income, cash flow statement, menu income statement, cost of goods sold (if applicable), and net income. You can also add in expense accounts, among other components of your statement income.

Your accounting system will be able to track other metrics like interest income, business operations expenses, revenue, goods, sales revenue, tax rate, and more. Most of these items will be placed in your income statement line items and your financial report. Most big-name companies have very complex income statements, which is something you’ll need to incorporate as your business grows.

How to Write an Income Statement

Now that you know the elements included in a financial statement, otherwise known as the income statement, it’s time to learn how to write one. While there are plenty of income statement template samples available online, it will still be essential to be familiar with each part. That way, you can still write your income statement when a template isn’t available.

Step 1: Choose a Specific Period

Income statements usually measure revenues and expenses in a span of a certain period throughout the year. It’s typically generated monthly, quarterly, or annually. Before you start calculating your income statement, you’ll need to choose the duration you want to use.

Step 2: Write the Income Statement Header

Write your company name at the very top of the document. In the line beneath it, write the words, “Income Statement.” On the third and next line, write the period of the time that the income statement covers. For example, if it’s yearly, the usual date you need to place on your income statement would be December 31, [Year].

Step 3: Format the Body of the Income Statement

Keep in mind that income statements usually have four notable sections.

- The first section calculates the total amount of the money made, from the cost of goods sold to sales revenue. In other words, it’s called the gross profit.

- The second section calculates your total operational expenses.

- The third section calculates profits and losses that are not related to your operational costs.

- The fourth section calculates the money that you’ve made in profit after subtracting all of your expenses from your revenue. This number is also called your net profit or net income.

Automate Your Billing and Make Your Life Easier

Whether you need to create an income statement or want to send out a regular invoice to your customer, you need to start automating your entire billing process. It might be a daunting idea to some, but automating your business is absolutely crucial and game-changing in today’s fast-paced world. That’s why you need to start embracing automating, starting with your billing strategy.

By automating your invoice through a recurring billing software like ReliaBills, you can create a better and more accurate income statement whenever you need to. Recurring billing will keep track of your recurring transactions based on recurring schedules. Automating your recurring billing strategy will make it easier for you to reconcile and process payments, allowing you to focus on other areas of business instead.

Recurring Billing Improves Your Cash Flow

By using recurring billing software like ReliaBills, businesses can benefit by having their invoices automatically sent out, and payments automatically received. In addition, with recurring billing, you spend less time processing your invoices manually, which is why it can help improve your cash flow in the long run.

Recurring billing helps businesses retain customers through convenience for recurring transactions like monthly subscriptions or automatic bill payment services. In addition, recurring billing makes processes easier for business owners, who can now focus on other parts of their business.

Recurring billing is beneficial for businesses big and small because recurring transactions are commonplace in many industries today- from technology to entertainment; most companies use recurring billing to handle monthly payments automatically.

Why Switch To Recurring Billing?

Traditional invoicing and recurring billing strategies are effective in their ways, but recurring billing can be even more beneficial to your business.

Recurring billing software like ReliaBills is a good solution for businesses that use recurring transactions on a regular basis because it will allow you to save time by processing recurring transactions automatically without having to handle them yourself manually.

Recurring billing is a widely used method that helps businesses increase recurring revenue and streamline processes. Recurring transactions like monthly payments and subscriptions are becoming commonplace in many industries today, which is why recurring billing can help you stay ahead of the curve when it comes to your recurring revenue model.

Get Started Today!

If you’re planning to switch to recurring billing, ReliaBills can help you start today! Our recurring billing software automates recurring invoices and payments, which is a huge time saver. In addition to that, the ReliaBills recurring billing software also helps improve your cash flow and makes it more predictable. Furthermore, our system will remove the need for manual checks or paper-based processes in your payment process. That way, you can fully grasp the ease and convenience of automated billing.

Recurring Billing Software from ReliaBills

ReliaBills offers recurring billing software to help manage your recurring billing processes. Using our recurring billing feature, you can set up recurring invoices and recurring payments in minutes! In addition, you can also automate payment collection with recurring or single-use tokens that are tied directly to the user’s account.

If you’re ready to get started today, you can create your free account now to access the ReliaBills basic plan. However, if you want to go premium, you can upgrade to ReliaBills PLUS for $24.95 per month. Visit our pricing page to know what additional features you will get from the PLUS version.

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

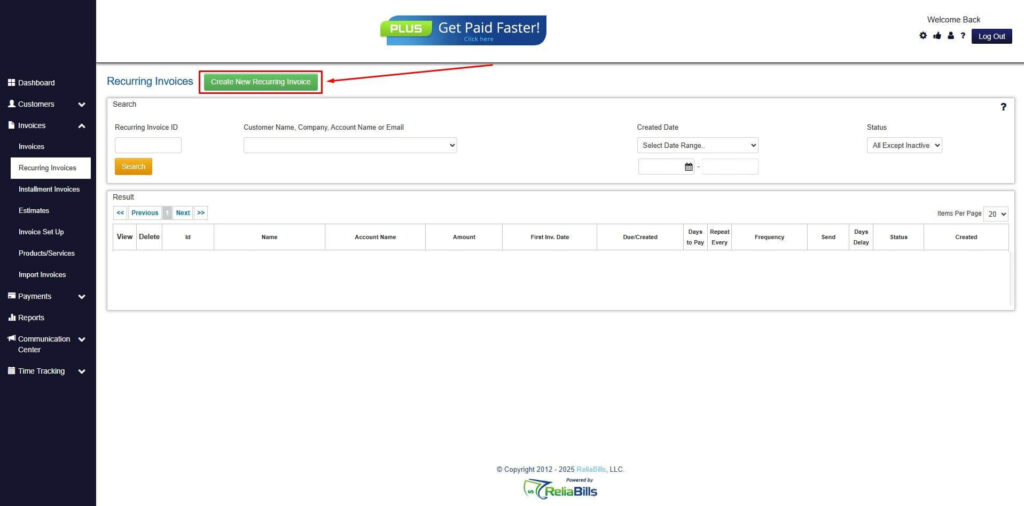

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

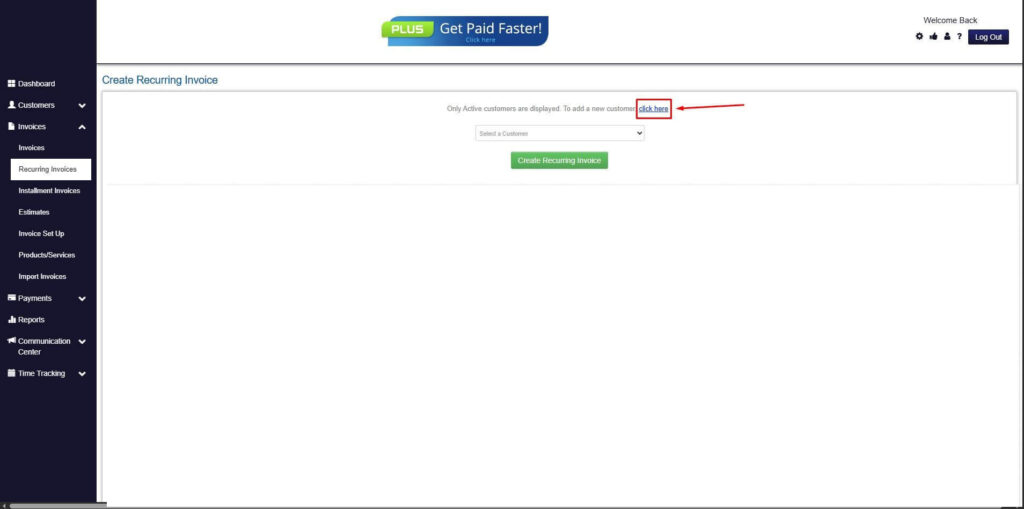

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

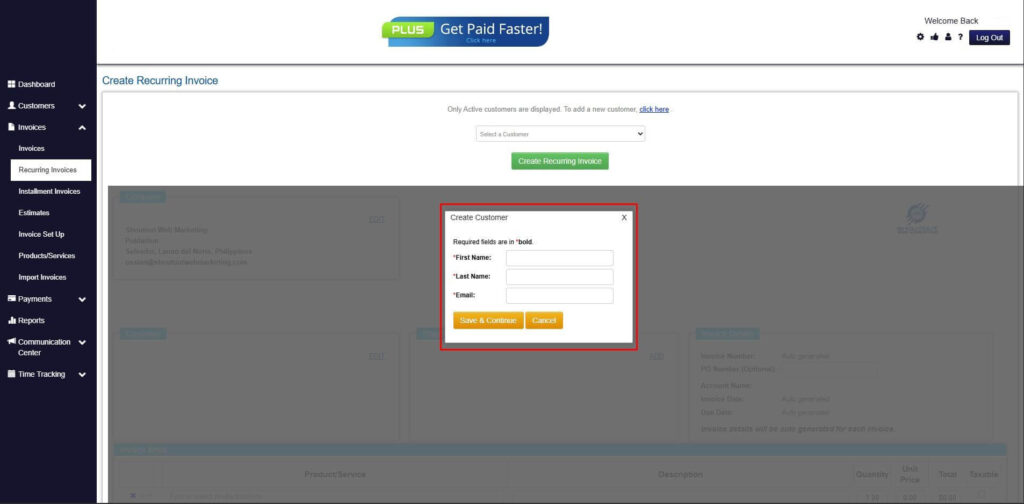

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

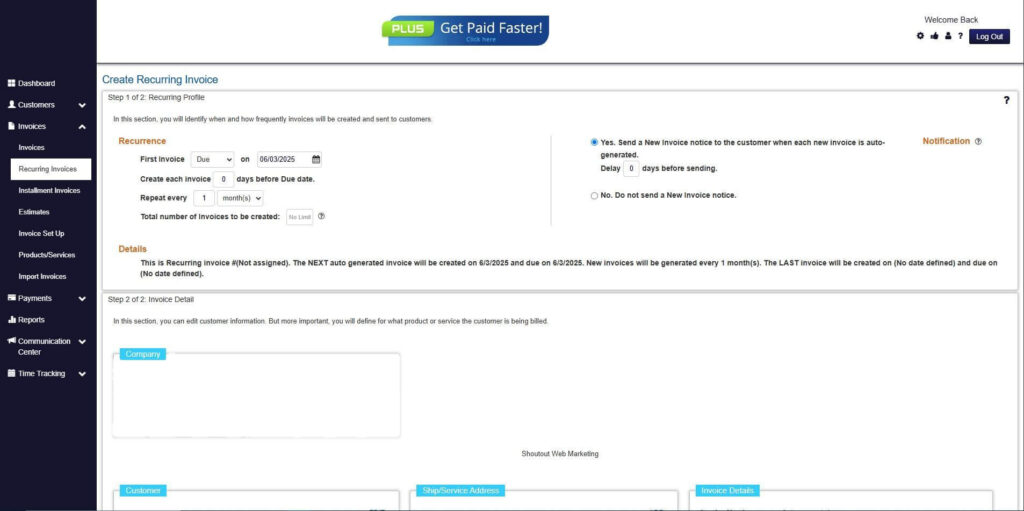

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

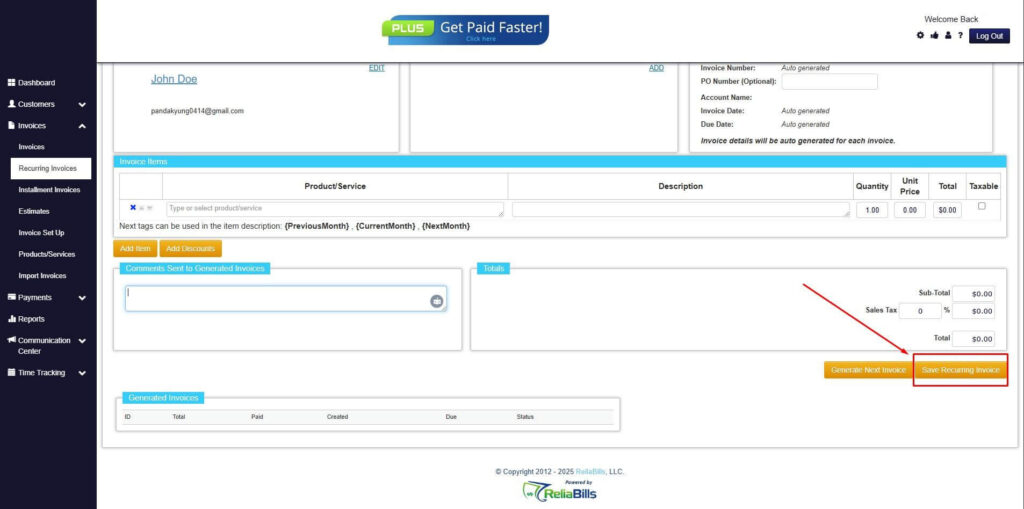

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

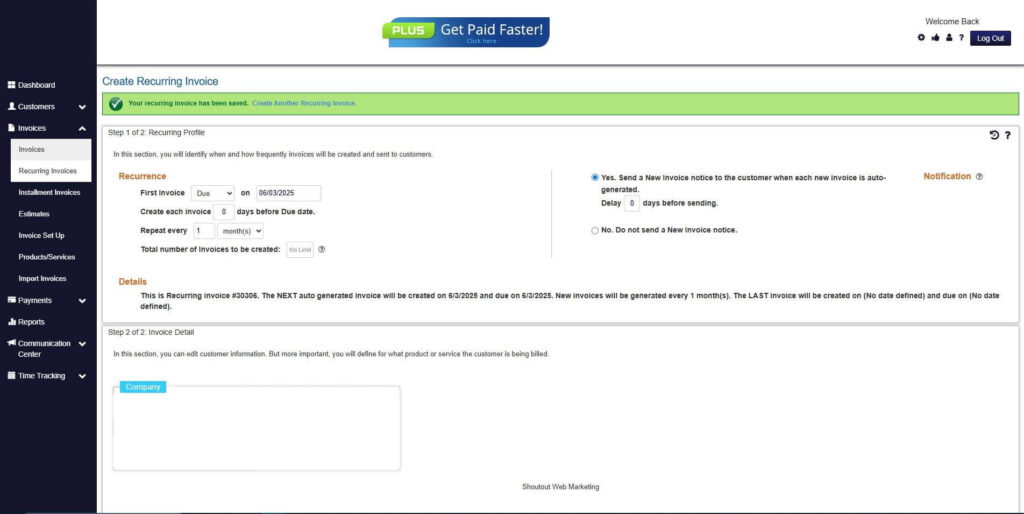

Step 9: Recurring Invoice Created

Your Recurring Invoice has been created.

Wrapping Up

When it comes to writing an income statement, it’s always important to know the details that come with it. From income figures to accounting to total operating expenses, these terms will be important for businesses that need to calculate their income statement. All of the information in this article will prove useful once your company grows, and you’ll need to create an income statement.