While rates vary by industry to some extent; in general, you can expect 10% of your customer’s credit card payments to get declined. In a card-present or retail setting, credit card declines can be unsettling. As the merchant, you don’t want to be the bearer of bad news, especially when your customer is standing right in front of you. Certainly, the recipient doesn’t like it either. So how can you fix this matter without it getting awkward for both you and your client? Well, for one, you have ReliaBills.

Fortunately for ReliaBills and our valued clients, most invoicing takes place in a card-not-present transaction. A card decline can cost you a payment that can result in frustration. That’s where ReliaBills comes in and saves the day. But before we get into too much detail, let’s first understand what a card decline is, and why does it happen.

Dealing with Credit Card Declines

Credit card declines can be a challenge for both you and your client. The decline message sent by the card-issuing bank is often intentionally vague or doesn’t make any sense. There are two good reasons for this:

- Banks need to protect their customers’ privacy. Quite frankly, as the merchant, it’s none of your business that the cardholder is behind on paying their bill, maxed out on their credit card, or had their card temporarily lost.

- If the transactions were made by fraudsters, providing more detail could potentially give them clues on how to find a way around security.

2 Types of Credit Card Declines

Credit card declines are defined by two categories: soft declines and hard declines.

Soft Declines

A soft decline occurs when the issuing bank successfully identifies the card and cardholder information; however, for any of several reasons, it fails to approve the disbursement of funds. Common reasons for a soft decline to take place are as follows:

- Insufficient Funds. As the name suggests, there are not enough funds for the transaction to take place.

- Card Activity Limit Exceeded. Often, for the protection of the cardholder, banks will limit the number of daily transactions, which is the maximum of a single transaction of the daily aggregate amount of transactions.

- Do Not Honor. The issuing bank has identified the card and cardholder but is refusing to disburse funds. For the protection of the holder, the bank is withholding useful information. The reason for the decline comes from one or multiple information provided (name, zip code, expiration date) to be incorrect.

- Generic Decline. Similar to “Do Not Honor,” the issuing bank has identified the card and cardholder. However, it’s refusing to disburse funds. Again, for the protection of the cardholder, the bank withholds useful information.

The only good thing about soft declines is that transaction failures are temporary. You can retry your card in one or two days after the decline occurs and hope for valid authorization. Typically, the card association will allow four attempts in 16 days.

Hard Declines

A hard decline occurs once the issuing bank does not approve the payment. This type of card decline is a permanent authorization failure that doesn’t have any retries. Hard declines may be caused by:

- Expired card. The card has or is about to reach its expiry date. In most cases, banks will issue an entirely new card number as opposed to simply extending the expiration date.

- Stolen Card. The card’s owner has reported it as stolen, and the bank is preventing any future transactions from going through. If the payment seems to be recurring, decline service to the person who is attempting the transaction and request an updated payment method from them.

- Closed Account. The cardholder’s bank does recognize the account. However, the account has been closed. The reason for the closure is undefined.

- Transaction Not Permitted. The customer’s bank is declining the transaction for unspecified reasons. In most cases, it’s possibly due to an issue with the card itself. A hard decline occurs when the problem originates with the processor or the issuing bank.

The problem with hard declines is that no matter how many times you retry your card number, it won’t work. The only way to prevent losing the payment is to have the customer fix the problem. It will eventually result in them having to give you a new credit card to avoid a delay.

How ReliaBills Can Get You Paid

The ReliaBills Merchant Services offers Revenue Recovery Tactic as an integrated feature of the software. That means we can get direct access to your customers and their payments. We can create standard and recurring invoices to make sure you get paid no matter the circumstances.

Here are samples of the difference that ReliaBills can do during a card decline:

- Customer payment information can be securely stored within the platform. That means we are aware if a card on file is about to expire and can notify you in advance.

- Even though you may have a card stored within ReliaBills for auto-pay, we can still send an automated reminder that auto payment will be made in a few days.

- If an auto-payment fails due to a soft decline, you will be notified immediately. Since it’s a soft decline, ReliaBills will automatically retry the card every two days for a total of four attempts.

- If an auto-payment fails due to a hard decline, you will be notified immediately. But since it’s a hard decline, ReliaBills cannot make another attempt. Instead, you will be automatically un-enrolled from auto pay and will receive the scheduled payment reminders.

With ReliaBills, you get a brandable payment portal. That way, your customers can self-manage their information. All of this makes ReliaBills a reliable option for small business owners to pay and get paid fast.

Our Recurring Billing Feature

Another excellent way ReliaBills can get you paid is through its recurring billing feature. It’s a payment model that enables you to bill your clients on a predefined basis. ReliaBills automates your entire payment process, which automatically charges your customer and sends them an invoice for goods or services on a prearranged schedule. In turn, you won’t have to worry about invoicing since everything is automated. This level of convenience will enable you to focus more on your business while you get paid in the process.

When a credit card decline happens, chances are your customers aren’t aware of it. With ReliaBills, you and your customer will receive a notification about the latter’s credit card getting declined. That way, they can either look to resolve the issue or use a different card to settle the payment. ReliaBills automates everything so that you won’t have to do it yourself manually. All you need to do is wait for the payment to enter your bank account.

Is recurring billing ideal for your business? Many indications say it will. For instance, if you’re running a subscription-based business, you will definitely thrive from a recurring billing strategy. So, if you’re collecting the same payment from your clients on a particular period, then you can benefit significantly from automating your payment processing through recurring billing.

With a solid recurring billing software like ReliaBills, you can reap the benefits that this billing model brings to the table, namely the following:

Save Time and Money

One of the main advantages of using a recurring billing system is the convenience of automating and streamlining the entire billing process. ReliaBills keeps track of your subscriptions, payment information, and payment due dates. By doing so, it can prepare and send invoices to clients regularly.

ReliaBills can also send email notifications about the status of your invoice. That way, you can monitor the progress of each invoice you send. With automation and standardization, you can eliminate the need for manual invoicing. In turn, it will reduce the time, effort, and cost associated with fulfilling this task.

Reduce/Eliminate Late Payments

A traditional payment system can be prone to late or nonpayment. Fortunately, you can remedy that by automating your invoicing system with ReliaBills. This feature is especially important when your customer base starts to grow. ReliaBills makes it easier to flag non-paying customers by sending them a past due notice. You can also pinpoint which customers tend to make these late payments. That way, you can focus more on them.

Establish Better Customer Relationship

Recurring billing is beneficial to both the business and its customers. Automation provides a level of convenience that every customer will appreciate. ReliaBills provides a tracking capability that will help you keep tabs on all the invoices that you send. In turn, your customers will also appreciate getting notified and settling their accounts in a single, convenient payment processing gateway. As a result, you can build better relationships with your customers. In turn, you can also increase customer retention rates while reducing potential churn.

There is a lot more to discover about ReliaBills and its awesome recurring billing process. So if you’re interested, make sure you head here to know more about this amazing feature.

We do more than anyone to get you paid. Visit us at www.reliabills.com. For more information, you can send us your inquiries at sales@reliabills.com. Or call our hotline at 1-877-932-4557.

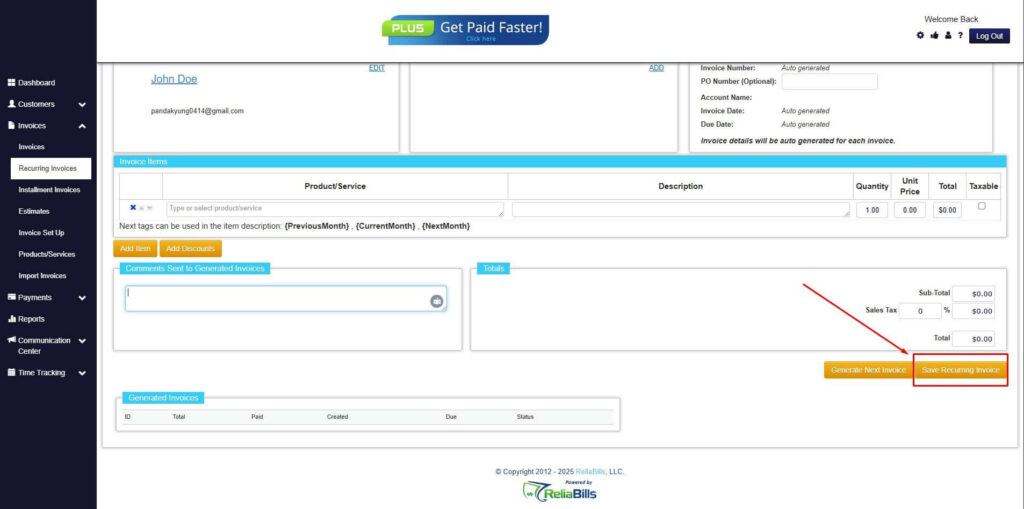

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

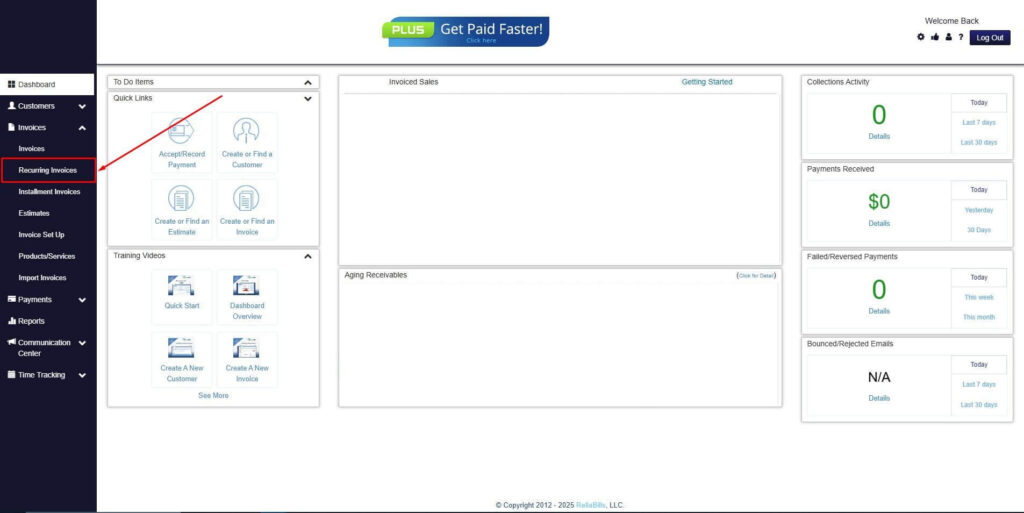

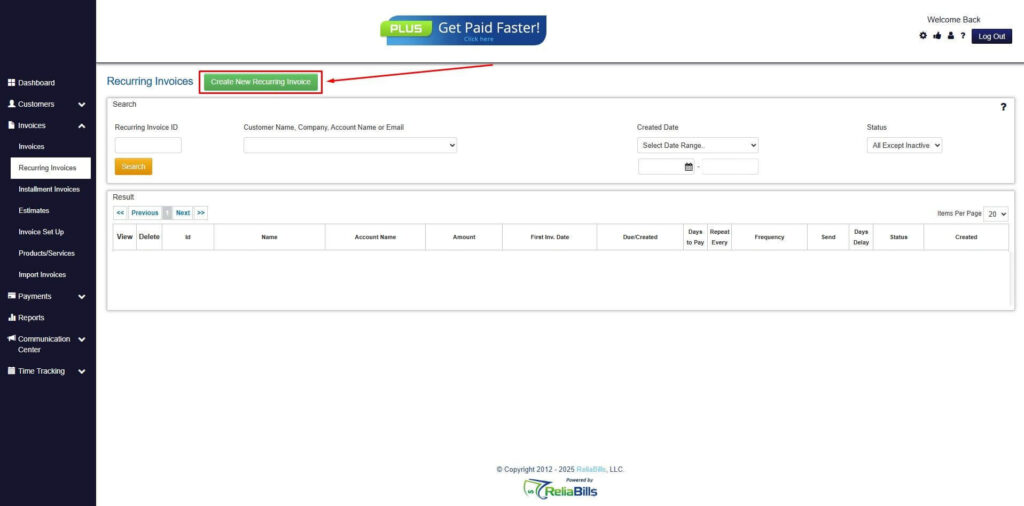

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

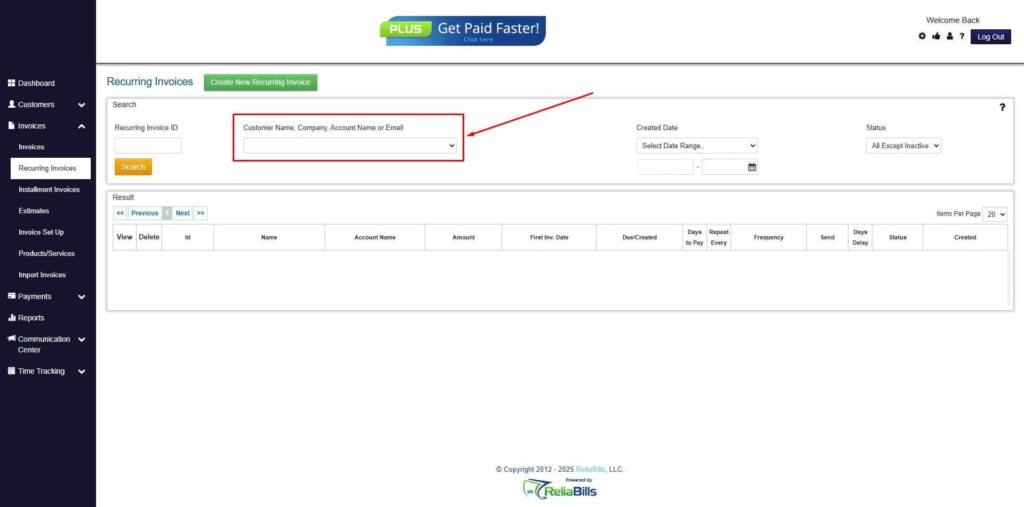

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

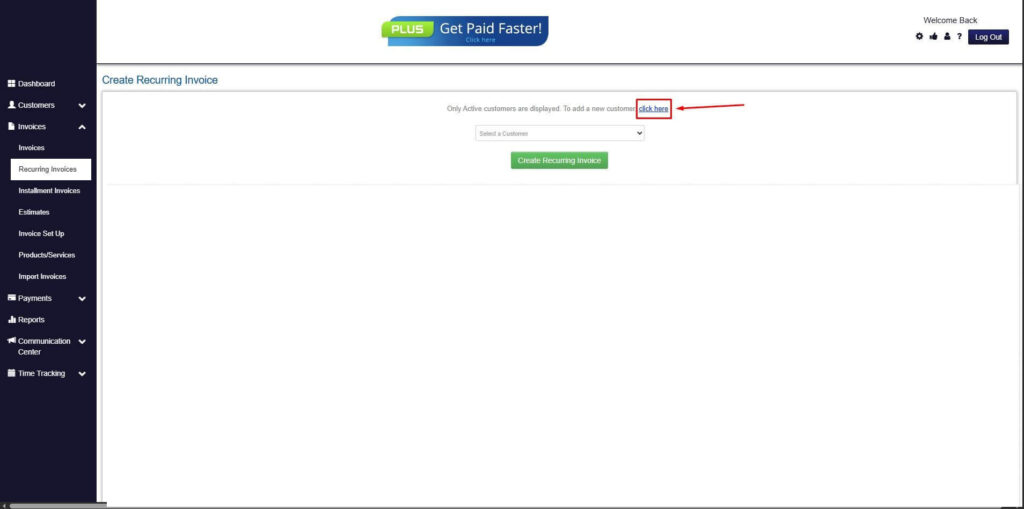

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

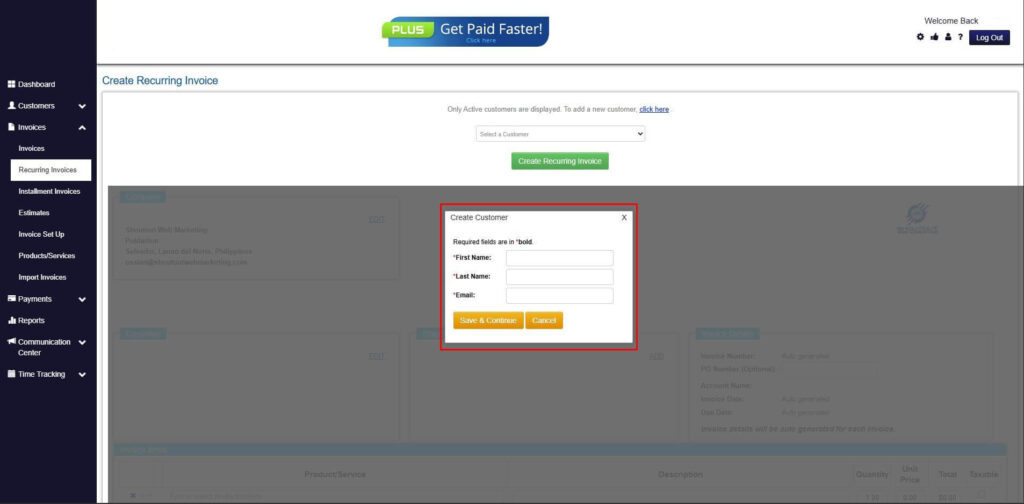

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

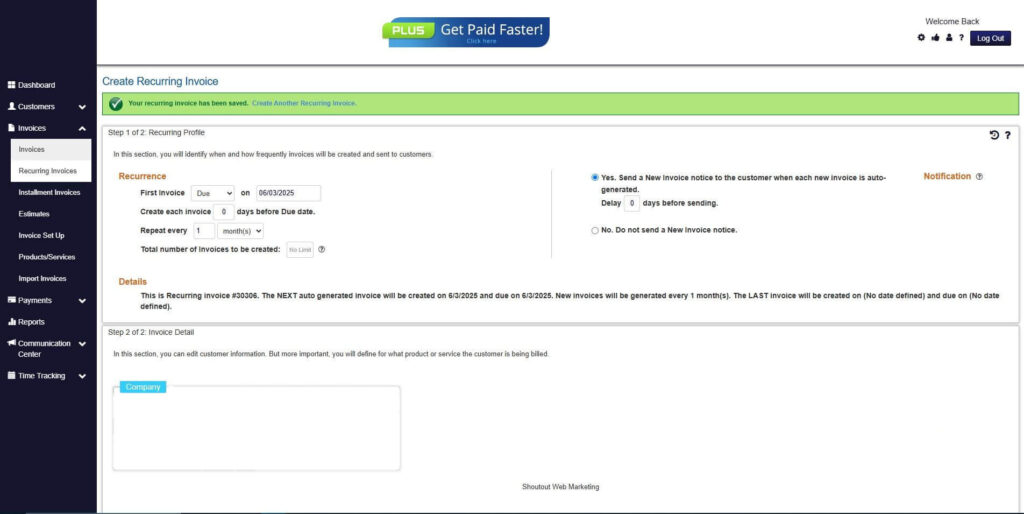

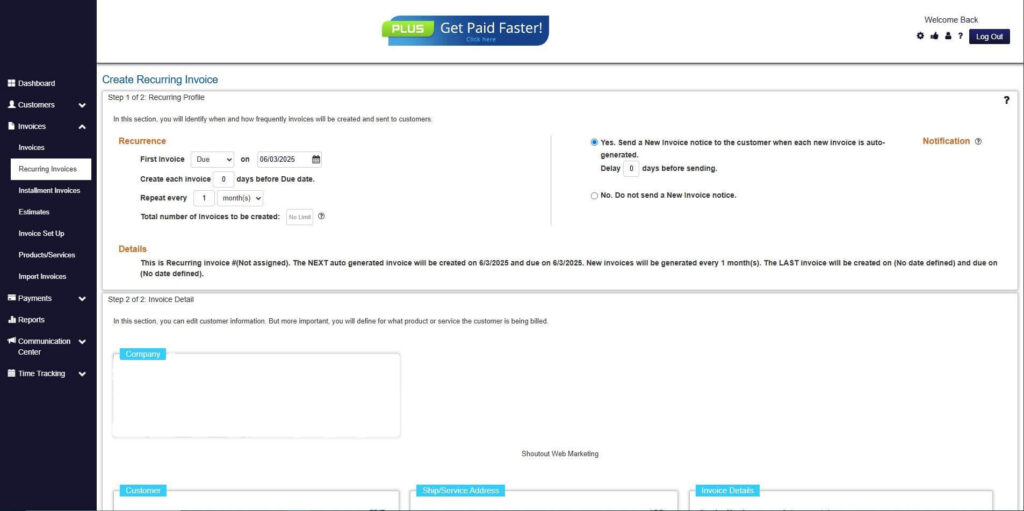

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

Your Recurring Invoice has been created.