Every year, the trend for bank invoice and ACH payment continue to increase at a rapid pace. In fact, a 2016 study found out that non-cash amounts increased by 10% that year, reaching a staggering $482 billion. The study also projects that growth from 2016 to 2021 indicates that non-cash transactions will continue to grow to another 12%.

There are several electronic payment options available, from credit cards to e-wallets like PayPal. But there are two types of electronic or online payments that have been around for quite some time now and are still relevant today. These are wire transfers and ACH (or Automated Clearing House) payments. For this article, we’re going to take a look at ACH payments and how to create a bank invoice template.

What is ACH Payment?

An ACH payment happens when money from one bank or financial firm is moved to another. This type of payment moves through a national network, all while a ‘clearinghouse’ processes the transaction.

Once a transaction passes through the clearinghouse, the network then batches daily online payments, which allows the network (not a bank) to process them later in the day. This process makes sure that each recipient receives the proper amount. Once processing is complete, the receiving bank will then receive their ACH payment in a batch. They will need to attribute each deposit to the appropriate bank account. Credit card payments can also make good use of ACH invoices. This payment method will prove useful for several applications.

This entire process is automatic, which means there won’t be any manual processing. By opting for electronic payments instead of manual paperwork, recipients will receive their money, in a fast, safe, and less expensive manner.

What is a Bank (ACH) Invoice Template?

A bank (ACH) invoice template is a form of invoicing that’s used to formally request one-time or recurring payments from a client through means of their bank or financing institution. ACH bank payments facilitate bank-to-bank transactions, allowing customers to make payment without having to use their credit cards, checks, or on-hand money. Bank transfers (also known as e-checks) benefits service or product-based business in many different ways in comparison to more standard invoice payment methods.

Advantage of a bank (ACH) invoice include the following:

- Quicker payment processing

- Lesser payment turnaround

- High-level security

- Cheaper transaction costs

- Convenience for both parties

In addition to the perks mentioned above, bank transfers are a great option because of the more definite nature of online payments. Unlike credit cards, ACH payments are very difficult and complicated to reverse. This payment method will be used for different applications, so make sure get familiar with it. For an ACH deposit to be reversed and disputed, the transaction would have to fall on the following situations:

- Unauthorized

- Initiated on the wrong date

- Be an incorrect amount

Required Information for ACH Deposit

To complete a bank (ACH) transfer, the issuing company will need to collect the following details and information from the customer:

- Bank account type (savings/credit)

- ABA routing number (nine-digit code for identifying the bank)

- Customer’s bank account number

- Full bank/credit union name

Since bank information is sensitive, companies need to make sure all invoice documents are in a safe and secure location for present and future accounting work.

Length of ACH Deposit Process

You might be wondering, ‘how long does an ACH deposit take?’ It will depend on the financial institution and the time in which the transfer was initiated. Transfers can take anywhere from one to five days. On the other hand, the more standard time frame consists of three to five days.

Differences Between a Bank Wire and ACH transfers

With both wire transfers and ACH transfers being electronic, transferring money from one location to another is now easier than ever. However, it can potentially confuse the invoice payment methods with each other. While many minute differences separate the payment types, the following are the major separating features, according to NorthAmericanBanCard:

- Security: both transfers go to a safe and secure payment gateway. However, wires are usually preferred by the recipient due to them being impossible to retract. On the other hand, bank transfers can be reversed in certain situations.

- Cost: the average cost of a bank (ACH) transfer is between $1 and $3. In comparison, wire transfers cost between $10 to $45, depending on the transferring institution, and whether the transfer is domestic or international.

- Transfer speed: Wire transfers are almost always done on the same day – unless it’s made after 5 P.M. local time. On the other hand, ACH deposits can potentially take up to five days to reflect in the recipient’s account.

How to Create a Bank (ACH) Invoice Template

To recap, a bank (ACH) invoice is used to collect a recurring payment – or any payment where the creditor has pre-authorization. This process is common for subscription charges or any payment that will be made periodically or repeatedly. No matter the agreement signed, the payor may terminate authorization to the payee at any given moment.

Creating a bank (ACH) invoice is similar to creating a standard invoice. The only difference is the details and some minor inclusions that you need to make. Here’s a step-by-step guide on how to create this type of invoice:

Step 1 – Download the Bank ACH Invoice as a Word or PDF File

There are many invoicing platforms like FreshBooks that offer a free bank (ACH) invoice. All you need to do is download the template in either Word or PDF format. Of course, there are other invoicing systems like ReliaBills that let you edit and create your invoice straight from their platform. In this case, all you need to do is select the bank details invoice template and start editing from the site.

Step 2 – Introduce the Manufacturer or Vendor Expecting Payment

The payment seeker (that’s you) may be a Manufacturer, Vendor, Sole Proprietor, or Contractor. In any case, the full identity of the payment seeker should be added to the “Company Name” box or field introducing the header.

Beneath the “Company Name” should be a distinct set of empty lines displayed with labels. The first line is reserved to identify the one in charge of the business that’s seeking a payment.

This person or company’s identity should be followed with entries defining your complete business address. Include your street address, city, state, country, and zip code.

Display the payment seeker’s telephone and email information on the blank lines that says “Phone” and “E-mail” to complete the header.

Step 3 – Make a Presentation of This Document’s Classification

Even if the paperwork we are creating is, in fact, an invoice, it won’t be regarded as such without adding an item that will classify it as a written payment request. That’s why you should add an Invoice number. The template usually has a blank line that says “Invoice No.” near the top of the page under the header. If not, then you can add a dedicated section for this one. The invoice number will also be useful for recording and documentation purposes.

Don’t forget to include specific dates like the date of when this invoice is created and the payment due date. Make sure you add the dates in the “Date” line.

Step 4 – Submit the Client ID

This invoice will continue with an additional section of identification before proceeding to its focus. The “Bill To” section will act to inform the Recipient of this document’s expectation of them and will call attention to itself with a heading. The first line will need the Payer or Client’s “Name” furnished. Supply this “Name” field then proceed to place the paying client’s complete billing by making the next three available lines.

Step 5 – Document the Product, Subscription or Service Being Bought

Now that everything is in place, it’s now time to deal with the subject of this invoice. That’s why the next thing you need to do is to attend a basic table that will organize its presentation. The “Description” part of the invoice should feature summaries defining items such as dates or work, product/merchandise descriptions, or any other definition that can easily be confirmed by the customer.

After defining what the payment transfer will cover, we must also define the payment on its own. Locate the second column on this table and record the exact base cost underneath the “Amount” section.

Step 6 – Itemize the Products or Services

More than one amount should be listed above. Many invoices tend to allow this with a “Subtotal.” In this section, you must add all such amounts owed to one sum then report this result in this field.

Don’t forget to calculate taxes like sales or service taxes, as well as any other relevant additions to the cost. Make sure you add them to your subtotal.

Step 7 – Inform the Client About the Final Day Payment

The wire transfer or direct deposit should be expected by a certain day. This process can be expressed as a countdown from the invoice “Date” that you provided. Enter the maximum number of “Days” from the invoice “Date.” It should define when this document’s response is a payment.

Step 8 – Provide the Banking Information Needed for Fund Transfer

In most cases, the Paying Client will be unable to affect a wire or bank transfer or a direct deposit without the necessary information. The banking information has been set to display at the end of this invoice but will require your entries to be completed.

Make sure you locate the “Make Payment To” section, then add the account number and routing number where payment must be deposited on the appropriate lines at the top of the left- and right-hand column respectively. Also, don’t forget to add the name of the bank and that of the merchant account holder.

Last but not the least, the address where the Bank where the Client will deposit the payment must be presented. The “Address” line at the end of this section will accommodate this need nicely.

Why Automate your Bank (ACH) Invoice?

Knowing how to create an invoice is great. But if you want to make it even better, you should tap into recurring billing. It’s currently the hottest trend in the payment processing industry. And it’s not hard to understand why: recurring billing can help you manage your cash flow better and make more money per month without having to do too much invoicing.

How Does Recurring Billing Work

Recurring billing is a great way to ensure that you always have cash flow coming in, especially if your product or service is subscription-based. It allows customers to pay for products or services regularly, usually monthly. This can be helpful for both you and your customers.

For customers, it means they don’t have to worry about remembering to pay each month. They make one payment, and you get paid every month until they cancel their subscription.

For you as a business owner, it means that you can collect money even when your customer forgets to pay or doesn’t have the cash on hand at the moment of purchase – which happens more often than people think!

How Recurring Billing Can Help You

There are a few critical ways that recurring billing can help you as a business owner:

- It can help you manage your cash flow better. When customers pay on a monthly basis, it spreads out your payments and enables you to avoid having large sums of money coming in at once. This is helpful whether your business is just starting or you’re already running a large enterprise.

- It can help your customers pay at the right time. Nowadays, people tend to not have cash on hand when they make purchases online – and while that’s fine in some cases, recurring billing makes it easier for them to get paid!

- It creates more stability in your business. Recurring billing is a great way to ensure that you always have more cash coming in than going out – which means there’s less chance for your business to go under.

- It can help you increase revenue and make more money. By making it easy for customers to pay multiple times each month, recurring billing helps them invest in your products or services more quickly, which means you can earn more money per month.

- It makes it easier for your customers to pay and stay on top of things. Rather than remembering when they need to make a payment or worrying about paying late, recurring billing helps ensure that customers don’t have as much stress in their lives!

ReliaBills Recurring Billing

When it comes to recurring billing, you have many options in the form of software and apps. Some are better than others, but we strongly recommend using ReliaBills for your invoicing needs if you want an easy way out. The basic plan – which includes all the invoicing features – is 100% free. But if you want more features like recurring billing, you need to upgrade to ReliaBills PLUS for only $24.95 per month.

With ReliaBills, you can create an invoice template that will automatically bill your customers on a recurring basis. You set the parameters, and ReliaBills will do the rest! This is a great way to make sure that you always get paid on time without any hassle. Plus, it’s super easy to use, so there’s no steep learning curve.

If you’re looking for a great way to automate your invoicing process, we highly recommend using ReliaBills. It’s easy to use and will save you time and hassle in the long run. Plus, it’s affordable, so there’s no reason not to try it out!

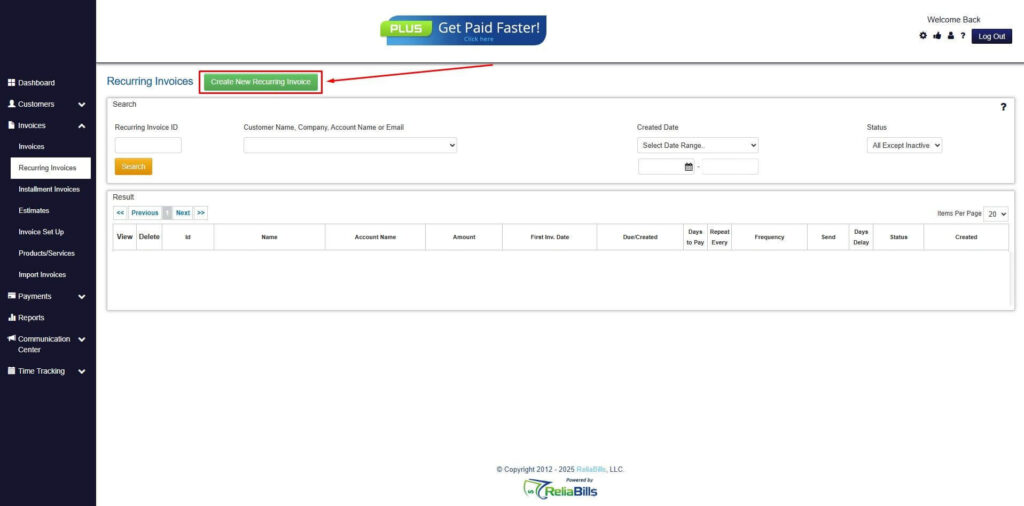

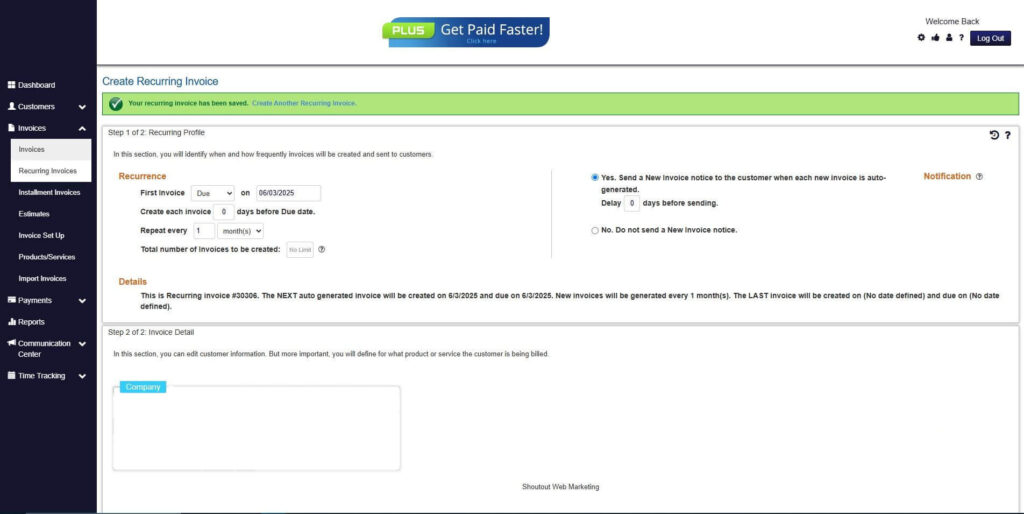

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

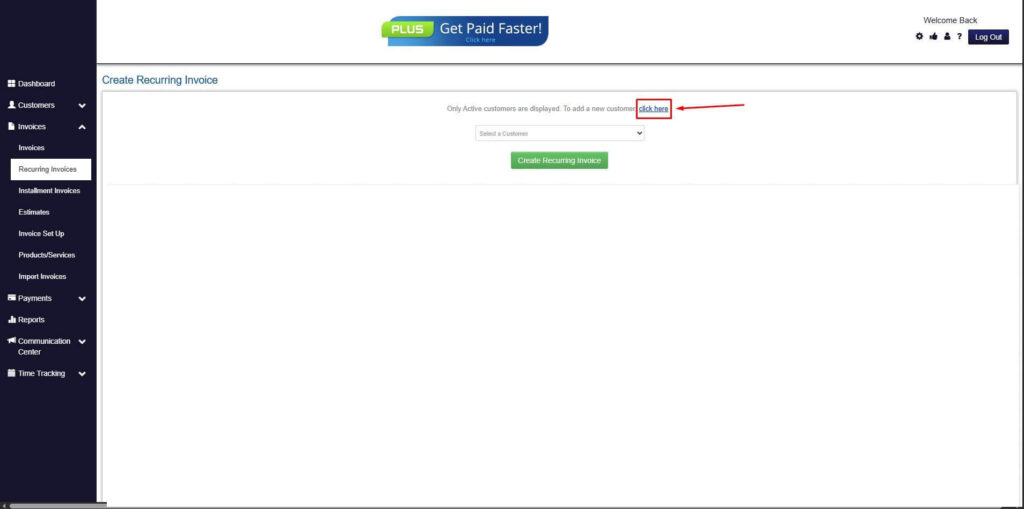

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

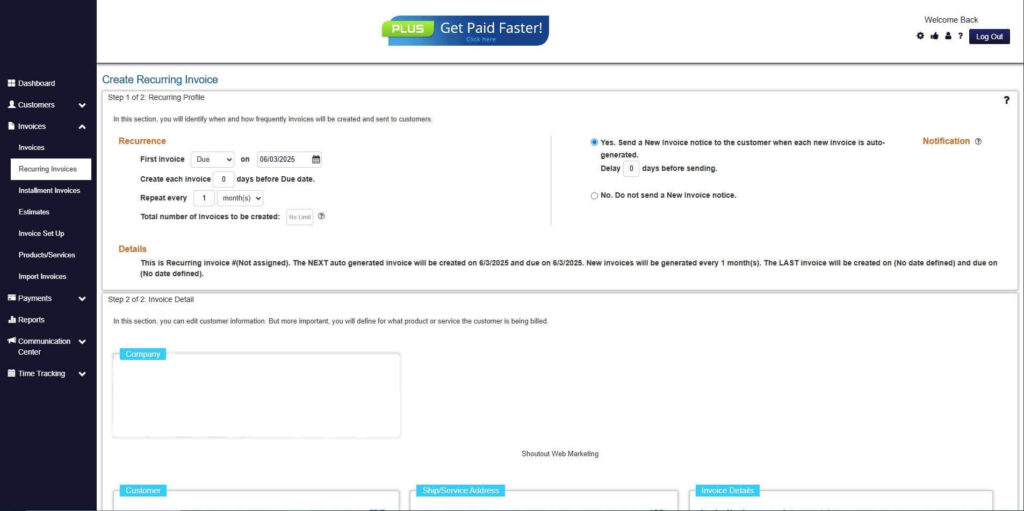

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

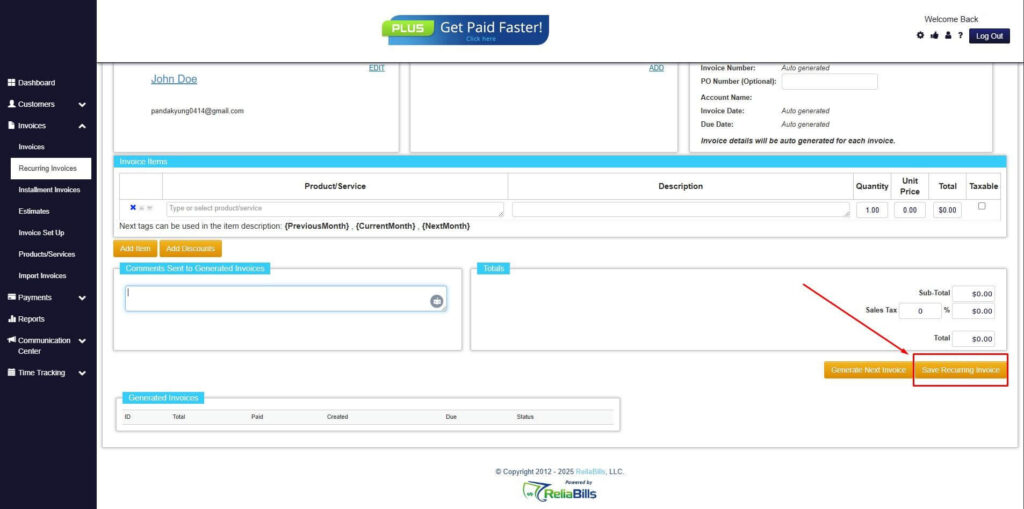

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

- Your Recurring Invoice has been created.

Wrapping Up

With this type of invoice, you will be paid faster. Now that you know how to create a bank (ACH) invoice, you can now do so to get payment from your clients. Just make sure to follow this guide carefully so that you can create the proper ACH invoice for both present and future transactions. This payment method proves useful for different aspects. Keep in mind that you can also use ACH invoices for credit card payments.