Understanding the intricacies of credit card processing, particularly the mechanisms of Authorize and Capture, is crucial for merchants aiming to optimize their business operations. These two processes form the backbone of payment card transactions and profoundly influence a merchant’s cash flow and customer satisfaction.

This article will explore the nuances of ‘authorize and capture,’ unraveling their functionalities and demonstrating how merchants can leverage them for greater transaction efficiency and security. By breaking down these concepts into their building blocks, merchants can gain the necessary insight to make informed decisions about managing and executing payments.

Definition of Authorize and Capture

The first step in uncovering the mystery of authorize and capture is understanding their respective definitions and purposes. Let’s break down each term to discover what they represent in the payment card industry.

Authorize

Authorize is the initial step in the credit card processing cycle. It validates the buyer’s credit card details and checks whether they have sufficient funds for the transaction. During this phase, the issuing bank holds the demanded amount on the cardholder’s account, but no money is transferred yet. This process helps to mitigate the risk of fraudulent transactions and insufficient funds.

Capture

The Capture process follows Authorize and refers to collecting the previously held funds from the customer’s bank account. This process can occur immediately after authorization for businesses providing instant services (like grocery stores) or later for those who need time to prepare. Please try again or contact support if it continues.

Essential Steps in the Authorize and Capture Process

Both processes are essential to the payment card industry, enabling merchants to process transactions securely and reliably. Here’s a closer look at both phases in greater detail:

Step 1: Create the Payment

The process starts with the creation of a payment. Here, the customer presents their credit card for payment by swiping, inserting, or providing the card details online. The merchant’s payment gateway then prepares to process the transaction. This step also includes the entry of additional transaction information such as amount, date, and time.

Step 2: Request for Authorization

Post the creation of payment, the merchant submits an authorization request. The payment gateway sends the transaction details to the issuing bank in this step. The bank then reviews the transaction, ensuring the validity of the card details and checking if the cardholder has sufficient funds to cover the transaction. If approved, the bank earmarks the transaction amount, securing it for future capture.

Step 3: Capture Funds

The final step in the process is capturing the funds. At this stage, the merchant sends a capture request to the issuing bank to transfer the previously authorized funds. If the authorization is still valid, the bank will transfer the funds from the customer’s account to the merchant’s account, finalizing the transaction. Merchants must know that delayed captures may lead to declined transactions, as authorizations can expire.

Examples of Authorize and Capture in Action

Let’s explore a couple of examples to understand how Authorize and Capture work in real-world situations.

Example 1: Immediate Capture at a Grocery Store

Suppose a shopper at a grocery store presents a credit card for payment at checkout. The cashier swipes the card, and the payment gateway requests authorization from the cardholder’s bank.

Once authorized, the bank earmarks the purchase amount from the cardholder’s account. The grocery store, providing immediate services, captures the funds right away. The transaction is completed within seconds, and the shopper can leave with their groceries.

Example 2: Delayed Capture at an E-commerce Store

Online businesses often process transactions differently. When a customer orders, the payment gateway requests authorization from the cardholder’s bank. If approved, the earmarked amount is held for future capture.

However, instead of capturing the funds immediately, the merchant waits until they are ready to ship the product. Once the product is dispatched, the e-commerce store captures the funds, completing the transaction.

Example 3: Partial Capture in a Restaurant

In the restaurant industry, the payment process includes an additional layer of complexity due to tips. When a customer pays their bill, the restaurant requests authorization for the amount of the meal alone. Once authorized, this amount is held for future capture.

The customer then adds a tip to the bill, and when the server closes out their shift, the restaurant sends a capture request for the total amount, including the meal and tip. This way, the restaurant effectively uses a form of partial capture, initially authorizing one amount but capturing a greater amount that includes the additional information.

These examples illustrate that the timing of the capture can vary based on the nature of the business and the services provided. Understanding and effectively managing the Authorize and Capture process can significantly enhance the fluidity of transactions and customer satisfaction, leading to sustainable business growth.

How to Authorize and Capture Relates to Recurring Billing

Recurring billing is another unique instance where the Authorize and Capture process is crucial. This model applies when the same customer is billed repeatedly over time, usually for subscription-based services such as software, digital media, or fitness memberships.

Authorization in Recurring Billing

Similar to single transactions, recurring billing requires an initial authorization for the first payment cycle. The merchant must validate the customer’s credit card details and ensure the availability of sufficient funds. However, re-authorize might not always be necessary for subsequent billing cycles, depending on the payment gateway and the recurring billing setup.

Capture in Recurring Billing

The capture process in recurring billing happens at predefined intervals based on the subscription plan. This could be monthly, quarterly, or annually. The merchant captures the authorized amount from the customer’s account at each interval.

Challenges & Considerations in Recurring Billing

One challenge in recurring billing is maintaining up-to-date card information. Cards may expire, get lost, or be replaced, leading to failed transactions. Therefore, merchants need to have a system in place for updating card details.

Furthermore, while recurring billing simplifies the transaction process for the merchant and the customer, it also requires the former to stay compliant with the Payment Card Industry Data Security Standard (PCI DSS) due to the storage of customer card details.

Understanding and correctly implementing the Authorize and Capture process is crucial in ensuring the smooth operation of recurring billing, ultimately leading to improved customer retention and steady revenue streams.

Why Use ReliaBills?

If you’re going to accept credit cards in your business, it’s essential to make sure you’re using the right payment gateway. Billing software can streamline and simplify the payment process, helping companies maximize profits while minimizing manual effort. If you’re shopping for the ideal billing system right now, you must try ReliaBills!

ReliaBills is a cloud-based invoicing and billing software designed to automate payment processes, reduce administrative overhead, and streamline payment processing duties. ReliaBills’ payment processing features include automated recurring billing, payment tracking, payment reminders, online payment processing, and much more!

It also provides valuable tools that help manage customer information, monitor payment records, and create proper billing and collection reports. As a result, invoice and billing management are simple and convenient. You also get access to active customer support, ready to assist you whenever you need help.

Get started with ReliaBills for free today! And if you want more features, you can upgrade your account to ReliaBills PLUS for only $24.95 monthly! Subscribing to ReliaBills PLUS will give you access to advanced features such as automatic payment recovery, SMS notifications, custom invoice creation, advanced reporting, and more!

With ReliaBills, you have an all-in-one solution to your invoicing and payment processing needs. Our convenient solutions will enable you to focus more on running and growing your business. Get started today!

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

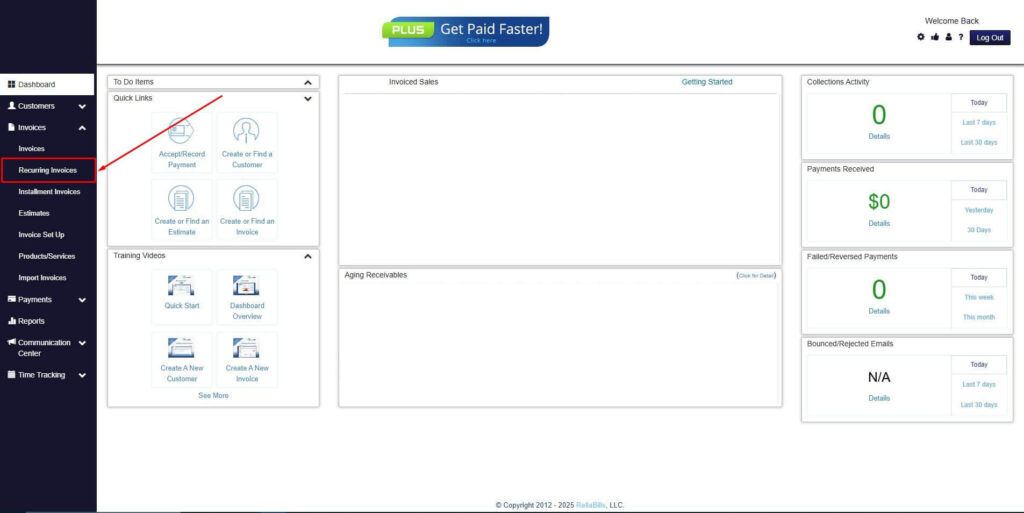

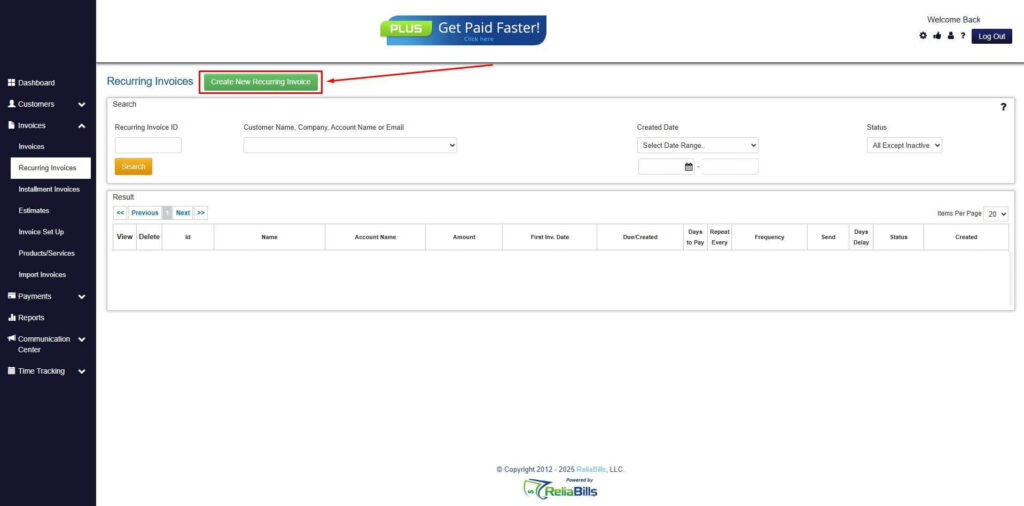

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

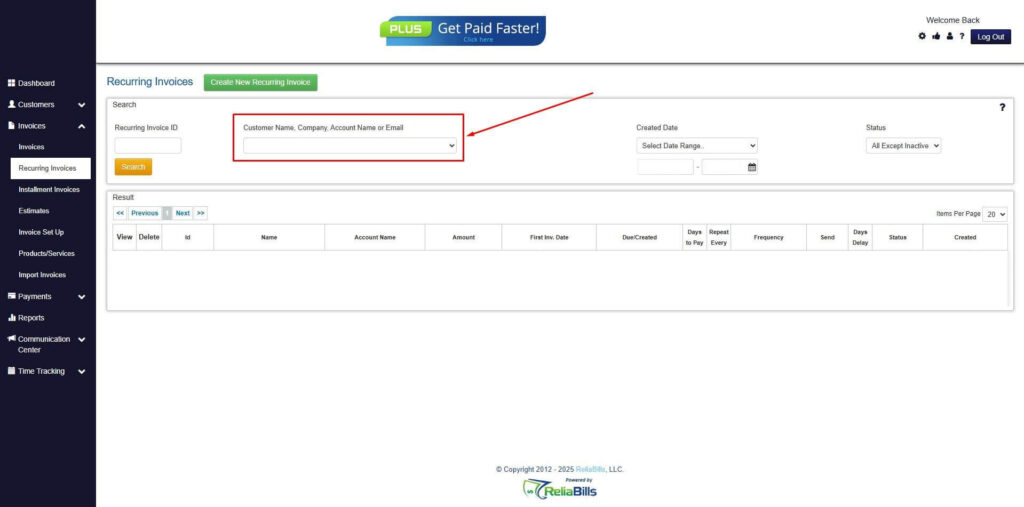

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

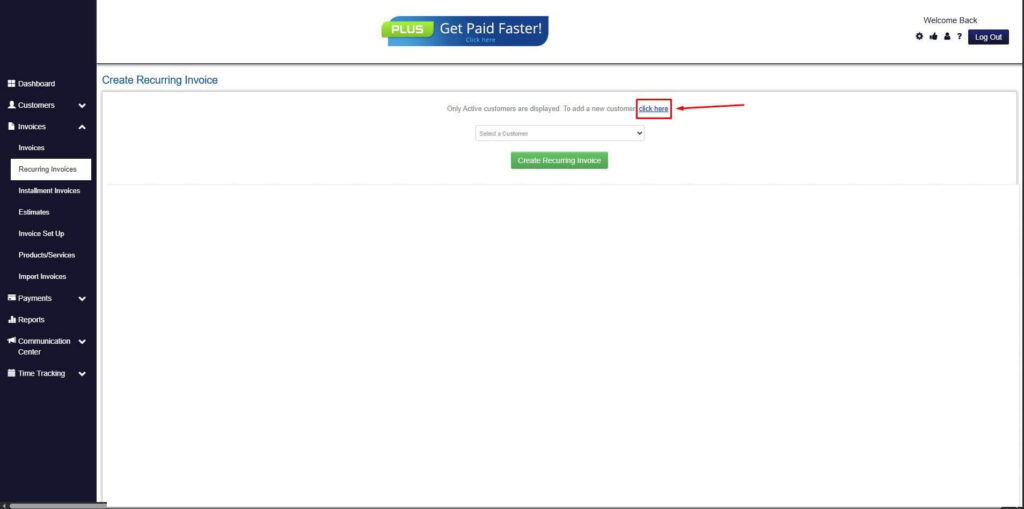

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

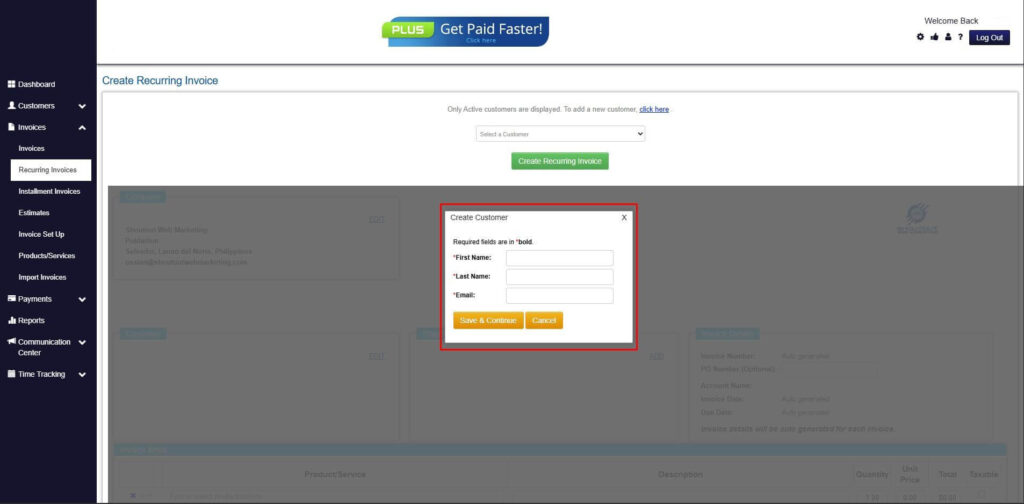

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

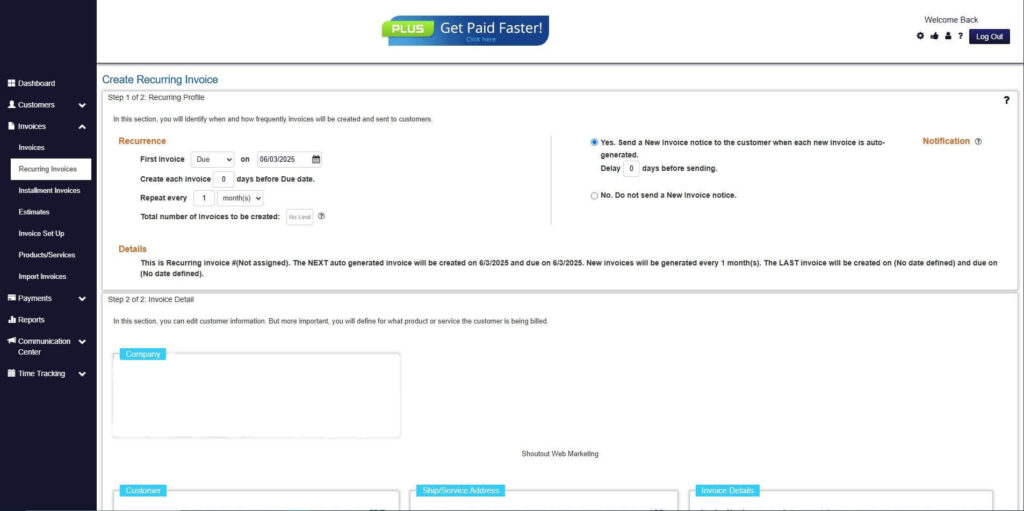

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

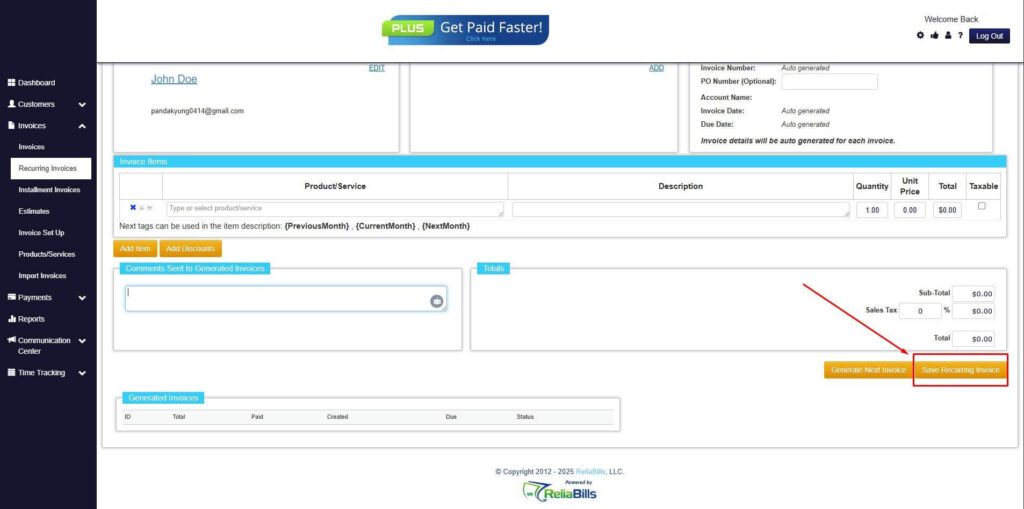

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

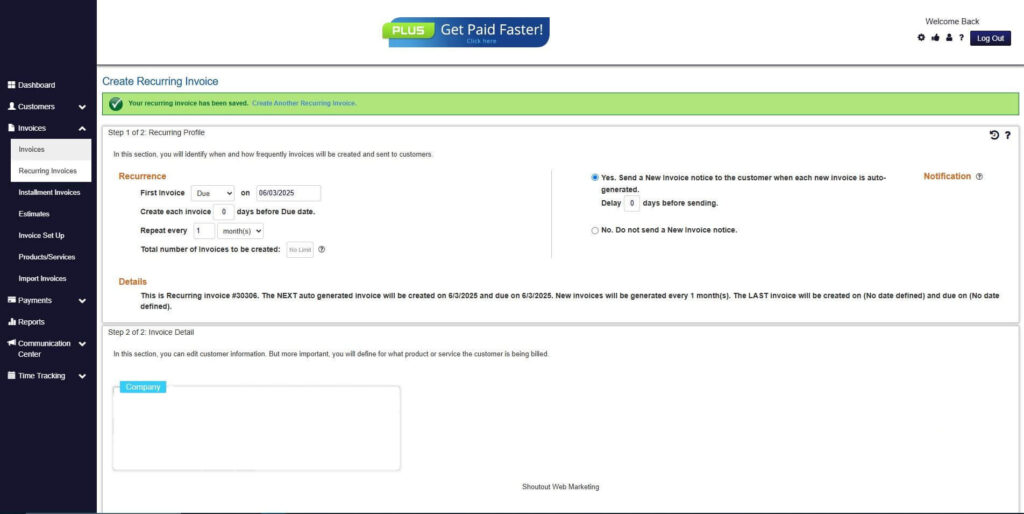

Step 9: Recurring Invoice Created

- Your Recurring Invoice has been created.

Wrapping Up

The processes of Authorize and Capture are critical elements in credit card transaction life cycles, particularly for businesses like e-commerce stores, restaurants, and those offering subscription-based services. Merchants can enhance transaction fluidity, bolster customer satisfaction, and foster sustainable growth by understanding and effectively managing these processes.

Recurring billing adds another layer of complexity, necessitating regular card information updates and adherence to PCI DSS standards. Reliable billing software, such as ReliaBills, can greatly simplify these tasks, automate payment processes, and even provide valuable customer management tools.

Thus, a keen understanding of Authorize and Capture processes and the right tools can be a game-changer for businesses seeking to optimize their payment processing. Get started today!