A lot of business owners love crunching numbers when it comes to profit and revenue. However, only a few have an interest in actual accounting work.

As every business owner can attest, understanding accounting fundamentals can be the difference between a successful business or a complete failure. That’s why as early as right now, you need to educate yourself about financial statements.

At the core, there are three types of financial statements that every small business owner should know: balance sheets, cash flow statements, and profit and loss statements.

On the surface, they may seem like complex and headache-inducing concepts. However, if you break them down into their separate field, you’ll realize that they’re pretty straightforward and easy to understand.

This article focuses on the profit and loss statement, also known as the P&L statement. By the end of this article, you will hopefully absorb everything to know about P&L statements and know where to download a free profit and loss template.

What is a Profit and Loss (P&L) Statement?

A profit and loss statement, also known as a P&L statement, measures your business revenue (sales or income) and expenses during a given period of time. Also referred to as an income statement, P&L is a document that will tell you if your business is either making or losing money.

A small business owner can use a P&L statement to assess his or her business’s overall performance. At the same time, they can also use it to identify points of concern that need improvement and strategies for growth.

In fact, the United States Small Business Administration views the P&L statement as “the best tool for knowing if your business is worth it.” A profit and loss statement is typically assessed in three periods: monthly, quarterly, or annually.

Note that there are different kinds of P&L statements. Some are very simple to understand and create since they are only a few lines. On the other hand, some can also span for a couple of pages. It will depend on the size of your business and how complex your operations are. Basically, the bigger your business gets, the more complicated your profit and loss statement is going to become.

Small businesses with only a few sources of income and expenses will have a shorter and simple profit and loss statement. On the other hand, a larger business with multiple income streams and expenses will have a longer, more complex one.

In terms of form, a profit and loss statement is essentially a table containing all the income and expenses that your business has accrued over a particular period. It is usually created in any spreadsheet tool (Google Sheets, Microsoft Excel, etc.).

The Purpose of a Profit and Loss Statement

The primary purpose of a P&L statement is to calculate and determine the net operating profit and loss of a business. It’s a statement that lets you know if your business is either making or losing you money.

If the P&L statement says you’re making a profit, you should either re-invest in your business, save it, or make a variety of other positive decisions moving forward. However, if you end up with a loss, it’s a clear indicator that your business is unsustainable.

You shouldn’t give up when your P&L statement says that you’re on a negative trajectory. You can use it to pinpoint areas of improvement to salvage your business. However, if you’ve already made the adjustments, yet you’re still losing, it’s probably time to move on to other business ventures.

On top of that, you can also use a profit and loss statement to help you make better, informed decisions like the following:

- Can you afford to hire new employees?

- Can you afford to move into a bigger and better office?

- How are you going to plan your taxes?

- Is your current business growth strategy effective?

Depending on who is using it, a profit and loss statement can have many uses. So make sure you make the most of this document by going through the numbers and see where you’re winning or losing.

How to Prepare a Profit and Loss Statement?

At this point, you now have a general idea of what a profit and loss statement is all about. It’s now time to know how to create one for your business.

But where do you start? Your main focus should be on two accounts: income and expense. To give you an idea, here’s an example of the types of income and expenditures that a typical business has:

Income:

Sales

Revenue

Interest income

Rental income

Fees for services

Expenditure:

Cost of goods sold

Salaries

Insurance

Taxes

Rent

Interest on business loans

- Create your statement using a spreadsheet application. Tools like Google Sheets or Microsoft Excel have P&L templates. With that said, here’s a quick look at some of the basic tips to create a profit and loss statement from scratch.

- Choose a specific period. Are you planning to assess your business progress on a monthly, quarterly, or annual basis? Note that the shorter the time frame, the less meaningful data you will get. By “shorter time frame,” we mean anything less than a month (e.g., daily or weekly). On the other hand, calculating your P&L statement in years can also get overwhelming.

- List your business revenue for your chosen period, breaking down the totals by month. Include your income sources, again, by month.

- Calculate your expenses. Make sure you separate direct costs like OPEX from COGS.

- Determine your gross profit; subtract your direct costs from your revenue.

- Determine if you’re making or losing money. Subtract the total expenses from your gross profit. If you get a positive number, that means your business is making money and is on the right track. When you get a negative number, your business is losing, and you’ll need to assess every area of your operations. Sight the biggest problem that’s holding your small business back. Use the insight that you gather from the profit and loss statement that you created to start setting your business back to the path of profitability.

Examples of a Simple P&L Statement

To wrap up this discussion, let’s take a look at some basic examples of what a P&L statement looks like.

The Simple P&L Statement Example

If you’re running a solo business with little to no diversity in both revenue or expenses, your profit and loss statement might look as simple as this one below:

ABC Company P&L Statement – 2021

- Revenue – $1,000,000.00

- Direct Costs – $700,000.00

- Gross Profit – $300,000.00

- Indirect Expenses – $200,000.00

- Net Profit – $100,000.00

The cost of ‘goods sold’ was subtracted from the ‘revenue’ to give you a gross profit of $300,000.00. The ‘indirect expenses’ are then subtracted from the ‘gross profit to reveal a positive net income (profit) of $100,000.00.

A More Typical P&L Statement

Of course, it’s not always that easy and simple. Most small businesses’ profit and loss statements are a bit more complex than that. Here’s a more realistic P&L statement:

ABC Company (March 2021)

Income

- Gross Sales – $1,200,000.00

- Less: Returns – $200,000.00

- Net Sales – $1,000.000.00

Cost of Goods Sold

- Materials – $200,000.00

- Service Labor – $700,000.00

- Total Cost of Goods Sold – $900,000.00

- Gross Profit – $700,000.00

Expenses

- Advertising – $100,000.00

- Depreciation – $20,000.00

- Insurance – $30,000.00

- Professional Fees – $10,000.00

- Office Expenses – $40,000.00

- Total Expenses – $200,000.00

- Net Operating Profit – $100,000.00

As you may notice, we’ve used the same sample data from the ‘Simple P&L statement’ example to make it easier to see how they line up. The five main totals are in the bold test; however, the ‘ income,’ ‘cost of goods sold,’ and ‘expenses’ are all broken down into multiple line items. Note that under the income category, there’s a line that’s labeled, “Less: Returns.” You will likely see this appear if you look up other examples. This line refers to items that are subtracted from the initial value in a section for clarity.

Ensure Consistent Profit with Automated Recurring Billing

When it comes to the data that you put into your profit and loss statement, every business would want their profits to exceed their losses. That’s why it’s important to ensure that you have consistent and reliable cash flow throughout the year.

While having high-quality products and services is key, one of the most significant yet often overlooked aspects of getting paid is proper, consistent, and efficient invoicing and payment processing. That’s why you need to consider moving towards an automated recurring billing strategy.

Why Recurring Billing is So Popular?

Companies can reduce expenses and streamline their billing process with automated recurring payments. This is because the business knows it will receive a regular payment every month — which means no more human errors associated with invoicing or processing bills on time, as well as no need to pay for an expensive staff that processes bill payments manually. Customers are also protected from billing errors because the automated system verifies every transaction for correct payment.

Businesses can even create separate recurring billing plans with different pricing, discounts, and special promotions to offer their customers more flexibility in choosing a plan that works best for them.

Secure Financial Transactions

Every Transaction is Secure With Recurring Payments: Online businesses using subscription-based models are always at risk of fraudulent transactions. Fortunately, recurring payments are not subject to the same security vulnerabilities as one-time purchases because they’re automatically verified by a secure system before processing each payment.

Manage Billing Cycles with an Automated Recurring Payments System

Businesses can manage their billing cycles easily using automated recurring billing software. By creating a recurring billing plan, businesses can make it easier for their customers to pay on time.

Customers Don’t Need to Open and Act On Invoices Every Month

With automatic payments each month, there is no need for customers to open bills or act on invoices every billing cycle — which saves them time and money. Customers don’t need to remember when bills are due, nor do they have to worry about late fees if the payment is not processed on time. In addition, recurring billing can help customers stay on top of their expenses more easily because all charges will be sent together in one email or statement each month.

Increased Customer Satisfaction

Better Customer Experience with Recurring Payments: Not only does recurring billing increase customer satisfaction, it also provides a better customer experience.

For example, many businesses today offer subscription-based services to their customers which give them access to special features or content on the company’s website. With this type of service, there are no more costly and time-consuming installation fees or software updates; customers simply pay a monthly fee for access.

Customers also appreciate the convenience of signing up online as opposed to visiting physical locations — especially if they’re looking for an automated, hassle-free experience with no hidden costs.

Choose ReliaBills

Recurring billing is great, but only if you use the right software for it. That’s why you should give ReliaBills a try. It’s a superb invoicing and recurring billing platform that provides you with all the necessary tools and features you need to get started with automated recurring billing. At just $24.95 per month, you can upgrade to ReliaBills PLUS to access its recurring billing system.

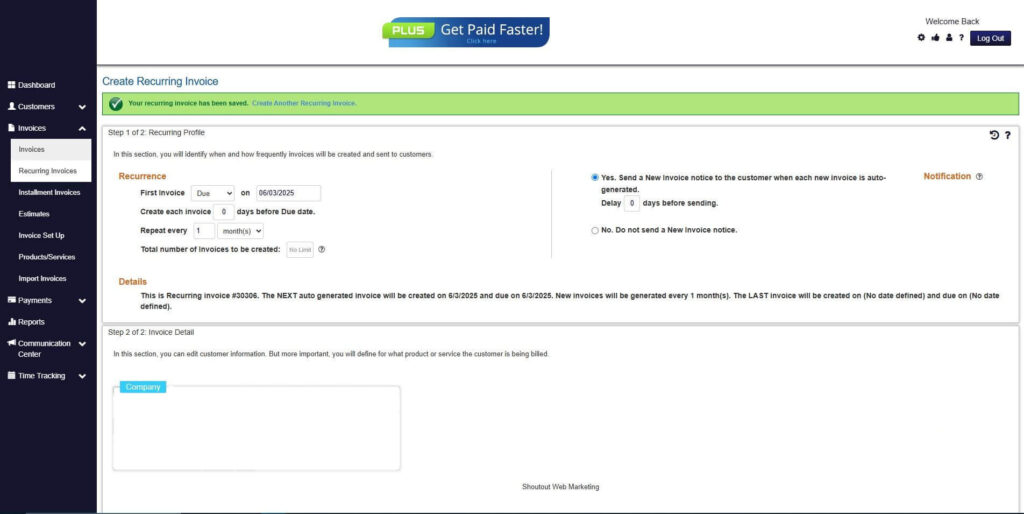

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

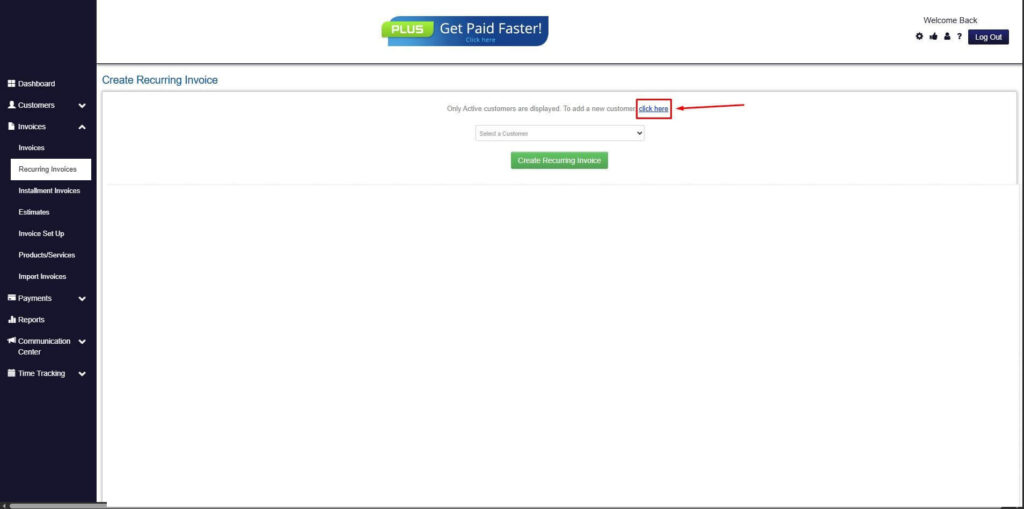

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

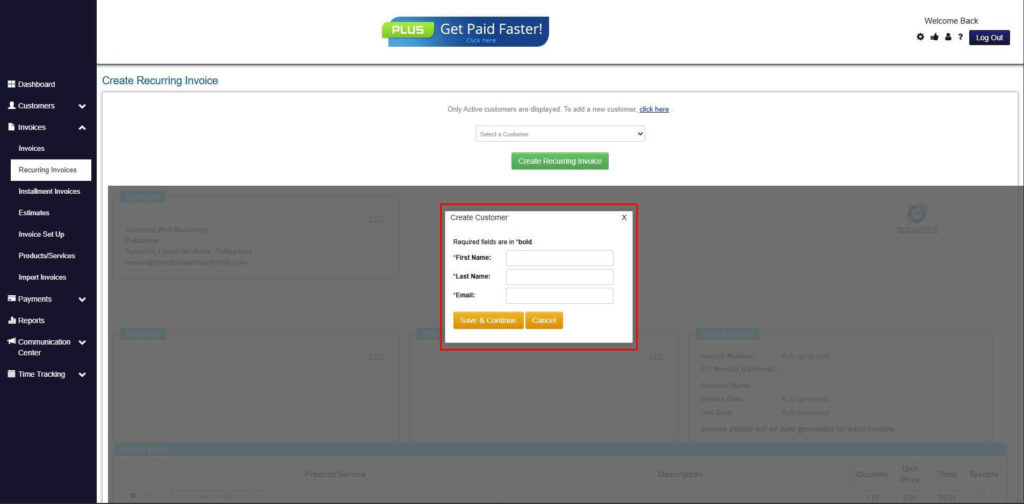

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

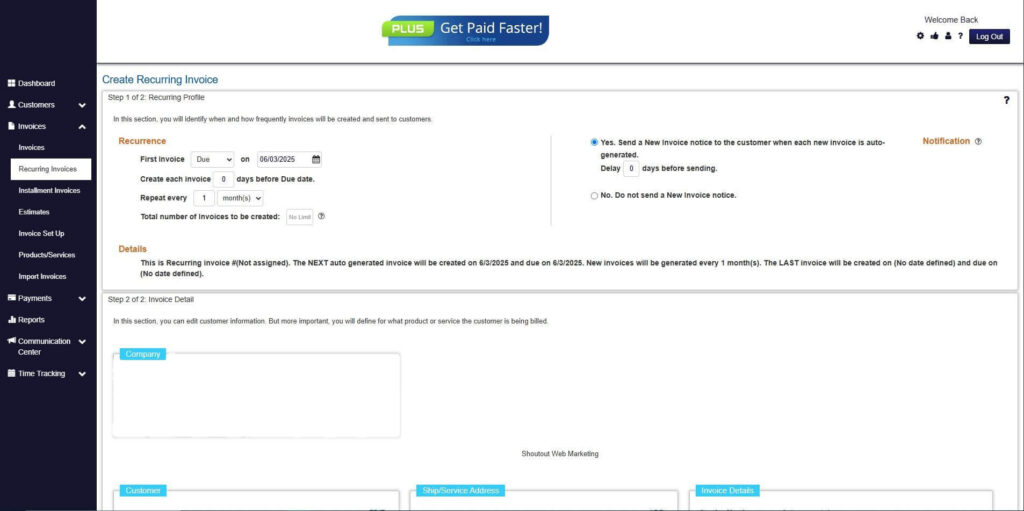

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

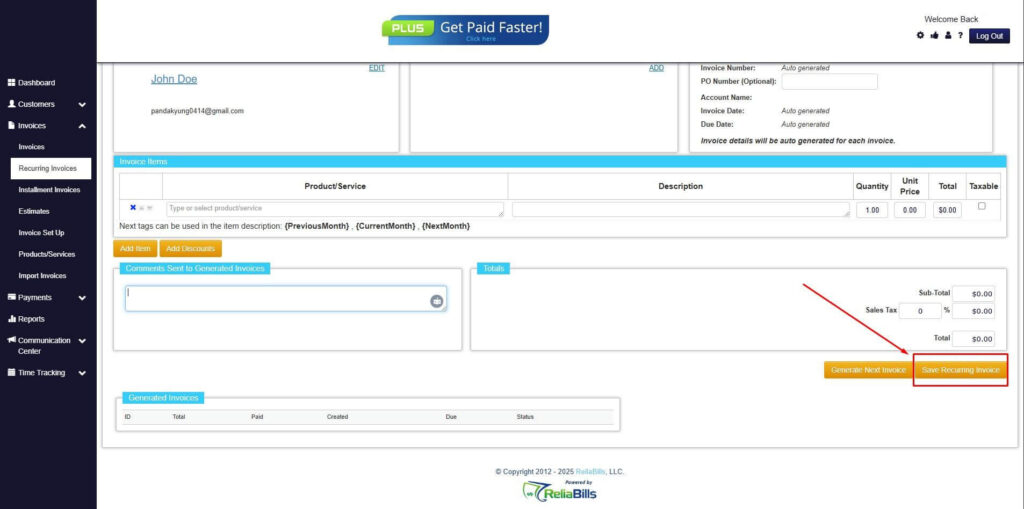

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

- Your Recurring Invoice has been created.

Wrapping Up

A profit and loss statement are an essential tool that every business should use. It provides transparent information about a business’s financial status. If you think that your business is losing, use a P&L statement to verify if your hunch is true. You can also use it to pinpoint areas of improvement to keep your business afloat. We hope this article gave you some valuable information about the profit and loss statement you can now use when running your business.

To stay updated on articles like this one, bookmark ReliaBills in your browser today.