When a business sells goods or offers its services to large clients, such as retailers or wholesalers, it’s usually paid via credit. This process means that the customer doesn’t have to pay for the goods or services it acquires from the business immediately. Instead, the purchasing company is given an invoice that contains the total amount due and its corresponding due date. Business owners are aware of this and are finding ways on how to deal with it.

However, offering credit to customers will tie up funds that the business can otherwise use to grow its operations or invest in other opportunities. That’s why to finance accounts receivables that are slow-paying or meet with short-term liquidity; the business may opt for invoice financing instead. It’s an excellent method that you’re going to learn in this article. First, let’s define what it is and how it can impact small businesses.

What Is Invoice Financing?

According to Investopedia, Invoice financing is a payment method wherein businesses borrow money against the invoice amount due from their customers. Also known as “accounts receivable financing,” this process helps businesses for short-term and long-term success. In addition, it also helps businesses in a lot of ways, specifically the following:

- Improve cash flow

- Pay employees and suppliers efficiently

- Reinvest operations and growth earlier

Invoice financing doesn’t just improve cash flow. It’s also about getting the necessary funds to support your business operations before your customers settle their invoice. If your business has to wait until your customers pay their balances in full, you can potentially stunt your growth and development. In addition, it can also ruin your business operations since you won’t have any funds to use until you are compensated by your clients. That’s why invoice financing is extremely essential.

For invoice financing to work, the business will have to pay a percentage of the invoice amount to the lender as payment for borrowing the money. At the same time, invoice financing can also solve problems associated with customers taking too long to pay. In addition, invoice financing can also solve challenges in obtaining business credits.

Types of Accounts Receivable Financing

To further your understanding of invoice financing, you need to get to know its different types. Currently, there are three:

Invoice Factoring

A common variant among small businesses under industries like clothing or manufacturing. In these areas, long accounts receivables are a normal process in the entire business operations. Invoice factoring provides a cash advance based on the total invoice amount of the unpaid invoices. With invoice factoring, you will typically receive around 50 to 80 percent of the invoice value upfront based on your clients’ risk profile. This process is called invoice discounting. You will then receive the remaining value once the clients settle the invoice, minus a factoring payment. This fee is created in several ways. However, it generally nets out to around three to five percent of the total invoice value.

Standard Invoice Financing

this method involves the same process as factoring. However, the difference is that this one isn’t a sale of your accounts receivable. Instead, standard invoice financing works by using the accounts receivable as collateral to get the advance. Keep in mind that you are fully responsible for managing customer relationships, as well as pay their invoices. That also includes late payments. Once your customer payments are late, you will also be responsible for the amount that you advanced. The fees are usually around two to four percent of your invoice numbers per month.

Receivable Based Line of Credit

This type of invoice financing is based on a percentage of your credit line, which is usually 80 to 85 percent of the value of your customers’ unpaid invoices. Note that the value is calculated based on how the invoices aged. That means they will give a full value for the current invoices while also giving a discount for unpaid invoices. Your invoice factoring company will pay an interest rate based on your current balance. Once an invoice is settled, your balance will reduce. Keep in mind that there will be a fee when you draw the credit line. However, this is usually a cheaper option than the aforementioned invoice financing types with an APR that’s less than 20 percent.

Pros and Cons of Invoice Financing

Similar to other payment methods, there are ups and downs to invoice financing that you also need to know. That’s why, for this section, we will discuss the pros and cons of this type of financing. That way, you can better understand if this payment method is for you:

Pros of Invoice Financing

- If you want the best way to establish a short-term financing method to borrow money, invoice financing is the one for you.

- Since you’re looking to sell invoices, the main focus lies on your actual invoices.

- This can also help remove some of the financial pressure that comes while you wait for your customers to pay back what they owe you.

- The terms from the origination fee to the interest rates make invoice financing the easiest choice when you’re looking to lend money.

Cons of Invoice Financing

- Right of the bat, the most noticeable disadvantage of invoice financing is its high cost.

- While fast approvals help solve your financial problems than traditional loans, the overall cost may lose you a portion of money in the form of fees and other payment obligations.

- The requirement of invoices to be used as collateral to finance can prohibit some types of businesses.

- Business-2-consumer (b2c) businesses looking for financial compensation may be out of luck when using this type of financing.

- Invoice financing is not viable if the business’s cash flow originates at a point of sale instead of long-term invoices.

Best Candidates for Invoice Financing

As has been implied throughout the entirety of this article, invoice financing isn’t for everybody. It can be great for some businesses while detrimental to others. To let you know right away if your business qualifies, here’s a shortlist of the best candidates for invoice funding:

- Business-2-Business (B2B)

- B2B businesses with big-name Clients

- Seasonal Businesses

- Businesses with large invoices and purchase orders

- Businesses under industries with long billing cycles

With that said, here’s another list of the best-suited businesses for invoice funding or financing:

- Agriculture

- Business consulting & legal services

- Manufacturing

- Marketing services

- Real estate

- Retail

NOTE: Invoice funding or financing is not an ideal option for business-2-consumer (B2C) companies (e.g., subscription-based companies, SaaS).

Improve Your Invoicing with Automation

Whether or not your business uses invoice financing to run its operations, you need a smooth and effective invoicing strategy. Due to the internet, manual invoicing is already considered an outdated practice with today’s fast-paced business landscape.

If you’re still invoicing manually, it’s about time to make a change. Embrace the present and future with automated invoicing and simplify your entire billing strategy. That way, you can focus less on asking for payment and more on improving your business as a whole.

Recurring billing is an excellent billing model as it can help businesses get paid on time with minimum errors. This system automates your entire billing process while ensuring that you stay on top of your payments and other receivables.

ReliaBills is an excellent invoicing and recurring billing system that will help your payment processing from start to finish. We can help onboard customers, create ideal pricing plans, and of course, bill your customers. All of these possibilities are available in one platform.

Here’s what ReliaBills has in store for you:

Automated Invoice Creation

As a business owner, your schedule is pretty hectic. The last thing you want is to get glued onto your seat doing invoicing for hours on end. Fortunately, ReliaBills will make sure that you won’t have to do any strenuous invoicing work. Instead, you can save a lot of time by having our system import, generate, and send your invoice automatically. You can schedule your invoicing and even delay it whenever you need to make edits and other changes.

Automated Variable Payments

Customers are the reason your business is still afloat. Without a steady amount of customers, cash flow will soon run dry, and you will be forced to halt business operations. ReliaBills makes sure you keep your customers by enrolling them on AutoPay so that you can collect payment automatically. This level of convenience will impress your customers and give them a reason to stay.

Invoices Designed for Recurring Payments

As you may already know, not all invoices are created equal. Each invoice is explicitly made for a type of job or purpose. However, when it comes to ReliaBills, we make sure that all the invoices you generate are designed for recurring payments. You can include all the details and information you need. Once you’re done, you can set the scheduling to ‘recurring.’ Once you do, your invoices will be sent automatically on the date and time you placed them.

Failed Payment Mitigation

Delayed or nonpayment are the bane of any business. It cripples your cash flow, which will affect your daily business operations. Fortunately, ReliaBills has a way of dealing with problems such as failed payments. Automated payment isn’t 100% perfect. It will still encounter expired credit cards, insufficient funds in the card, closed accounts, and more.

Fortunately, these issues can be resolved immediately with a few edits and changes to the customer’s payment information. Once the system detects a failed payment, ReliaBills will inform the customer right away to make the necessary changes. In addition, ReliaBills will also conduct payment retries to attempt to process the failed payment to ensure that the problem isn’t the system itself.

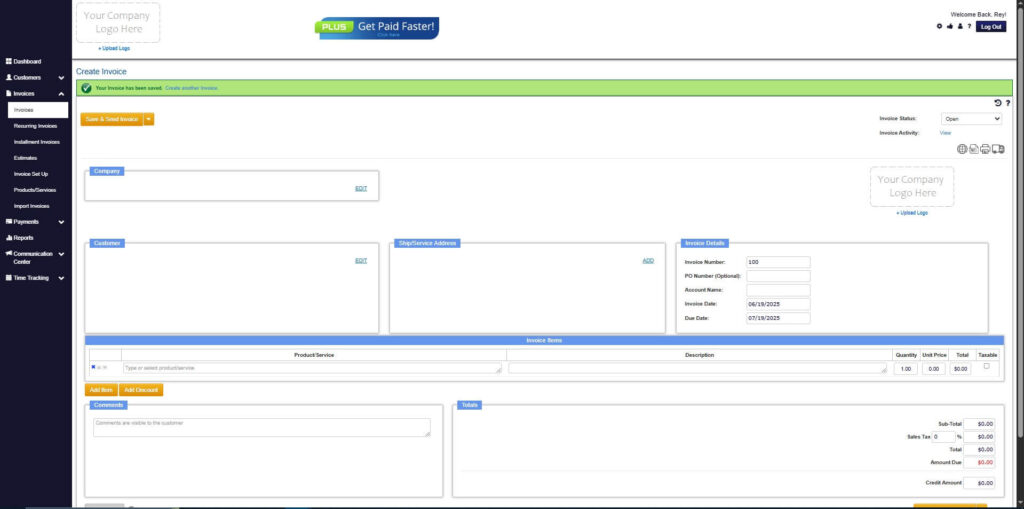

How to Create a New Invoice Using ReliaBills

Creating an invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Invoices

- Navigate to the Invoices Dropdown and click on Invoices.

Step 3: Click ‘Create New Invoice’

- Click ‘Create New Invoice’ to proceed.

Step 4: Go to the ‘Customers Tab’

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

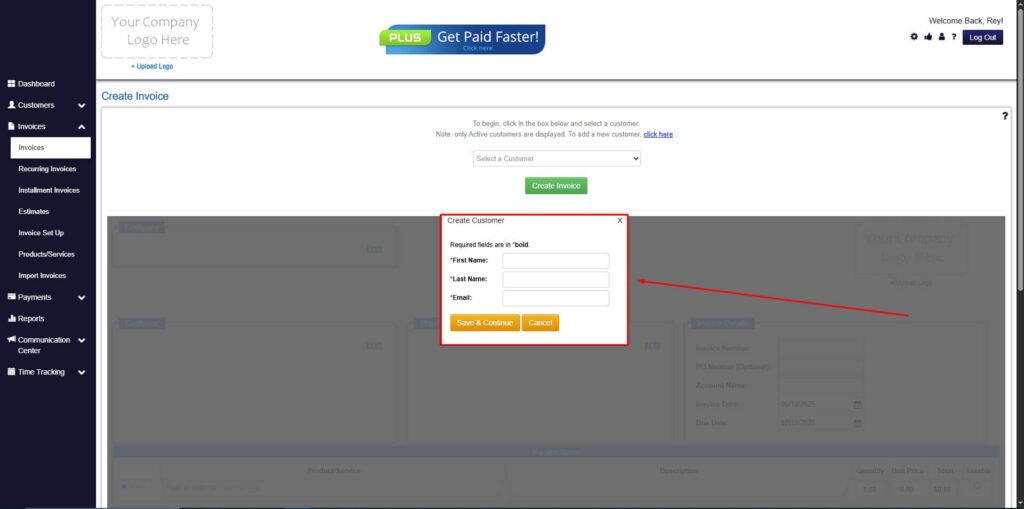

Step 5: Create Customer

- If you haven’t created any customers yet, click the ‘Click here’ to create a new customer.

- Provide the First Name, Last Name, and Email to proceed.

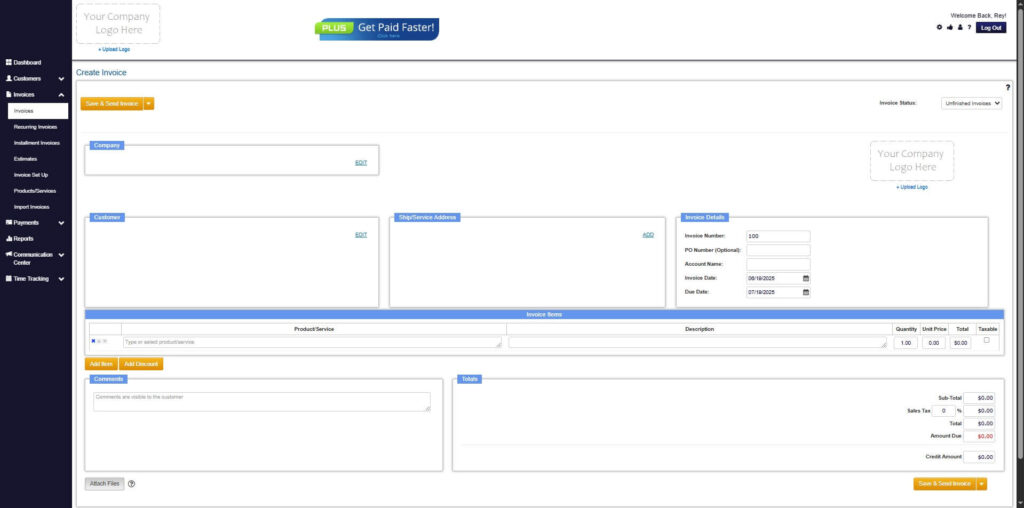

Step 6: Fill in the Create Invoice Form

- Fill in all the necessary fields.

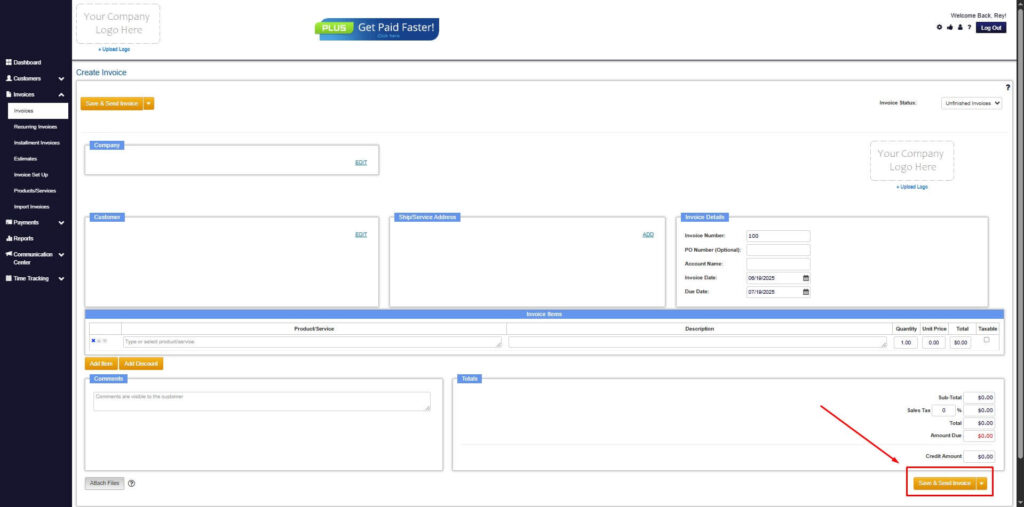

Step 7: Save Invoice

- After filling out the form, click “Save & Send Invoice” to continue.

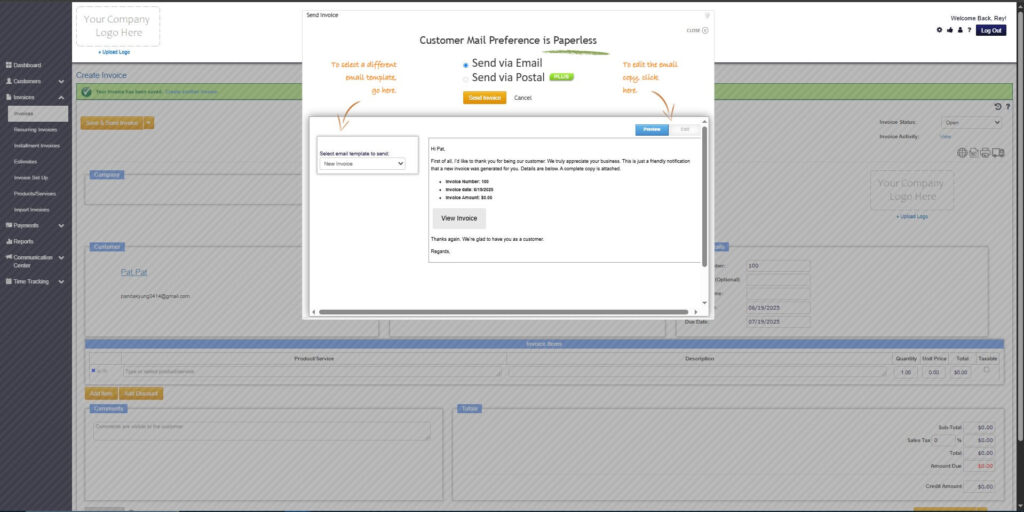

Step 8: Invoice Created

- Your Invoice has been created.

Wrapping Up

This type of financing is an excellent payment method. However, it’s not always a viable option. That’s why the first thing you need to do before you dive deep into this type of financing is determining whether your business is ideal for it or not. Hopefully, this article helped you with that. If you think that your business is fit for this, then you should get started today! For information about ReliaBills and our superb invoicing system, contact us today.