When you’re just starting out your business, online fraud may be the least of your thoughts and worries. However, as you progress from hundreds to thousands of transactions and start accepting payments, skimping on your online security would prove to be dangerous and expensive. In fact, as recent as 2018, surveys claim that US-based merchants have lost a whopping amount of $6.4 billion in payment card fraud alone. It goes without saying that this is a serious matter that needs attention. That’s why in this article, we’re going to go over payment fraud detection and how it can help secure invoicing.

Choosing the Ideal Payment Gateway

Credit card processors offer basic security measures to merchants. That means that even if with it in place, there will still be a significant chance that your business will experience payment fraud loss. For instance, PayPal is one of those merchants that don’t provide seller protection, whether for goods or services. That’s why before you choose a payment gateway to use, determine their level of protection against fraudulent transactions.

With the rapidly evolving digital economy, businesses need to innovate their fraud management strategies. Employing innovative techniques deemed effective is the best way to combat the rising threat of payment fraud. That’s why you must find the ideal payment gateway that will help protect your online invoicing. But first, you need to know how it secures your online transactions and how to choose the right one for your business.

Here are a few effective ways payment gateways reduce online payment fraud losses:

Address Verification Service – AVS

Address verification service, or AVS, is an effective way of detecting online fraud. When people purchase items on your online store, they’ll be required to provide their billing address and ZIP code. An AVS will check if the address provided matches with what the card-issuing bank has on their file. As part of a card-not-present transaction, the payment gateway can then send a request for user verification to the card-issuing bank.

Once the details have been placed, the AVS will respond with a code that will help the merchant determine if it contains a full AVS match. If they don’t match, more investigation will be needed. This can include checking for the following:

- Card Verification Value (CVV, otherwise known as the card verification code).

- Email address

- An IP address on the transaction.

If none of this information matches, then the payment gateway will automatically decline the transaction.

Card Verification Value – CVV

The Card Verification Value (or card verification code) is the three or four-digit code located at the back of every credit card. The code should never be saved and stored on the merchant’s database as it is highly classified. The CVV will act as a filter or added security measure that only allows the cardholder to use the card. The reason is that it’s only available on the printed card. That implies that whoever knows the CVV is confirmed as the owner of the card.

If an order is placed and the CVV does not match, your payment gateway will automatically decline the transaction. When making a card-not-present transaction, merchants will get the customer’s required card information to verify the transaction. Friendly fraud is an example of a risk that’s associated with card-not-present. It can potentially lead to a chargeback. By enabling a CVV filter, you can prevent online payment fraud and reduce the instance of chargebacks.

Device Identification

Device identification focuses on the device that was used to visit the website and make the order. The device used to make transaction range from smartphones, tablets to laptops, and desktop computers. This method profiles essential details about the computer, including the internet connection and browser, to determine if the online transaction has been approved, declined, or flagged.

Every device has a unique device fingerprint, which is similar to that of actual people. It will help identify fraudulent activities, as well as assess any potential risk. Many companies use device identifiers to determine the integrity of a transaction. It helps see if people who have made transactions on a website were previously flagged as suspicious. Since fraudsters and online criminals cannot imitate a computer’s unique identity, device identification proves to be a viable option for protecting your business from online payment fraud loss.

Payer Authentication – 3D Secure

Payer authentication is referred to by two things: MasterCard SecureCode and VeB (Verified by Visa). It is identified as a cardholder authentication measure that helps secure online transactions for each card’s customers. Payer authentication allows cardholders to create a secure code (PIN) that can then be used at checkout to confirm user identity.

By implementing this, merchants will be provided with chargeback protection, as well as cheaper interchange rates. Payer authentication is one of the most effective fraud prevention tools that many businesses use.

Flagging Large Transactions

Fraud artists make the most of stolen card information by making large transactions before it’s blocked. Dealing with large transactions can pose a huge problem to your business since you will have to bear the cost of allowing a suspicious transaction to take place. At the same time, it can potentially lead to a payment processor terminating your processing account. In short, your business will take a massive hit if you let large, fraudulent transactions through.

Fortunately, this can be solved simply by limiting the number of large transactions. You can specify a flat dollar amount, which is essential to avoid chargebacks. You can also limit the number of failed transactions that go through your payment gateway system.

Risk Scoring

Risk scoring tools are based heavily on statistical models that are designed to spot fraudulent transactions based on a set number of rules. Once payment has been made on your website, the tools will indicate the probability of the transaction being fraudulent. A higher probability indicates that you should verify the order. The lower the probability means it’s a safe transaction.

Risk scoring provides a case-by-case evaluation that will flag transactions based on the rules you choose, such as IP range, bulling address, anonymous emails, AVS failure tests, and others.

How ReliaBills Help Prevent Payment Failures

ReliaBills isn’t just a fantastic invoicing system; it’s also has a safe and secure payment gateway that will help reduce the instances of payment failures. Once you use ReliaBills to create and send invoices, you can also take advantage of its payment gateway system to receive payment.

While this is all happening, you will be notified via emails when the invoice has been received, and payment has been made. All of these features make ReliaBills a great payment fraud detection system that you should take advantage of. It’s free, and you can start using it after you’ve created an account.

Recurring Billing Can Also Help

ReliaBills also offers a superb recurring billing system that helps automate your billing and make it more convenient for you and your customers. It may not be a feature that focuses on detecting payment fraud; however, having a strong and secure payment processing system can help prevent the possibility of fraud since you are saving your customers’ payment data and using it whenever you collect payment from them.

It also detects if there are certain issues with a customer’s payment information. The customer will be notified immediately to fix the issue by editing the information that they entered. Once your customers enroll in AutoPay, they won’t have to keep entering their payment details whenever they pay you.

Not only is this feature convenient for your customers, but it also minimizes the chances of mistakes or errors that they commit whenever they pay you. Everything is done automatically so that you won’t have to do it manually.

Why is Recurring Billing Good for your Business?

Recurring billing makes recurring revenue possible, allowing your business to generate consistent cash flow for your company. You can use recurring billing in conjunction with upselling offers like addons, upgrades, or other related products that you offer on a recurring basis (i.e., monthly).

Using ReliaBills will make recurring billing easier than ever. Our recurring billing software system will take care of all the recurring transactions for you, including generating and sending invoices, as well as collecting payments automatically.

Benefits of Recurring Billing

- Improve your cash flow by ensuring that your customers pay every billing cycle.

- Have your customers pay on a regular schedule instead of just paying once.

- Retain more customers by offering recurring billing options.

- Reduce your need to hire employees for recurring billing and invoices since you can automate the process.

ReliaBills is the beacon of recurring billing that will help you improve your billing and your business as a whole. If you’re interested in this billing strategy and want to try it out for the first time, our system will prove to be the best option available out there for you. Are you ready to get started? If so, create your FREE account now and explore the many possibilities of ReliaBills and its recurring billing feature. You can also upgrade to ReliaBills PLUS for even MORE perks.

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

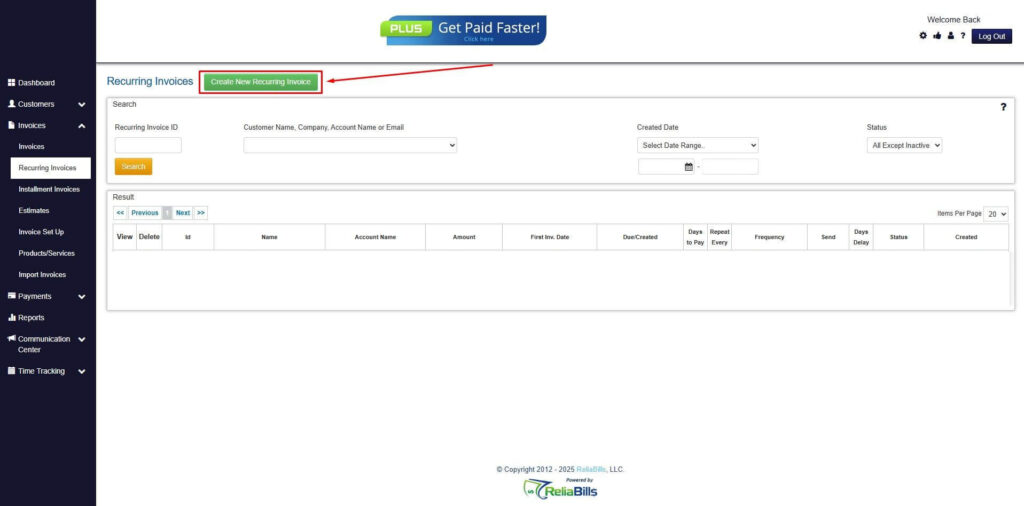

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

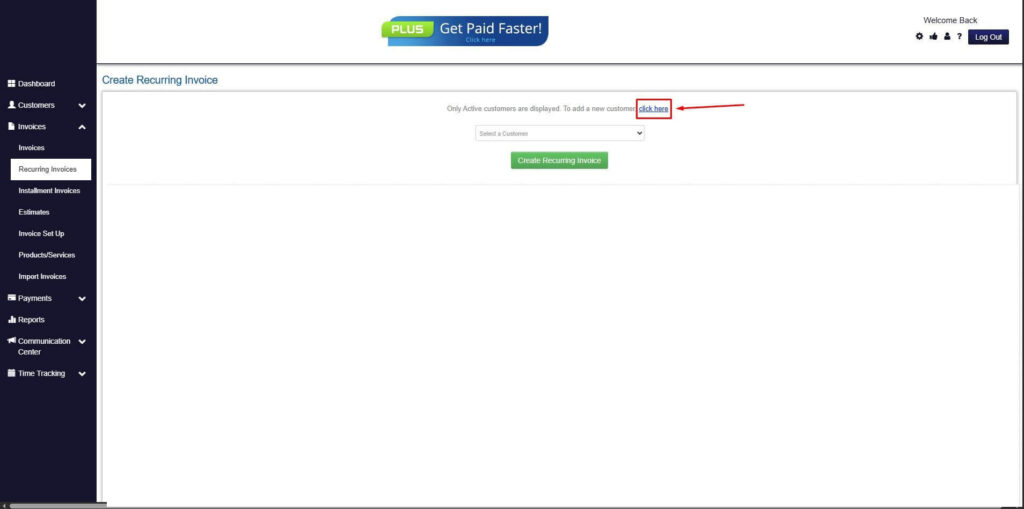

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

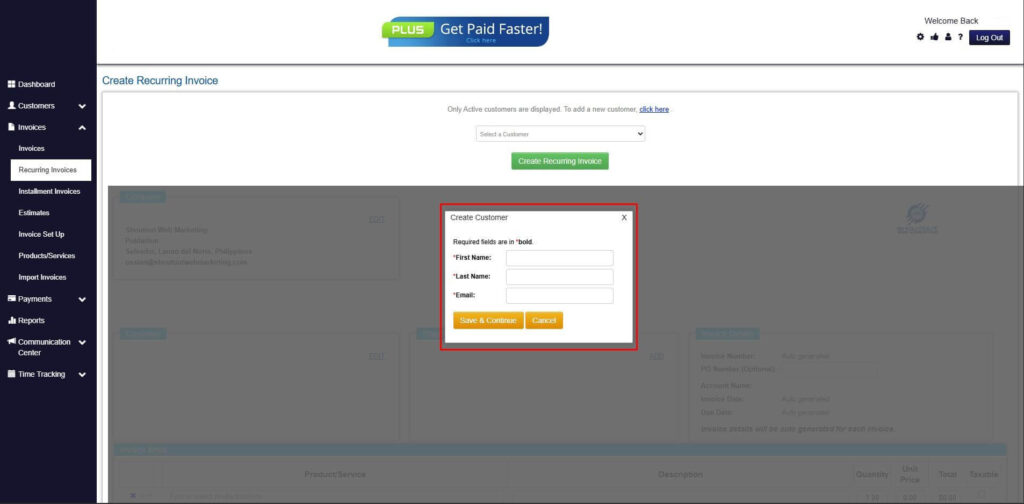

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

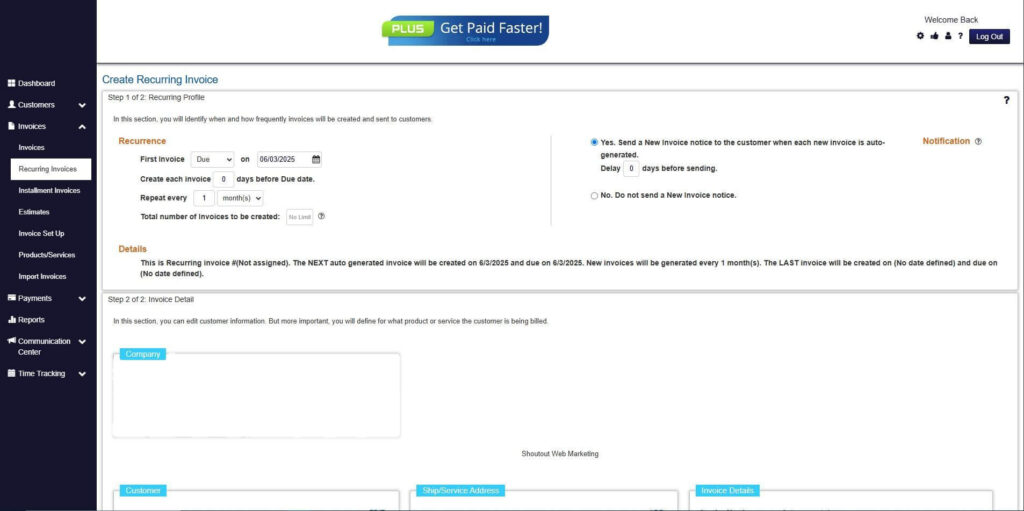

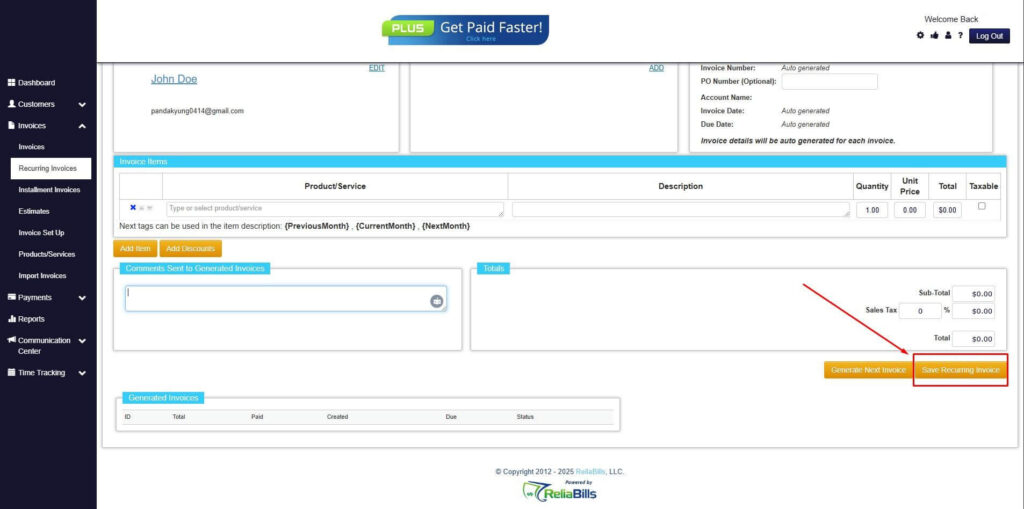

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

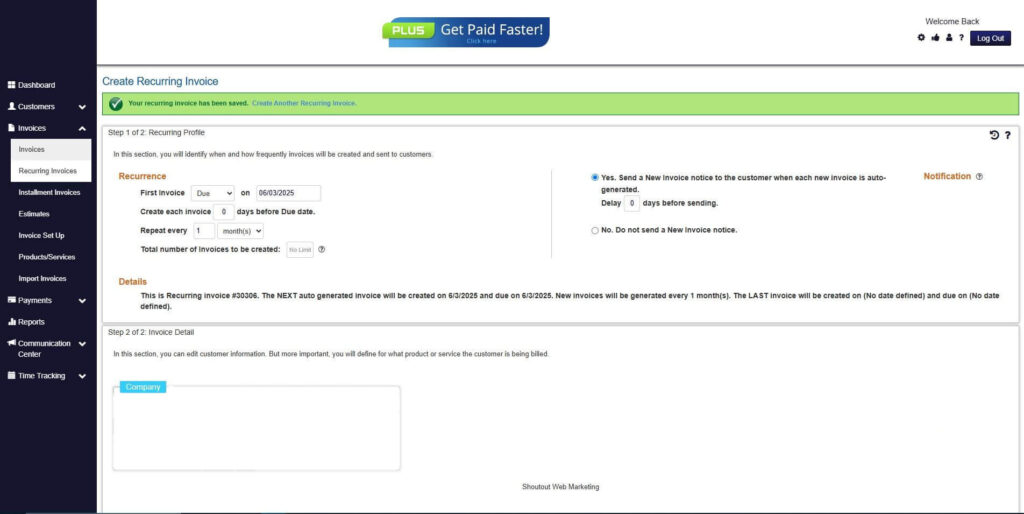

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

Your Recurring Invoice has been created.

Wrapping Up

With business now turning towards a more digitized landscape, payment protection should now be at the top of your priority list. With a safe and secure payment gateway, you can prevent payment fraud loss and chargebacks. At the same time, your business will progress towards a better position when you start using a reliable payment gateway. For more information about ReliaBills, visit www.reliabills.com.