As a small business, it can be hard to compete and keep up with other bigger names in the industry. At the same time, small business owners also contend with a variety of different challenges and issues every single day. Striving to produce high-quality services and products, increase sales, satisfy unhappy customers, and motivate their employees can be stressful. Fortunately, it’s good to know that all of these cash flow problems can be with proper cash flow management. In this article, we will discuss tips on how to how to manage cash flow effectively as a small business. Managing cash isn’t rocket science, but it isn’t as easy as it sounds. That’s why we’re going to show you strategies on how you can improve cash flow management and make sure you can overcome any cash flow problem that you may encounter.

First, we need to discuss what is cash flow, why it’s important, the meaning of cash flow positive, and how to analyze cash flow. That way, you will be able to understand what it is, why the flow of cash into your business is essential, and why proper management is key to all of it.

What is Cash Flow?

So, before we delve deeper into this topic, let’s first discuss what cash flow and cash flow management are. It’s a glance at your business finances during a specific period. It pictures out cash flowing into and out of your business. This concept lets you know how liquid and flexible your enterprise is, all while getting an idea of what it’s relative long-term health is going to be. That’s why you should track and analyze your cash flow on a monthly basis. You can even look at it on a weekly, quarterly, or even annually as well.

The Importance of Cash Flow

So you now know what cash flow is and what it’s all about. But is it that important? Let’s put it this way – cash flow is the lifeblood of an organization. It’s mainly responsible for paying employee salaries, buying supplies, and making investments for business infrastructure. It’s also quite a challenge for small business owners. Those who cannot manage their business cash flow efficiently has a high chance of failing. On the other hand, those who do can improve nearly every aspect of their small business and even develop it into something bigger.

Many small businesses tend to make costly mistakes when it comes to accounting for their cash flow. Bad practices include overestimating sales, failing to track bills, incorrectly allocating resources during startup, and not planning.

Importance of Being ‘Cash Flow Positive’

A part of cash flow management is understanding the importance of being in a cash flow positive state. The primary goal for every business is to make more money than it spends. If you’re on the right path and making more cash than you spend, you’re on your way to ultimate profitability. Once you encounter a problem, your spending (accounts paid) can overtake your income (accounts received) over a period, which can hamper and stress your cash flow.

Here’s an example: let’s say you have $100,000 cash on hand in one month. However, you spend around $150,000 on utilities, employee salaries, rent, taxes, supplies, loans, and raw materials. You sell $200,000 in products or services. From that analysis, you’ve made $50,000.

However, what if that $200,000 doesn’t come in right away. What if the invoice payment process of your top customer is stalled, taking an extra month or two to pay you? All of a sudden, your business is experiencing negative cash flow. Once that happens, you will have a hard time meeting your current financial obligations.

Being in a ‘cash flow positive’ state means that you understand the cash flow of money in and out of your business. You’re making the right decisions and adjustments to compensate for both short and long-term disruptions that can potentially happen. So make sure you place ‘being cash flow positive’ among the topmost echelon of your priorities.

How To Analyze Cash Flow?

If you’re a small business and you’ve never analyzed your cash flow before, you might start by using a simple spreadsheet. Here’s a step-by-step process on how to do that:

- First, determine how much cash you have on hand at the beginning of the time period – which is a particular month of the year. If you have multiple business bank accounts, make sure you add them all together. Put this number at the top of your sheet.

- Second, list all of your payments and income for a month. This list should include all of your costs, like operating, financing, and investment activities. Subtract all of these payments from your cash on hand and add the income to your cash on hand. Use actual income – don’t use invoiced income that you haven’t received yet.

- This process should leave you with a number that’s either larger than the cash on hand at the start (positive cash flow) or smaller than that (negative cash flow). While you might have a negative cash flow for a temporary period, especially if you have some big, one-time expenses, the goal is seeing a positive cash flow each month.

5 Tips To Improve Cash Flow

Now that you know just how important cash flow management and being cash flow positive is, you would want to know different strategies on how to improve your current cash flow. Keep in mind that managing cash flow can be difficult without knowing the effective methods that we’re going to show you. We listed five effective tips for proper cash flow management. That way, you can overcome any cash flow problem that comes your way. Convert sales into cash quickly, all while reducing and extending your payments to build a comfortable cash cushion. Go through each tip and learn how to manage your cash flow properly.

1. Predict and Anticipate What Your Business Needs in the Future

For your business to flourish, you should avoid any surprises by predicting future needs. Your cash flow determines the health of your business. That’s why similar to the human body; you need to anticipate when it will get sick. It’s the fundamental process of proper financial management and something that you need to consider. To improve your cash flow and by predicting the future.

There’s nothing more frustrating than desperately looking for cash. To start with this method, make sure you keep accurate and timely accounting records as they are incredibly essential to understanding your businesses’ financial standing. Make use of your past monthly income and cash flow statements, as well as your balance sheets to measure and calculate your available cash flow and predict likely results for the next months. That way, you will be aware in advance of any potential shortcomings and give you time to prepare for them.

2. Establish Healthy Connections with Lenders

The odds of being able to loan cash or entice investors to put more cash in your business whenever you need it are extremely low. Bear in mind that bankers are least interested in lending to a business that’s in desperate needs since their primary objective is to get paid back. That’s why after making predictions of your cash flow statement in the coming months, you should start establishing goods connections with potential lenders before you need their help and now when you need it. By doing so, you may be able to secure a commitment of future loans.

Most bankers make secured loans assets like the following:

- Accounts Receivable (AR) – is a revolving line of credit that’s based upon a percentage (60% to 80%) of total accounts received. Financing and management are two of the most common ideas on how to manage the flow of cash to your company. The balance due fluctuates up and down as the account receivable varies:

- When sales and account receivables increase; the bank advances more cash flow on the line.

- When sales and AR decreases, you should make payment to bring the loan in line with the negotiated loan-to-accounts receivable-ratio. That way, you will execute proper management, and the flow of money entering your business will be consistent.

- Inventory – Lenders like inventory as it’s expected to be sold and turned into cash. Bankers prefer raw or finished inventory since it’s most marketable in the event of default. Many bankers don’t lend on in-process inventory as additional management and investment are required before it can be sold. Cash flow statement can be slow if these cash flow problems are not fixed right away. Similar to an AR loan, an inventory loan fluctuates up and down as inventory levels alter. A common ratio of loan-to-inventory is around 50%.

- Equipment – While not a short-term loan, owned equipment in good condition can secure a fixed-term loan for a single shot of cash during a crisis. That’s why proper equipment management is necessary. However, keep in mind that the more specialized the equipment, the lower the loan-to-value ratio you may receive. If you have excess or old equipment that’s marketable, sell it for cash. Having an extra amount of cash is more valuable than excess of unused assets. It can ensure that the flow of cash entering your business is consistent and that you’re running your business efficiently.

3. Keep Your Cash Flowing

Cash flow management is all about making sure you keep the amount of cash flow balances in interest-earning accounts. These are available in most banks within the country. There are some cases where you might encounter a minimum balance requirement. However, since the flow of interest rates on these accounts are lower than saving accounts, certificates of deposit, or cash flow market accounts, always consider keeping the largest portion of your funds in higher-paying accounts.

Transfer funds as needed to meet the minimum balance requirement in your interest-earning accounts. Avoid long-term certificates of deposit, which can potentially lock you in for a specific period and hinder the flow of money that goes into your business. The reason for this is that redeeming early can cost you interest. Instead, you should invest in either penalty-free certificates of deposits or commit that portion of funds that you’re unlikely to need during the life of the certificates of deposit.

Set up a different payroll account and establish a bi-monthly cycle. Bi-weekly payroll systems require 26 pay cycles a year, while only 24 for bi-monthly. That means you can save the extra administrative costs of collecting, tabulating, and verifying payroll information. Make sure you require your employees to make direct deposits to reduce the costs of writing and sending checks. Finally, transfer the payroll funds right away before payment to keep your cash earning interest as long as possible.

4. Train Your Customer and Work with your Vendors

As a small business owner, your goal is to collect payment for your services or products before or after incurring the expense of producing or delivering them. The best option is to receive payment via cash on delivery (COD). However, that’s not always a viable option. That’s why you should invoice your customers the day you deliver your product with the note that “payment is expected on invoice receipt.”

Don’t suggest waiting until the end of the month. Include a notification that interests are charged for all payments that aren’t made. Also, make sure you stay on top of your accounts receivable aging, which is a report that categorizes AR according to the length of time that invoices have been outstanding.

Also, make sure you have an established process of following up with late or delinquent payers.

Send these three letters in order:

- An initial form letter ten days following receipt asking for payment.

- A second follow-up letter – with more aggression – in 20 days demanding payment.

- A third and final letter in 30 days to go along with a phone call from your collections clerk seeking payment.

Just as you want your customers to pay you, keep in mind that your vendors want payment as well. However, early payments to vendors can potentially hurt your cash flow; which is why it should be avoided if possible. Delay payment as long as you can while remaining consistent with the terms of the sale. If there’s no penalty for late payments, set a pay cycle of 45 to 60 days from receipt of an invoice. While slowing the outflow of cash is essential, it’s equally important to maintain a good credit rating and cordial relations with your critical vendors.

Always be aware that slowed or delayed payment will result in constant contact with the affected vendor. In those cases, be vigilant that you make all future payments as promised. If you’re forced to delay payments, contact the vend as soon as possible with an explanation, as well as a plan, to become current and active with paying your debt.

5. Maximize Cash Inflows While Sinking Outflows

Finally, you should consider the simple concept of maximizing the cash that goes into your business than the amount of money that goes out of it.

If you work with contracts, set up payment schedules and amounts that parallel or exceed your sunk costs. If your customer demands modification of standard products or services that have not been identified in your contract, seek additional payment through fees or change orders.

Small businesses that offer regular service or product should also consider subscription sales whereby customers are required to prepay. Magazines, Landscaping, cable television, and any type of maintenance service are good examples of companies that can make good use of a subscription model. In addition to receiving upfront cash to cover future costs, you also have the advantages of securing future sales and easier resource scheduling.

Layaway programs have also returned in vogue as an alternative to sale and payment plans. A layaway program will allow customers to choose a specific product, which is then reserved for future purchases and deliveries when payment has been completed. That way, the seller will use the cash prior to incurring the product’s cost.

Reducing the amount of outflows is simply making sure your expenses are lower than the cashflow that goes into the business. Cash flow problems arise once you’re spending more than what you’re earning. Your expenses will balloon and you won’t any progress with your business. Keep in mind that cash flow problems are normal. What’s not normal is tolerating these cash flow problems instead of finding a solution. Fortunately, we’re here to help you in managing cash flow.

Here are some of the ways that will allow you to save more on your daily business operations and reduce overall outflow:

- Don’t Replace Capital Equipment; Repair It Instead. You can save money by having regular maintenance on all of your equipment. You can use reconditioned replacement parts from third-party suppliers instead of factory new parts—partner with a local repair facility to handle jobs that are too big or complex for in-house personnel.

- Buy Used Equipment. There is plenty of used equipment that is still in good condition and are priced for less than a new one. Take advantage of that opportunity and save a lot of money on equipment costs. Search local advertisements and actions in your area. Make sure you look for companies whose assets have been foreclosed and are being sold by a lender.

- Delay Product Upgrade Until Absolutely Necessary. It can be tempting to buy upgrades when you have the money. But if you’re trying to reduce the outflow, then you might want to consider delaying any upgrades until you absolutely need it. Anticipate the lifespan of your equipment and make sure you purchase a new product before it breaks down. That way, business operations will not be affected even if you’re delaying any potential upgrades.

ReliaBills Can Help with Cash Flow Management

Proper cash flow management is the key to success, no matter what business you’re running. As long as you understand the importance of cash flow management, running your business will be smooth sailing moving forward. If you want to make flow management easier and hassle-free, you should try out ReliaBills.

Invoicing is an integral part of cash flow management as it’s the document that’s sent to the customers before payment is made. That’s where ReliaBills comes in handy.

How ReliaBills Can Help Improve Your Cash Flow Management

ReliaBills can provide tremendous assistance to your business operations by making your invoicing process easier and hassle-free. We can help create and send a unique invoice to ensure you get paid on time for your goods or services. As a result, you will be able to have a consistent cash flow for your thriving business.

If you’re not yet aware, recurring billing or recurring payment is a payment model where the customer gives full authorization to the merchant to acquire funds from their accounts automatically at regular intervals in exchange for the goods or services provided to them. Since it’s ‘recurring,’ this process will be continuous until the customer cancels their subscription to the business.

How Does It Work?

A recurring payment system automatically collects payment from the customer’s account via credit or debit cards or other methods like direct debit and ACH fund transfer. Your business must have a payment service provider to go along with a merchant account for this to work.

A merchant account is a different type of bank account. It’s not the same as a standard business account. It will accept automated payments from your customers’ accounts. That means the amount coming from your customers’ accounts will be deposited to the merchant account first before being transferred to the business’s actual bank account.

The payment service provider will handle the payment processing duties from collecting recurring payments, processing them in a safe and secure payment gateway to depositing the funds to your business bank account.

Keep in mind that each recurring payment processor will have varying workflows.

However, they typically follow these general steps:

- Customer chooses the recurring payment mode from a list of options

- A customer accepts the terms and conditions associated with the preferred recurring payment option.

- The customer will enter their card details to make an initial payment. Their payment information will then be saved on the payment gateway page for subsequent or future transactions.

- A corresponding invoice will be sent to the customer at the end of every billing cycle in accordance with the predetermined payment schedule.

- Payment will then be processed, and the funds will be transferred to the merchant account. However, this will only happen once the acquiring and the issuing bank approves the transaction.

- The customer will then be notified about the status of the recurring payment transaction. If the payment fails, an automated follow-up instruction will be sent to them about how they can resolve the issue.

- Recurring billing ensures that your customer won’t have to enter payment details again. Every step will be automated until your customer cancels their subscription.

Benefits of Recurring Payment

Apart from it improving and stabilizing your cash flow, recurring billing also offers the following benefits:

Reduce late payments and collection time

Late payments are detrimental to any developing business. They affect your customer relationship and revenue potential. With recurring billing, you can rest assured that payment collection will be automated and prompt based on your predefined schedule. At the same time, your business will also spend less time reaching out to customers and having awkward conversations about their late payments.

Minimize Effort

A recurring billing system like ReliaBills is fully automated. It cuts down the cost and effort of your invoicing and payment processing duties by at least 50%. The only challenge you’ll need to face is setting it up the first time. Once you’re all set, our system will handle the rest. The only time intervention will be needed is when you need to change the payment type and the amount charged, which you can do any time you want.

Prevent Fraud

Recurring payment data is processed and stored in integrated payment gateways. These servers protect your business against fraud with payment card industry (PCI) compliance and tokenization methods. These technologies help detect and prevent fraud, defend your business from fraudulent activity, and reinforce a more trustworthy image among your customers. ReliaBills and its recurring billing strategy have a lot in store for you and your business.

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

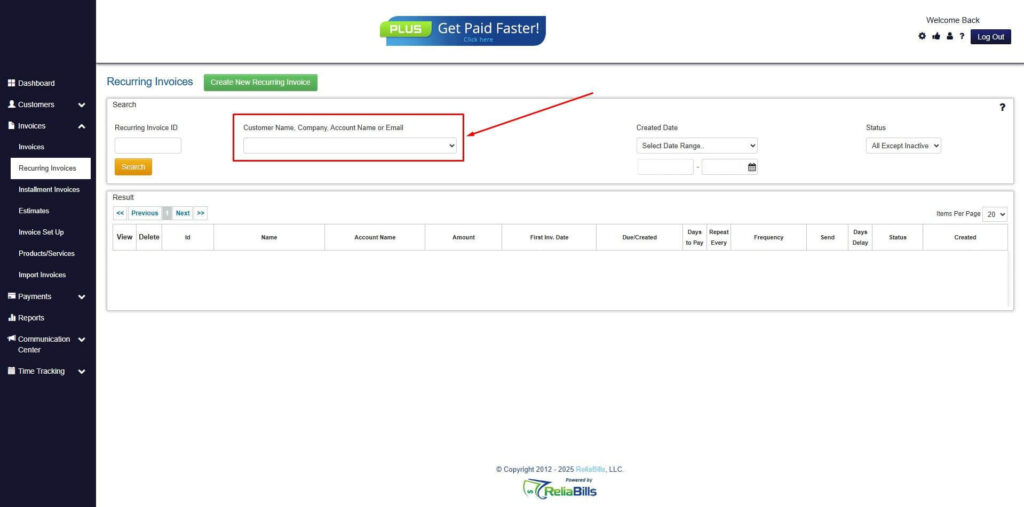

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

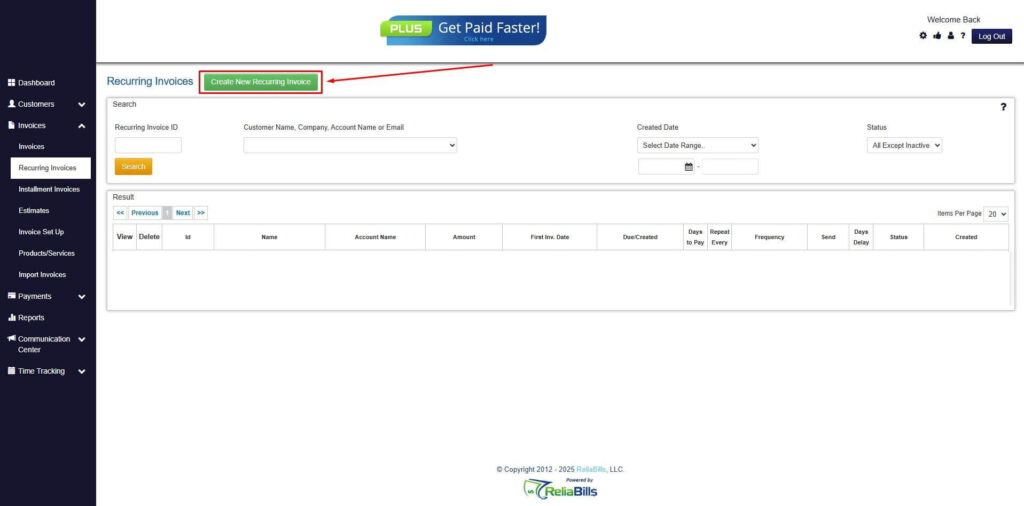

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

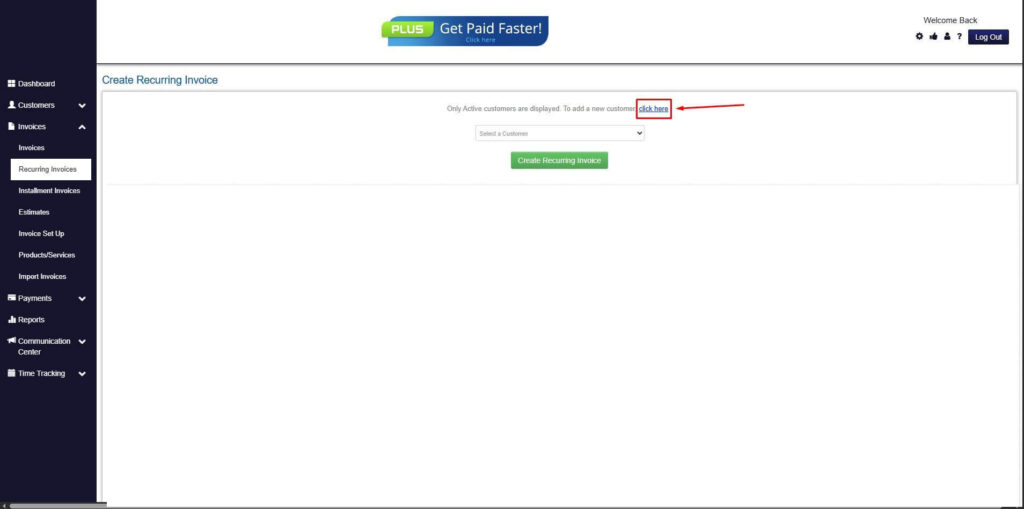

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

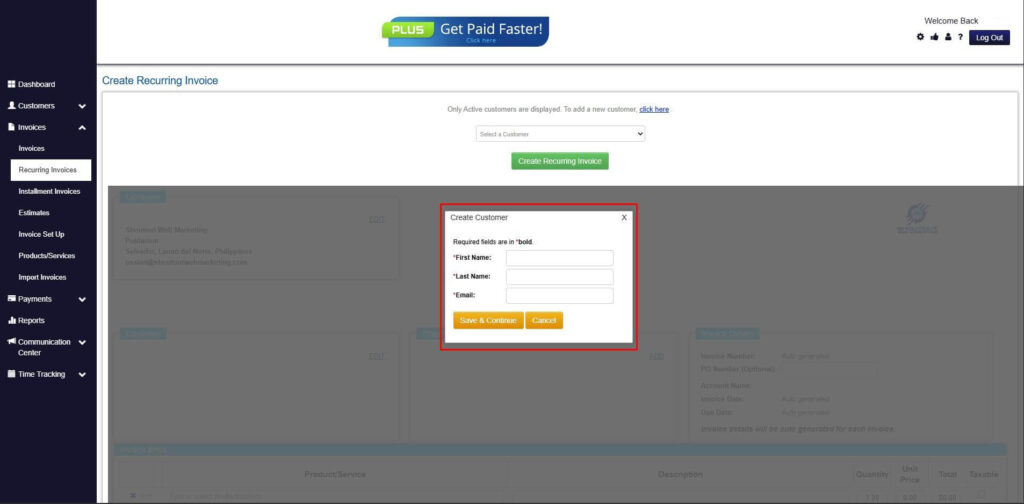

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

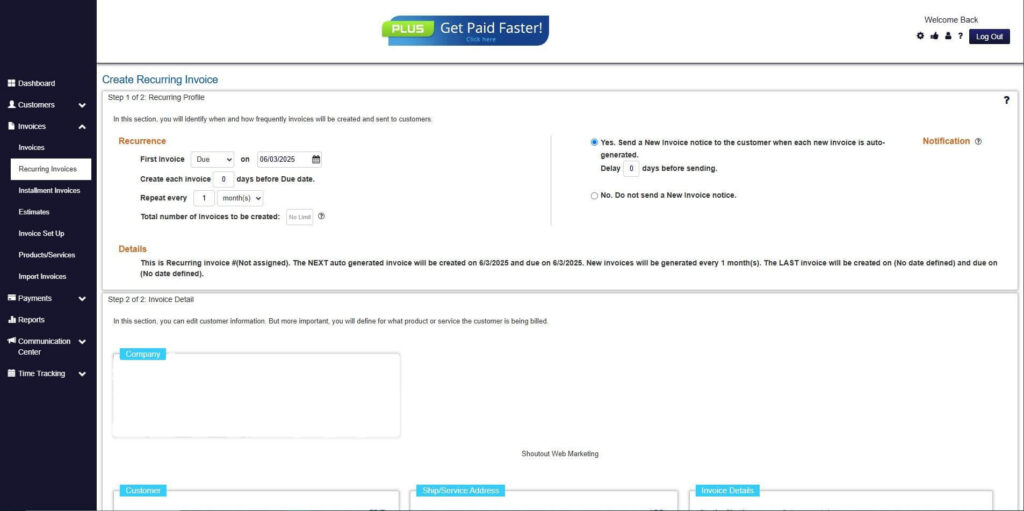

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

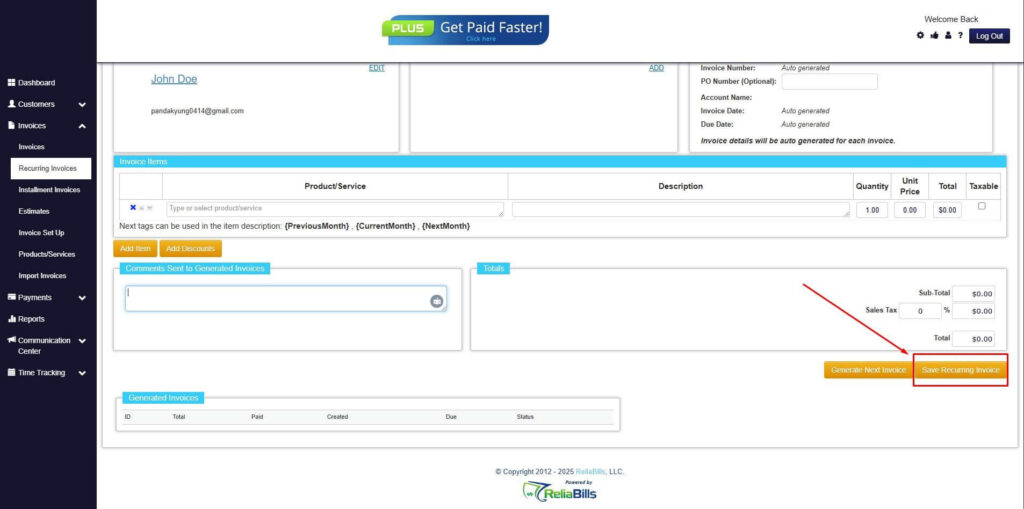

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

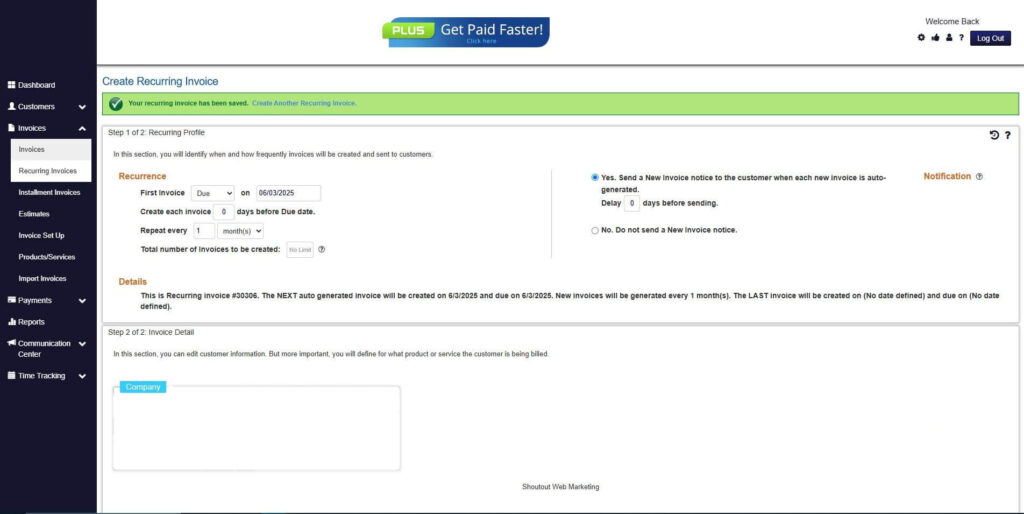

Step 9: Recurring Invoice Created

Your Recurring Invoice has been created.

Wrapping Up

ReliaBills is a comprehensive invoicing system that allows you to schedule and send your invoices like a true professional. You can customize your invoice template and make it unique to your company, schedule your invoices to make sure it is sent to the recipient on time, and get notifications once payment is made.