Can a merchant reverse a refund? In the world of ecommerce, payment reversals can be a huge headache for merchants. Whether it’s a card-not-present or recurring transaction, there’s always a chance that a cardholder may dispute a payment. If that happens, the merchant can often find themselves on the losing end.

Fortunately, merchants can do a few things to defend themselves against payment reversals. By understanding the rules and regulations around payment reversals, merchants can put themselves in a better position to fight back against them.

This article will look at how can a merchant reverse a refund to defend themselves from payment reversals and protect merchant revenue.

What Are Payment Reversals?

A payment reversal, also known as a reverse transaction, is when a cardholder disputes a transaction and requests a refund from the merchant. This can happen for various reasons, but most often, it’s because the cardholder believes the transaction was fraudulent or that they were overcharged.

Payment reversals can be a real pain for merchants, especially if they’re not prepared for them. Not only can they lose out on the sale, but they may also have to pay fees to the card issuer. In some cases, the merchant may even be liable for the entire amount of the disputed transaction.

Types of Reverse Transactions

There are three primary types of reverse transactions: an authorization reversal, a refund, or a chargeback:

Authorization Reversal

The first form of payment reversal is called an authorization reversal. This is when the cardholder contacts the merchant and requests that the funds for a transaction be returned. Once approved, the merchant can then process the reversal and refund the cardholder.

The main advantage of an authorization reversal is that it’s the quickest and easiest way to process a refund. The entire process can be completed in a few days, and the merchant doesn’t have to pay any fees.

However, there are a few drawbacks. First, the cardholder can only request an authorization reversal if they haven’t received the purchased goods or services. Second, the cardholder can only request a reversal within a certain timeframe.

Refund

The second form of payment reversal is called a refund. This is when the merchant initiates the refund rather than the cardholder. Refunds can be given for various reasons, but they’re often given because the cardholder is unhappy with a purchase.

The main advantage of refunds is that they can be given any time, for any reason. This gives the merchant a lot of flexibility when it comes to processing refunds. Additionally, the merchant can often avoid paying fees by issuing a refund.

However, there are also a few drawbacks to consider. First, the merchant may have to eat the cost of the transaction if they can’t recover the funds from the cardholder. Second, refunds can take a long time to process, which can be frustrating for both the merchant and the cardholder.

Chargeback

The third and final form of payment reversal is called a chargeback. This is when the card issuer initiates the refund rather than the cardholder. Chargebacks can be given for various reasons, but most often, they’re given because the cardholder believes the transaction was fraudulent.

The main advantage of chargebacks is that they can be processed quickly. Additionally, chargebacks can be issued for any reason, which gives the cardholder a lot of protection.

However, just authorization reversal and refund, there are a few drawbacks. First, the merchant may have to pay fees to the card issuer. Second, chargebacks can be very difficult to fight, and the merchant may not always win.

What Causes Payment Reversals?

There are a variety of reasons that payment reversals can occur. Of course, the most common reason is fraud, but chargebacks can also be caused by things like customer disputes, technical errors, and even friendly fraud.

Fraud

The most common cause of payment reversals is fraud. Fraud can happen in various ways, but most often, it occurs when the cardholder’s information is stolen and used to make a purchase.

Customer Disputes

Another common cause of payment reversals is customer disputes. A customer dispute can occur when the cardholder is not satisfied with a purchase or when they believe the transaction was fraudulent.

Technical Errors

Technical errors can also cause payment reversals. A technical error can occur when the merchant processes a transaction incorrectly (e.g. the information entered was incorrect).

Friendly Fraud

Finally, payment reversals can be caused by friendly fraud. Friendly fraud occurs when the cardholder knowingly makes a chargeback for a purchase that they actually made. This can happen when the cardholder is unhappy with the item or when they want to get their money back for any reason.

How Can Merchants Defend Themselves from Payment Reversal?

Can a merchant reverse a refund? No business wants to deal with payment reversals. But unfortunately, they’re a reality of doing business as they can happen anytime. There’s no stopping them from occurring. However, there are a few things you can do to minimize the risks and defend your business:

Ensure Information Populates Correctly

Some information fields identify and track data with each authorization. Some examples would include the following:

- Transaction Identified (TID): links authorization to subsequent transaction messages.

- Surface Trace Audit Number (STAN): Identifies all messages associated with a cardholder transaction.

- Retrieval Reference Number (RRN): Links estimated sales to the original authorization request.

- Authorization Characteristics Indicator: Specifies an incremental transaction total.

- Duration Field: Number of estimated days during which charges will be tabulated.

Ensuring that you get all transaction data in the right information field before submitting. Otherwise, you can have issues with information not matching up and can create an invalid transaction.

Get Authorization for All Transactions

Payment processors require merchants to get authorization for all card-not-present and ecommerce transactions. An authorization code confirms that the cardholder has the funds to pay for the purchase. If you don’t get authorization, you can be held liable for any chargebacks.

Store Customer Data Securely

If you’re storing customer data, it’s important that you do so securely. You should never store full credit card numbers or expiration dates.

Additionally, you should always use a secure server when storing customer data. A secure server uses encryption to protect data from being accessed by unauthorized individuals.

Confirm Projected Clearing Data

Sending an email confirmation after an order has been placed is standard practice. This confirmation should include the customer’s name, purchase amount, and projected clearing date. The projected clearing date is when the funds will be deducted from the customer’s account.

Deflection

Deflection is an ideal solution to protecting merchant revenue but can be difficult to achieve. Deflection is identifying and stopping a payment before it gets processed. If a cardholder is attempting a chargeback fraud, you can use deflection to stop the payment before it goes through.

Representment

While it isn’t ideal, representment does serve as the last line of defense against payment reversals. Representment is the process of disputing a chargeback and providing evidence to show that the transaction was valid.

Following these tips can minimize the risk of payment reversals and help defend your business against them.

ReliaBills Can Help Protect Your Business Against Payment Reversals

If you want to reduce the amount of payment reversals, consider using ReliaBills—one of America’s leading invoicing and payment processing solutions. With ReliaBills, you have a safe and secure system that can help you get paid on time.

With ReliaBills, you have a comprehensive system that can help you process payments and deal with potential issues like payment reversals. Our systems offer the following features to help you combat payment reversals:

- Chargeback recovery: ReliaBills will help you recover lost revenue from chargebacks and payment reversals.

- Recurring payments: You can set up recurring payments to get paid on time, every time.

- Invoicing: Send invoices directly to your customers to help streamline the payment process.

- Automated Failed Payment Recovery: Automatically retries failed payments so you can get paid, even if the initial payment fails.

- Auto Bill: Get paid faster without delays by automatically storing customer payment information and billing.

ReliaBills can help you reduce the risk of payment reversals and get you paid on time. To learn more about how ReliaBills can help your business, visit our website at www.reliabills.com or give us a call today. We’re here to help you deal with payments and reduce payment reversals!

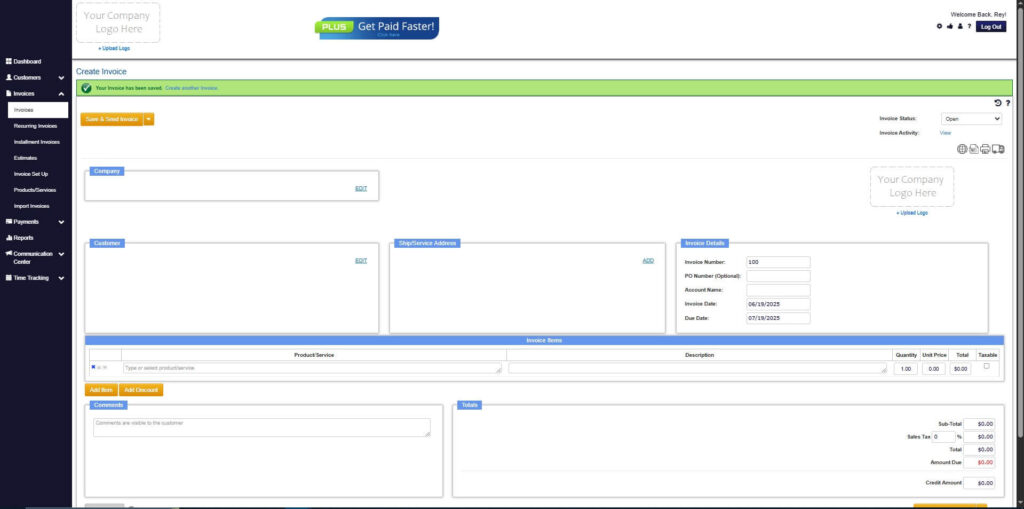

How to Create a New Invoice Using ReliaBills

Creating an invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Invoices

- Navigate to the Invoices Dropdown and click on Invoices.

Step 3: Click ‘Create New Invoice’

- Click ‘Create New Invoice’ to proceed.

Step 4: Go to the ‘Customers Tab’

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

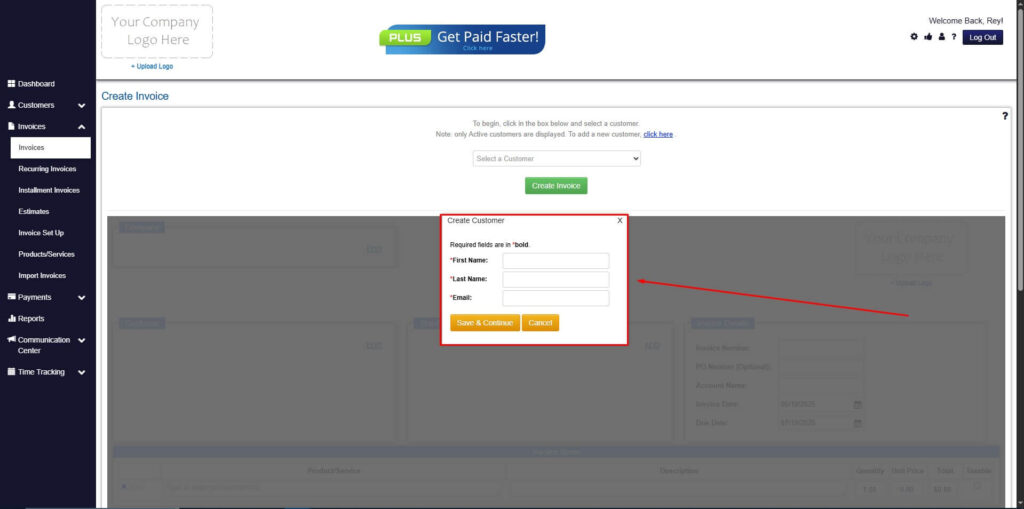

Step 5: Create Customer

- If you haven’t created any customers yet, click the ‘Click here’ to create a new customer.

- Provide the First Name, Last Name, and Email to proceed.

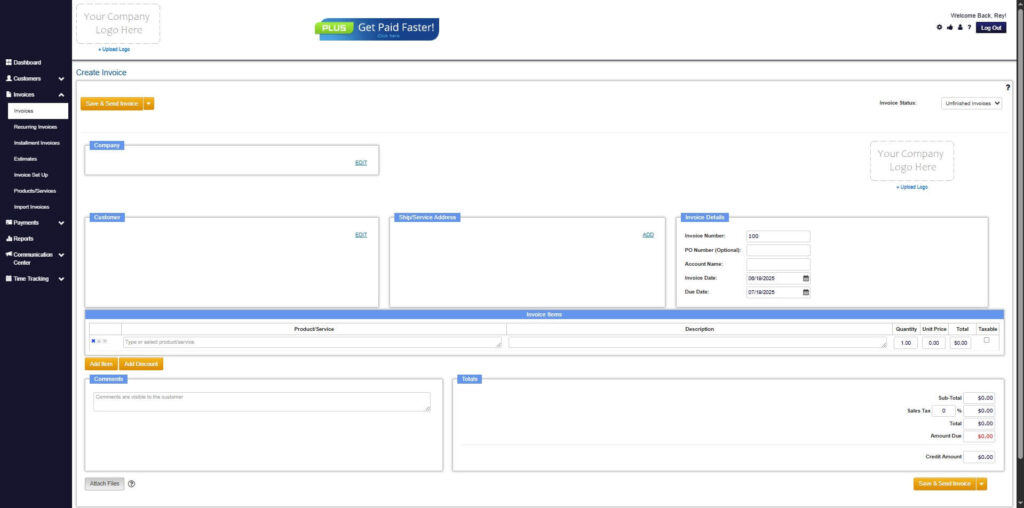

Step 6: Fill in the Create Invoice Form

- Fill in all the necessary fields.

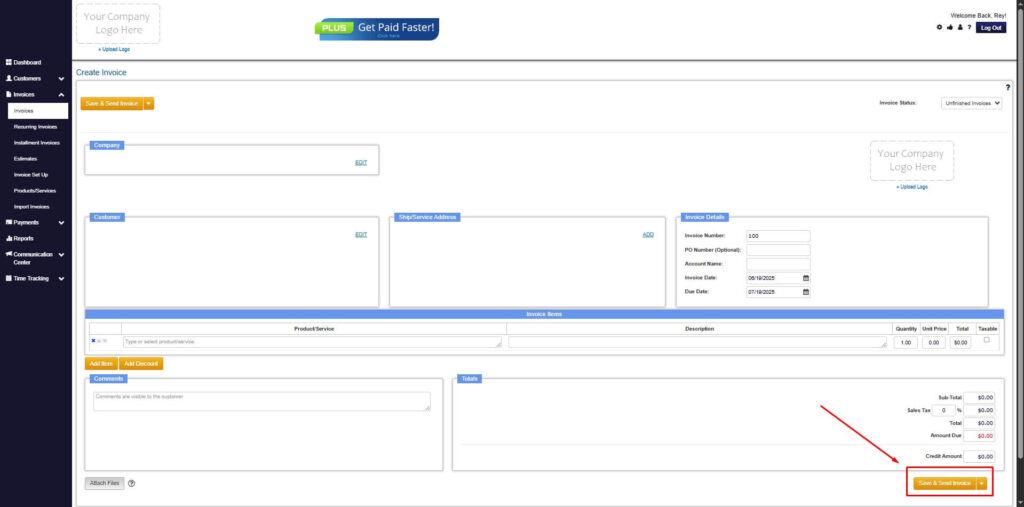

Step 7: Save Invoice

- After filling out the form, click “Save & Send Invoice” to continue.

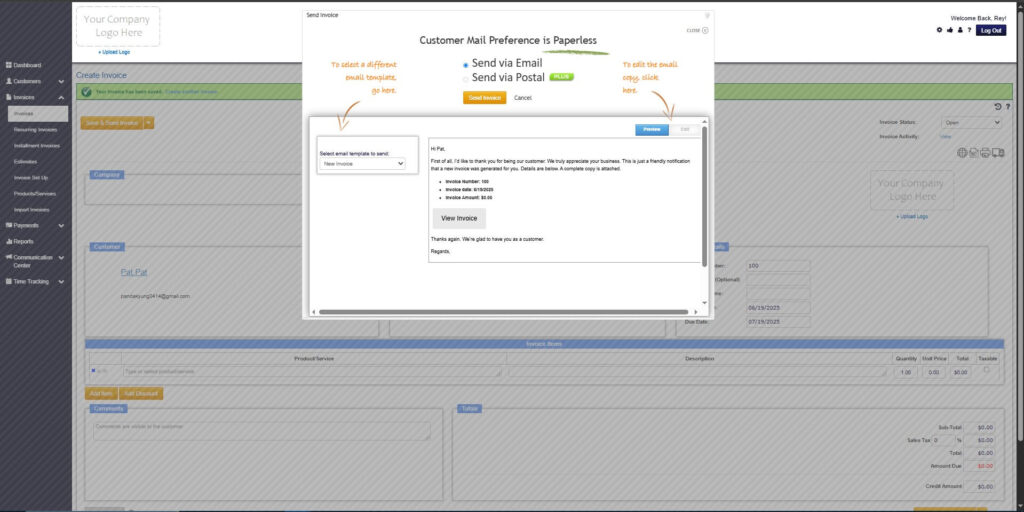

Step 8: Invoice Created

- Your Invoice has been created.

Wrapping Up

To answer the question “Can a merchant reverse a refund?” Payment reversals are the worst. But by following the tips above, you can help reduce their occurrence and better defend your business against them. If you want to protect your business further, consider using ReliaBills. With our invoicing and payment processing solution, you can get paid on time, all while reducing the risk of payment reversals.