Cash flow is the operational lifeline of every small business. Even companies with strong sales and growing demand can struggle financially when payments are delayed. The time gap between issuing invoices and receiving payment often creates stress that impacts daily operations.

Many small businesses extend payment terms to remain competitive. Net 30, 60, or 90-day agreements are common across industries such as manufacturing, logistics, consulting, and wholesale trade. While these terms support client relationships, they also tie up working capital.

Because of this gap, financial tools like invoice discounting for small businesses have become increasingly popular. Instead of waiting for customers to pay, businesses can access a portion of their receivables immediately and maintain smoother operations.

What Is Invoice Discounting?

Invoice discounting is a short-term financing solution that allows businesses to borrow money against unpaid invoices. Rather than securing funding through fixed assets or long credit histories, the business uses its outstanding receivables as collateral.

This method differs from traditional loans because it is directly tied to active sales performance. As invoice volume increases, available financing capacity also increases. That flexibility makes it attractive to growing businesses with consistent billing activity.

Invoice discounting for small businesses is especially useful for companies that operate in B2B markets. Since larger corporate clients often negotiate extended payment terms, receivables can represent a significant portion of locked-up capital.

How Does Invoice Discounting Work?

The process begins when a business delivers goods or services and issues an invoice to the customer. Instead of waiting weeks for payment, the business submits the invoice to a financing provider for review.

After verification, the lender advances a percentage of the invoice value. This advance typically ranges between 70 and 90 percent, depending on customer creditworthiness and industry risk.

When the customer pays the invoice in full, the lender deducts agreed-upon fees and releases the remaining balance to the business. The company regains full access to its revenue, minus financing costs. This cycle can repeat continuously as new invoices are issued.

Invoice Discounting vs. Invoice Factoring

While both solutions provide cash based on receivables, their structure differs significantly. In invoice discounting, the business retains control of collections and customer communication. The financing arrangement is often confidential, meaning customers are unaware of it.

In contrast, invoice factoring typically involves transferring collection responsibilities to the factoring company. Customers are notified to pay the factor directly. This structure can influence how clients perceive the business relationship.

Fee structures also vary. Factoring often includes higher service costs because of outsourced collections. Invoice discounting for small businesses may offer lower fees but requires strong internal credit control systems.

Why Do Small Businesses Experience Cash Flow Gaps?

Extended payment terms are one of the most common causes of liquidity challenges. Even if invoices are accurate, clients may delay payment until the final due date or beyond.

Seasonal sales fluctuations also contribute to inconsistent income. Retail, construction, and tourism-based businesses often generate revenue unevenly throughout the year. During slow seasons, receivables may not cover fixed expenses.

Upfront operational costs such as payroll, rent, utilities, marketing, and inventory purchases must be paid regardless of client payment schedules. When multiple clients delay payment simultaneously, financial pressure increases rapidly.

How Invoice Discounting Improves Cash Flow

Invoice discounting for small businesses converts accounts receivable into immediate working capital. This shortens the cash conversion cycle and improves liquidity.

Faster access to funds allows businesses to pay suppliers on time, negotiate early payment discounts, and avoid high-interest emergency loans. It also reduces the risk of missed payroll or delayed operational spending.

With stable cash flow, businesses can focus on growth rather than survival. Investment in marketing campaigns, technology upgrades, and staffing becomes more manageable when revenue timing is predictable.

What Are the Costs and Risks of Invoice Discounting?

Service Fees and Discount Charges

Financing providers charge a percentage of the invoice value as a service fee. This fee may be calculated weekly or monthly until the invoice is paid. Over time, these costs can reduce overall profit margins, especially for businesses operating on tight pricing structures.

Interest or Financing Rates

In addition to service fees, some providers apply interest based on how long the invoice remains unpaid. The longer a customer takes to pay, the higher the total financing cost becomes. Businesses must calculate the effective annual rate to understand the true cost.

Qualification Requirements

Not all businesses qualify for invoice discounting. Providers often assess customer creditworthiness, revenue history, and invoice quality. If customers have poor payment records, approval rates may decline or fees may increase.

Customer Non-Payment Risk

In many invoice discounting agreements, the business remains responsible if the customer fails to pay. This means the company must repay the lender even if it has not collected funds from the client. Understanding recourse versus non-recourse terms is essential.

Impact on Profit Margins

Frequent use of invoice discounting for small businesses can gradually reduce profitability if fees accumulate. Businesses should evaluate whether improved cash flow justifies the financing expense.

Administrative and Contract Complexity

Financing agreements may include minimum usage requirements, contract lock-in periods, or volume commitments. Reviewing contract terms carefully prevents unexpected financial obligations.

When Should a Small Business Consider Invoice Discounting?

Rapidly growing businesses often experience cash shortages despite strong sales performance. When revenue increases faster than incoming payments, liquidity gaps appear.

Companies with large outstanding receivables or extended payment terms may benefit from unlocking that capital. Contract-based industries such as staffing, logistics, and manufacturing frequently use invoice discounting to maintain operational flow.

Seasonal businesses can also use invoice discounting strategically during peak production months. This provides liquidity when expenses are highest and revenue collection is delayed.

The Importance of Accurate Invoicing

Faster Financing Approval

Clean, error-free invoices increase the likelihood of immediate approval when applying for invoice discounting. Lenders verify invoice details before releasing funds, and discrepancies can cause delays.

Reduced Payment Disputes

Incorrect quantities, pricing errors, or unclear payment terms often result in client disputes. Disputed invoices typically cannot be financed, which slows down access to working capital.

Clear Payment Terms and Due Dates

Transparent terms reduce confusion and encourage on-time payment. Clearly defined Net 30 or Net 60 schedules support better receivables management.

Proper Supporting Documentation

Purchase orders, delivery confirmations, and signed contracts strengthen invoice validity. Lenders and customers both rely on accurate documentation before releasing funds.

Improved Cash Flow Predictability

Accurate invoices are paid faster and qualify more easily for financing. This creates smoother liquidity management and reduces financial uncertainty.

Stronger Business Credibility

Professional and consistent invoicing practices build trust with both customers and financing providers. Credibility can lead to better financing terms and stronger client relationships.

The Role of Recurring Invoices in Stabilizing Cash Flow

Predictable Recurring Revenue Streams

Subscription-based or contract-driven billing creates consistent income patterns. This stability reduces sudden cash shortages and improves budgeting accuracy.

Automated Billing Schedules

Recurring invoices are generated automatically at predefined intervals. This prevents missed billing cycles and ensures revenue is captured on time.

Reduced Payment Delays

Automated reminders and scheduled invoices minimize late payments. Clients are less likely to forget recurring obligations when systems handle notifications consistently.

Improved Accounts Receivable Management

Recurring billing simplifies tracking of outstanding balances. Businesses can quickly identify overdue accounts and take corrective action.

Lower Dependence on Financing

When revenue is predictable, the need for invoice discounting for small businesses may decrease. Stable cash inflow reduces reliance on external funding solutions.

Enhanced Financial Forecasting

Consistent billing cycles provide reliable data for projecting future income. This improves strategic planning and long-term financial decision-making.

How Can Businesses Combine Invoice Discounting with Billing Automation?

Automation accelerates invoice creation immediately after service delivery. This means invoices can be submitted for financing faster, improving liquidity timing.

Real-time receivables tracking allows business owners to see exactly how much capital is tied up in unpaid invoices. With better visibility, financing decisions become more strategic.

Automated reminders encourage timely customer payments. As collection efficiency improves, reliance on invoice discounting for small businesses may decrease.

Improving Financial Forecasting

Forecasting becomes more accurate when recurring revenue streams are clearly tracked. Predictable billing cycles provide stable baseline projections.

Monitoring aging reports helps identify payment delays early. Businesses can proactively adjust spending or financing needs before issues escalate.

By analyzing receivables trends, companies can determine whether invoice discounting is a short-term solution or a recurring necessity. Strong financial data supports smarter strategic planning.

How ReliaBills Supports Small Business Cash Flow

Strong cash flow begins with efficient billing. ReliaBills simplifies digital invoicing so small businesses can generate accurate invoices quickly and consistently. Automated workflows reduce manual entry errors and shorten billing cycles, which helps close the gap between service delivery and payment receipt.

Recurring billing plays a central role in stabilizing income. ReliaBills allows businesses to automate recurring invoices for subscription services, maintenance contracts, or installment agreements. By ensuring invoices are sent on time and reminders are automatically triggered, recurring billing reduces delays and strengthens accounts receivable performance.

For businesses seeking deeper insights, ReliaBills PLUS provides advanced reporting and real-time receivables tracking. Owners can monitor overdue balances, analyze payment trends, and improve forecasting accuracy. By combining invoice discounting for small businesses with automated recurring billing, companies build a more resilient and predictable cash flow system.

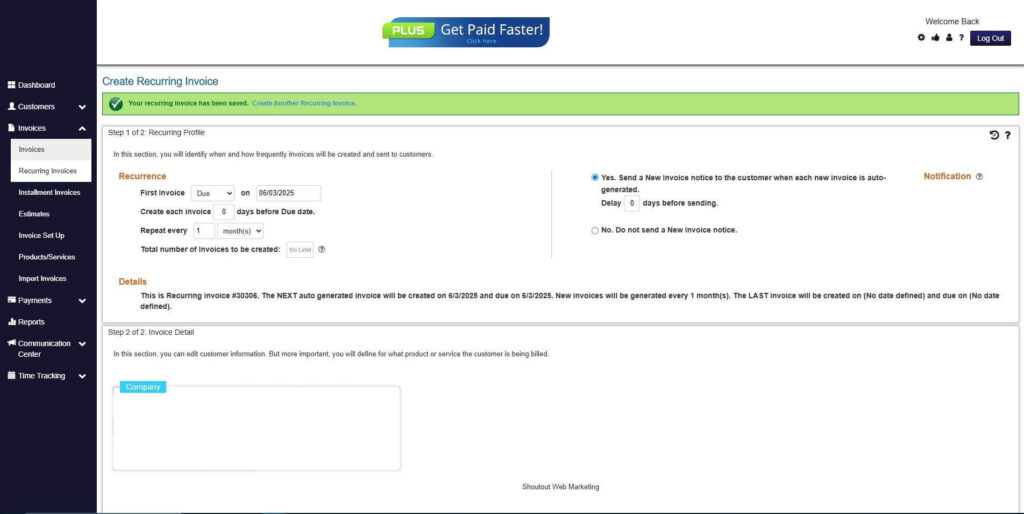

How to Create a New Recurring Invoice Using ReliaBills

Creating a New Recurring Invoice using ReliaBills involves the following steps:

Step 1: Login to ReliaBills

- Access your ReliaBills Account using your login credentials. If you don’t have an account, sign up here.

Step 2: Click on Recurring Invoices

- Navigate to the Invoices Dropdown and click on Recurring Invoices for an overview of the list of your existing customers.

Step 3: Go to the Customers Tab

- If you have already created a customer, search for them in the Customers tab and make sure their status is “Active”.

Step 4: Click the Create New Recurring Invoice

- If you haven’t created any customers yet, click the Create New Recurring Invoice to create a new customer.

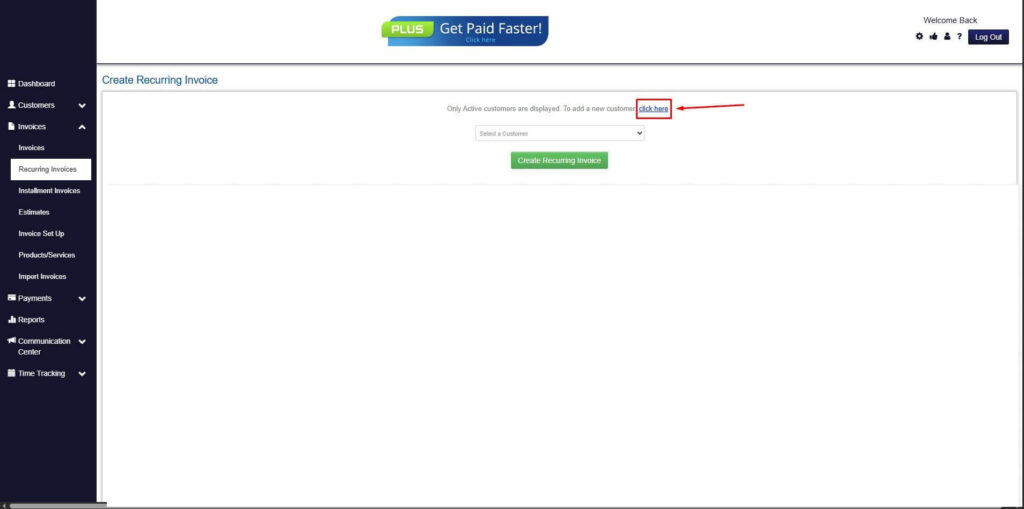

Step 5: Click on the “Click here” Button

- Click on the “Click here” button to proceed with the recurring invoice creation.

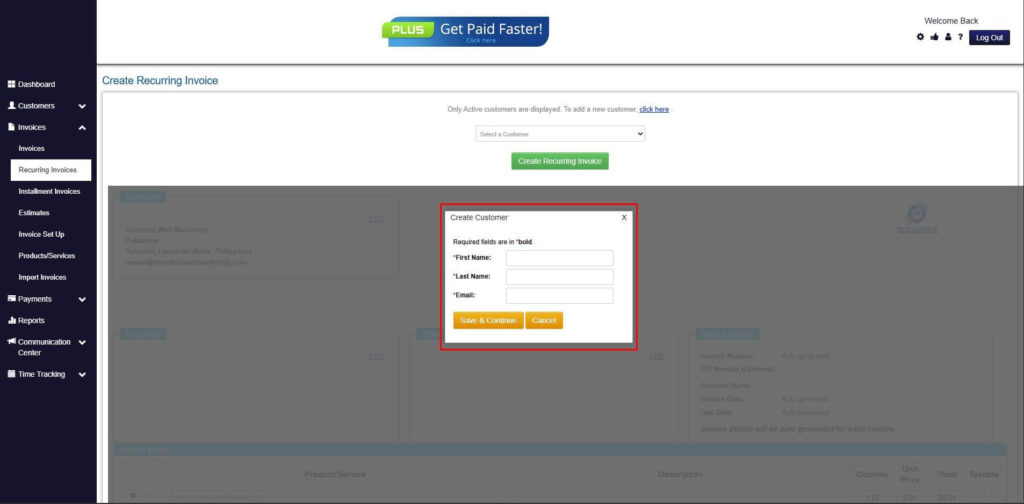

Step 6: Create Customer

- Provide your First Name, Last Name, and Email to proceed.

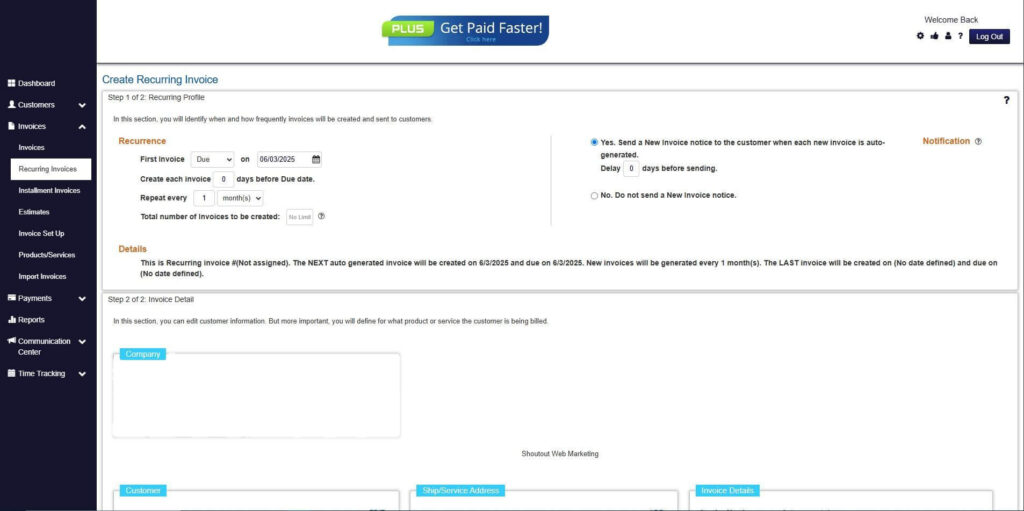

Step 7: Fill in the Create Recurring Invoice Form

- Fill in all the necessary fields.

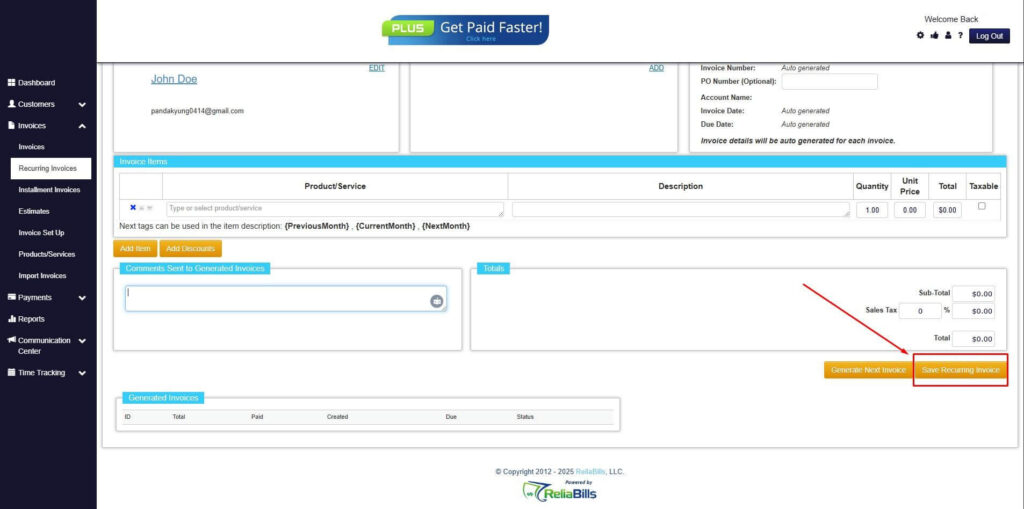

Step 8: Save Recurring Invoice

- After filling up the form, click “Save Recurring Invoice” to continue.

Step 9: Recurring Invoice Created

- Your Recurring Invoice has been created.

Frequently Asked Questions

1. Is invoice discounting suitable for startups?

It depends on revenue stability and customer creditworthiness. Startups with consistent invoicing may qualify, but lenders often require proven sales history.

2. Does invoice discounting affect customer relationships?

In most cases, it remains confidential, so customers are unaware of the financing arrangement.

3. Can recurring invoices reduce the need for invoice discounting?

Yes. Predictable recurring revenue improves cash flow consistency and may reduce reliance on external financing.

4. Is invoice discounting expensive?

Costs vary by provider and risk level. Businesses should compare fees against the value of improved liquidity.

Conclusion

Invoice discounting for small businesses offers a practical way to bridge cash flow gaps caused by delayed payments. It unlocks working capital tied up in receivables and supports operational continuity.

However, financing works best when paired with strong invoicing systems and disciplined receivables management. Accurate documentation, recurring billing automation, and real-time tracking reduce dependency on external funding.

By combining smart financing strategies with automated billing solutions, small businesses can improve liquidity, strengthen financial control, and position themselves for sustainable growth.